Wayfair remains one of our top ideas on the short side. While still 16% below where it was before the earnings blow-up four weeks ago, it has been strong over the past week headed into the Goldman conference. That’s not a surprise given that this management team is actually quite impressive when on the presentation/breakout/1-on-1 circuit. But as good as it is in selling its story to the street, as bad as we think it will prove to be in selling home furnishings profitably to a target market that we don’t think exists.

Here’s a few visuals that might offer up some context for questions for management on Wednesday morning.

1) $$$$$. If there’s one thing that’s clear, it’s that this company needs to spend up meaningfully to drive its top line (which, while decelerating, is still clocking in at an impressive 60%). We’re seeing the employee count grow at a staggering rate of 88% YY on top of 61% growth in customer acquisition expenses in the latest quarter. What interests us the most is how correlated customer acquisition costs are with repeat customer rate. In other words, repeat customers no longer need to be acquired. This could be a powerful model if acquisition costs roll off without a deceleration in revenue – but we would not bank on that. Aside from articulating – with specificity – what product categories to what consumers will profitably drive its top line (ie why its data/market research is better than ours), drilling down on these numbers would be our top focus with management.

2) EUROPE – THE FINAL COUNTDOWN? The original plan was for EBITDA to inflect at the end of 2016, but then European expansion pushed that out. At a fundamental level, we question why the company would look to grow in an even more difficult and fragmented market like Europe when it has yet to prove that can make money in a homogenous market like the US. Could the difference in cultures throughout Europe offer up more opacity in pricing – ie better margins? How does this offset the complexity of operating there? For example, the drive from the Northernmost point in Italy to the southern tip is about the same as NY to Miami. And while the customer in both US markets are the same, they are dramatically different from one another in Italy – not to mention the rest of Western and Northern Europe. When and how will incremental margin turn positive?

3) COMPETITION. Someone humor us and ask management how they think competition is reacting to Wayfair’s growth. Online vs Brick & Mortar. We don’t think management is arrogant or cocky enough to say ‘we don’t worry about competition given the $90bn addressable market.” If they said that and acted accordingly, then it would make the longer-term call close to bullet-proof. But if management articulates who and what it competes with different brands and in different product classifications and price points – everything from Bed Bath & Beyond to Amazon, to Pier 1, to Pottery Barn, West Elm, Williams-Sonoma, and RH – then we’ll be extremely impressed. Our bet is that they come out closer to the former. Anyone long this stock should want to prove us very wrong here.

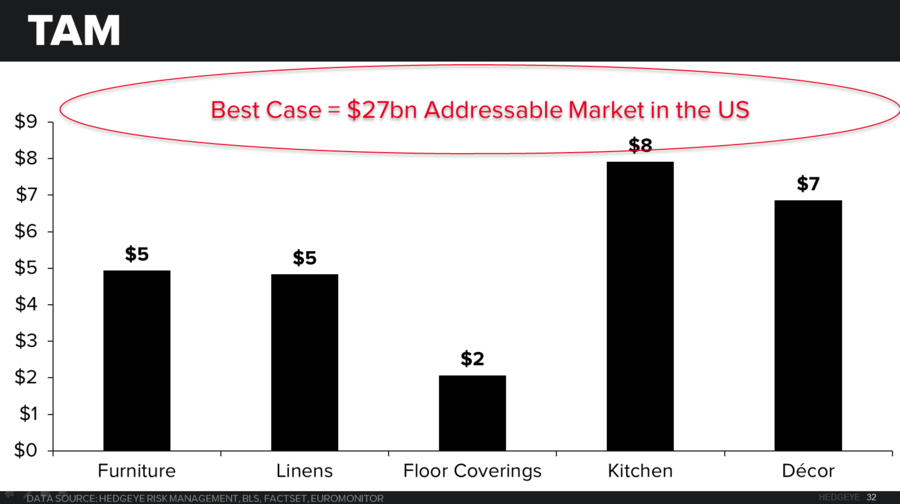

4) ADDRESSABLE MARKET. Our research suggests (see slides below) that management’s $90bn/60mm household target market is a pipe dream. The brands currently have about 75% awareness, which translates to about 3% of the targeted addressable market and 11% of target households as customers. How will the company get this done without excessive cost?

5) INSIDER SALES. When does this trend stop?

Addressable Market