“We don’t know what we’ll be doing a year from now ... you can’t expect the Fed to spell out what it’s going to do... because it doesn’t know."

-Stanley Fischer, FOMC Vice Chairman

Has your investing enthusiasm stagnated, secularly?

Is your proclivity for abandoning rationality in favor of serial attempts to front-run changes in policy rhetoric now past peak?

Are you unsure whether bad (macro data) is still good (for asset prices)?

Has your early cycle euphoria gradually ceded share to existential late-cycle angst?

You are not alone. And the chronic fatigue you are experiencing may not be your fault.

Not too many people know this but some compelling, early-stage research suggests that that constellation of psycho-emotional symptoms singularly characterizes a new category of acute disorders broadly classified as Fed Associated Recurrent Torpidity Syndrome … or, #FARTS.

There’s good news and bad news.

The bad news is that there is no existing remedy for FARTS and it’s likely only to worsen nearer-term.

The good news is it’s Friday.

Back to the Global Macro Grind …

When I was a teacher, a pedagogical point of emphasis was repetition and restricted focus.

In other words, focus the lesson on a singular or limited set of topics and repeat/practice to the point of inanity. Students may begin to get bored but they will remember the main takeaways of an exclusive topic. An eclectic and ranging discussion may be more interesting in the moment but retention will be close to zero in t+x days.

In that didactic spirit, I wanted to update an isolated theme we’ve given some focus to in institutional notes but not in Early Look-scape:

It’s an offshoot of a great call our healthcare team has had with their #ACATaper theme (email if you are interested in the Healthcare team’s work).

Here’s the conceptual and quantitative underpinning.

The implementation of the Affordable Care Act (ACA) resulted in a largely unprecedented influx of newly insured individuals. Because many of those formerly chronically uninsured had deferred care and carried higher acuity, their utilization rates subsequent to gaining coverage were comparably higher. The ramp in the insured base coupled with higher utilization and cost rates for the newly insured drove healthcare consumption higher and a discrete ramp in sales in earnings growth for the sector. Growth rates in healthcare relative to the S&P500 broadly and its defensive brethren (staples and utilities) decoupled, leading to marked outperformance in the related equities. The #ACATaper theme is centered on the reversal of this dynamic as the sector comps out of the benefit and growth shows a meaningful deceleration.

At the macro level, the implementation of ACA has provided a clear benefit to both employment and aggregate consumption growth.

That benefit becomes evident in the data concurrent with the initial enrollment deadline for ACA at the start of 2014 and builds conspicuously through 2015.

- Employment Palooza: Healthcare's share of total employment began to ramp in mid-2014 with Healthcare payroll gains driving ~16% of total NFP growth from 2Q14-2Q16. With healthcare industry employment just 10% of total, this represents a disproportionate share of growth.

- Benefit = Past Peak! Healthcare Job Openings (JOLTS) and net monthly payroll gains peaked in late 2015 alongside peak NFP gains and have begun a modest retreat in 2016. After broadly accelerating for 2 years, Healthcare employment growth peaked in March 2016 and has now decelerated in each of the last 5 months. Meanwhile, Job Openings in Healthcare – which show a strong relationship with overall medical consumption spending – dropped -6% sequentially in July and posted their first year-over-year decline in 26 months at -4.75% YoY. The Chart of the Day below depicts the ACA associated ramp in Healthcare employment and the emergent deceleration.

- Amplification Goes Both Ways: While trailing 6M/12M NFP gains have slowed in 2016, monthly Healthcare job gains have slowed only modestly until the most recent month. Healthcare employment rose just +14K in August, down from the +40K TTM average and marking the smallest monthly gain in 3 years. Should the fledgling deceleration in Healthcare employment progress, Healthcare would reverse from a relative support to a negative amplifier of the headline trend.

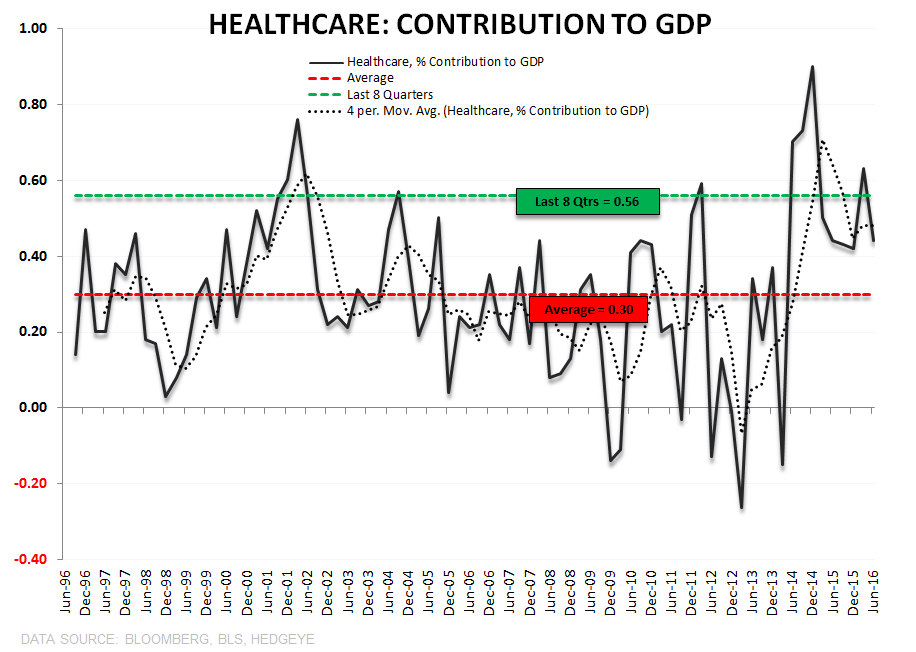

- GDP Juicing: As the chart above illustrates, over the last 8-quarters Healthcare’s contribution to GDP has seen a step function increase, contributing almost double its average contribution observed over the last 20 years.

Alas, the vision that we could one day all work in the healthcare economy and use our collective earnings to pay for each other’s collective healthcare under ACA in one utopian, incestuous circular economy was not to be.

ACA has proven effective as a jobs and consumption stimulus program. It served to augment employment growth over the last two years and has helped support headline payroll gains in the face of ex-healthcare softening in 2016.

However, as the #ACATaper theme plays out and the benefit decays, the support to NFP will similarly diminish.

The simple macro punchline is that #ACATaper is likely to = #NFPTaper.

Our immediate-term Global Macro Risk Ranges (with intermediate-term TREND signals in brackets) are now:

UST 10yr Yield 1.51-1.63% (bearish)

SPX 2166-2190 (bullish)

VIX 11.59-14.48 (bullish)

Oil (WTI) 42.86-48.61 (bearish)

Gold 1 (bullish)

Have a great weekend.

Christian B. Drake

U.S. Macro Analyst