Conclusion: The RH story is more complex than ever, but the call on the stock is arguably as simple as we’ve seen it in a while. Over the near term, the company is in the ‘dammed if they do, dammed if they don’t’ category. Sentiment is still so bad around the name, and both the stock and the team running the company are so hated, that we’re relatively sure that people will drill down hard on any misteps in the quarter – and there will be missteps – there always are with such a dynamic story. Conversely, whatever goes right, either by design or even by accident, is not likely to lend much to RH’s Street cred, at least not until the company can exhibit that things have stabilized and it can drive the business consistently in the right direction. Let’s face it…right now this company was just handed a Red Card and was ejected from the game. And to be clear, so are we for making the call. But so much of that is in the stock, and arguably was there before the company owned up on the last print when the stock fell from $103 to sub $30. Being ejected (TRADE) from the game does not wipe out the season (TREND), and very rarely/(thankfully) does it end a career (TAIL). We make mistakes and we learn. But in the end, we definitely think that RH will play again this season, and that should be apparent in 4Q of this year.

As we’ve stated numerous times since the blow up earlier this year, we’ve stepped back and re-examined this one ad nauseum. We have absolutely no problem walking away from a mistake. But any way we look at it (most ways, at least) we come out on the long side at $33 and a mere $1.6bn in market cap relative to $3bn in identifible and profitable revenue growth ahead of RH. No one cares about $6, $7, or $8 in earnings power anymore (even if it’s still there). If they did, it would not be trading at 6x those earnings and 3x EBITDA. But with the stock so beaten down, there are two real questions to ask…

1) Is the long-term opportunity still there? And,

2) Does management have the vision, the plan, and the raw process/talent to execute on the plan?

If the answer is Yes to both (and we think it is) – and if you have the luxury of looking at a TREND and TAIL duration (ie. into 2017 and through 2018/19), then we suck it up on the red card and look to the rest of the season. In spite of all the hate mail on the call, and the downright apathy as it relates to the story, we think that the upside/downside over 6-12 months is 4 to 1 on this name.

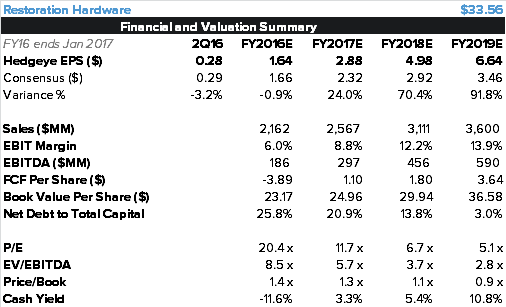

It all comes down to earnings and growth, right? In the end, earnings estimates for next year and beyond are too low. Yes RH messed up on the Modern roll out, managing new product flow, and a significant slow-down in the space early this year. It did not help that it all happened at once – mostly self-inflicted. But when we look at the costs associated with this mess (which we credit RH as not stripping out of results as other companies might do), we’re looking at underlying earnings of $2.50 this year versus the $1.65 it is likely to report. When we look at the base, grow it by maybe 10% – which it should at least do given square footage growth, a newer, less stale and more relevant product assortment, and better gross margin flow through from lower lease minimums associates with larger-format stores – then we can build to EPS of $2.80-$3.00 in 2017. The Street is currently at $2.30. Perhaps $3.00 is rich given the lack of management credibility and the potential for something to go wrong – again.

But building up to $4.50-$5.00 over 2-3 years is completely realistic. This earnings stream is absolutely not permanently impaired. Those numbers are 50-60% ahead of consensus. At the current multiple, we think the stock will work if earnings are only 10% above consensus.

Here’s a few points on both the call and what we want to see from the print.

- Inventory, Inventory, Inventory: This is obviously a bigger issue for the company than cleaning up its balance sheet. The company made a strategic decision to a) put a hold on the opening of new distribution facilities for at least another 2-3 years, and b) reduce its SKU count as it works to reassort the back end across category lines instead of regional lines. The company has the latitude to do the heavy lifting over the near-term with gross margins guided down 600-700bps in 2Q16. But in order to get more comfort in a rebased earning stream in 2017, we’ll need to see meaningful progress on this line.

- Efficacy of Grey Card RH Membership Program: Changing the way consumers shop is a tall enough task on its own. But this has been anything but an ordinary operating environment for RH. That, we think, makes it tough to gauge the efficacy of the Membership Program (as it is now being dubbed). Here is what we mean…i) the company decided to push all new product introductions (with the exception of RH Outdoor) into 2H16, skewing the math on what had been a typical late spring/early summer supply and demand curve, ii) vendor and supply chain snafus have limited the flow of product to the extent that order behavior has been altered by out of stocks, and iii) the promotional behavior from the company hasn’t changed significantly as it has worked to clean up inventory levels. On the last point, the company sent 115 promotional emails in 2Q16 – of those, 41% mentioned a sale in the title of the email blast above and beyond the 25% discount associated with the Membership Program (55% RH, 32% RH Teen, and 0% RH Modern). That looks a lot like the old status quo. There’s a good chance that RH meaningfully backs away from the Membership program – and already kinda did when it changed up the name. This might be the right business decision, and the right consumer decision, but not a Wall-Street confidence booster until people see that its accretive to the financial model. We’ll see…

- Management: The company is about 3 months removed from its corporate re-shuffle which saw the company eliminate $20mm in corporate related employee costs. Along with that, there has been considerable movement in the C-Suite with the COO Ken Dunaj, Chief Development Officer Doug Diemoz, and all 3 Chief Merchants exiting stage left in the past 18 months. Tack on the creation of the three Co-Presidents and it = a lot of moving pieces on a management team that has seen its credibility take a hit along with its market cap. That being said, we think that Gary Friedman has the strategic vision and pieces in place in order to execute on the plan. But – and this is a big but – we think that there needs to be plenty of talk about the additional pieces added to the RH management equation to give the street some confidence in the management team, as well as its ability to execute on the plan to restore sustainable growth to this story.