well Now you know

This is what your portfolio will look like if the Fed hikes (again) into a slowdown.

Boston Fed head Eric Rosengren's "time to hike" comments must be part of a new Federal Reserve policy initiative to be anti-data-dependent. In the face of very obvious U.S. #GrowthSlowing data, he just ramped the Fed Funds Futures on a SEP hike from 20% to 34%.

That's why stocks and bonds are down. That's also giving you an immediate-term TRADE oversold signal in most things I like.

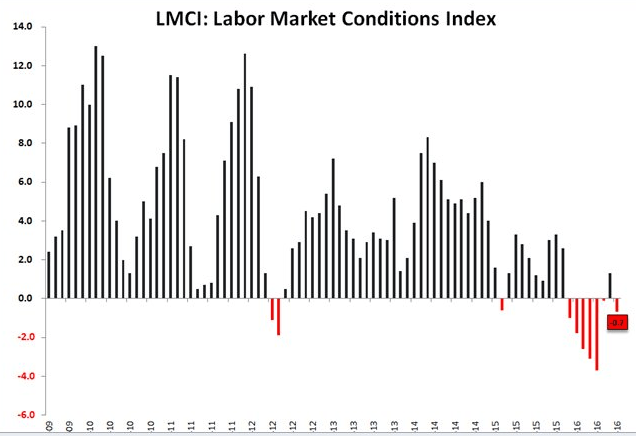

I'll leave you with the chart below. Wasn't this Janet Yellen's favorite indicator once upon a time?