“If only we had the vast knowledge of God, everything could be understood and predicted.”

-Benoit Mandelbrot

If you’re not religious but looking for new options, I do not recommend bowing at the altar of Federal Reserve forecast conformity. Thank goodness (and my God) that the USA’s economic data continued to slow yesterday. Stocks, commodities, and bonds loved it!

That’s right, #GrowthSlowing remains the bull case for “stocks” inasmuch as it’s always been the secular/demographic one for long-term US Treasuries. So I’m thinking I’m going to pick up some mind share from those marketing long-only-equity strategies until this stops.

If bad is good, when will bad become bad? No worries. Mr. Macro Market will let us know. That’s why what my man Mandelbrot called a “contrary approach, macroscopic instead of microscopic, stochastic instead of deterministic, more fruitful” to proactively predicting market scenarios than making a demi-Goddess out of Janet Yellen’s forecasts. (The Misbehavior of Markets, pg 29)

Back to the Global Macro Grind…

‘Dammit Keith, stop blaming Janet. She’s a nice lady and she works hard.’ Oh, I totally agree with that. If she’s “data dependent” she’s going to have to pivot back to dovish from hawkish – that’ll be her 6th hawkish/dovish pivot in 8 months. That’s really hard work!

What up with yesterday’s data, bros?

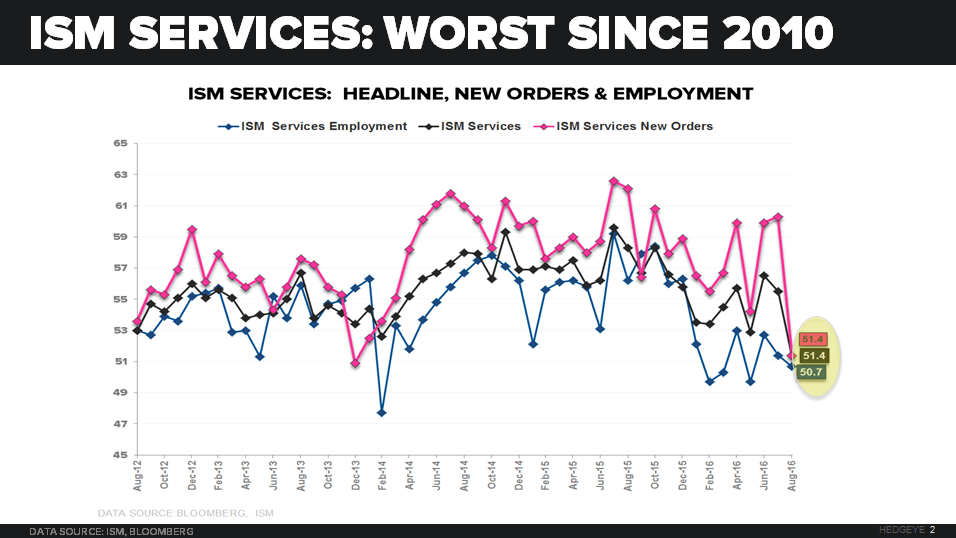

- ISM Services (proxy for 70% of the economy) slowed to 51.4 in AUG vs. 55.5 in JUL

- Business Activity and New Orders dropped a remarkable -7.5 pts and -8.9 points, sequentially

- Employment declined -0.7 pts, barely holding above a contraction at 50.7

Seriously. That was the worst ISM Services report since 2010 and the largest sequential decline in New Orders (leading indicator) in 104 months and this character at the San Francisco Fed, John Williams, came out intraday saying “the economy is strong” and needs rate hikes.

What, precisely, does “the economy is strong” mean? At Hedgeye we deal in real-time and space terms using this thing called the 2nd derivative as a leading indicator for future “levels.” In other words:

A) The economy is either accelerating or

B) The economy is decelerating

It’s not that complicated. Neither is measuring and mapping the rate of change in “inflation.” It’s easy to track how macro markets are pricing in deflation vs. reflation. The 5-year US Treasury Break-Even Rate has deflated back down to where it started 2016 = 1.30%.

Back to the whole concept we’re willing to give Williams a teach-in on @HedgeyeHQ – is the “data” getting better or worse (accelerating or decelerating)? If you’re into data point breadth, here’s a list that “data dependent” hawks should obfuscate or ignore:

- Chicago PMI = Worse

- ISM Services = Worse

- ISM manufacturing = Worse

- Markit Manufacturing PMI = Worse

- NFP = Worse

- Auto Sales = Worse

- Existing Home Sales = Worse

- Labor Market Conditions = Worse

In other words, like corporate profits, the manufacturing and industrial side of the US economy remains in a #Recession. Whereas the bigger and broader #LateCycle swath of the US economy (labor and consumption) continues to slow from its 2015 economic cycle peak.

I’d be more than happy to invite any establishment economist to our Macrocosm 2016 Conference (November 16th at The Yale Club in NYC) to debate me on why what I just wrote isn’t 100% accurate. Again, both stock and bond market bulls should be thankful it is.

While they aren’t accelerating on a trending basis, I purposefully left a few “bullish” economic data points off the aforementioned list. Can you tell me what they are? Do they, pardon the pun, trump the other eight? What is going to make those 8 data points great again?

Those are actually tougher questions than answering the why on how many economists/strategists missed the 2016 US economic slow-down. Two centuries ago, before astronomers had good telescopes, establishment scientists were able to obfuscate reality too.

I believe there is a God. I sort of believe there’s hell too (working for Obama’s Fed would certainly be some version of it). While I can prove those things to myself qualitatively, I can’t prove them to you, quantitatively, like I can the rates of change in economic data.

Our immediate-term Global Macro Risk Ranges with intermediate-term TREND Research Views in brackets are currently:

UST 10yr Yield 1.51-1.61% (bearish)

SPX 2166-2189 (bullish)

RUT 1 (neutral)

NASDAQ 5196-5284 (bullish)

XOP 35.21-37.98 (neutral)

RMZ 1 (bullish)

Nikkei 168 (bearish)

DAX 104 (bearish)

VIX 11.65-14.40 (bullish)

USD 94.23-96.49 (bullish)

EUR/USD 1.11--1.13 (bearish)

YEN 99.80-104.38 (bullish)

Oil (WTI) 42.77-45.90 (bearish)

Nat Gas 2.61-2.89 (bullish)

Gold 1311-1360 (bullish)

Copper 2.02-2.12 (bearish)

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer