This quarter was not a disaster by any means, but with slightly weaker revenue and a tempered outlook, it’s certainly not what a $76 stock at a 35x multiple needs to see. The aftermarket sell-off shows that clear as day. But the reality from where we sit is that there is much more downside from here. Our call was to press the short on the print. In hindsight, we’d have stuck with the same call from a risk management perspective. The reason is that even though the stock is selling off after market, we think there’s a good $20+ in downside left in this name. Our major concern is that numbers, and the rising capital costs to capture incrementally lower margin growth, do not synch with elevated expectations, and the company will need to guide down in 3-6 months, or flat out miss by 10% or better in 2017.

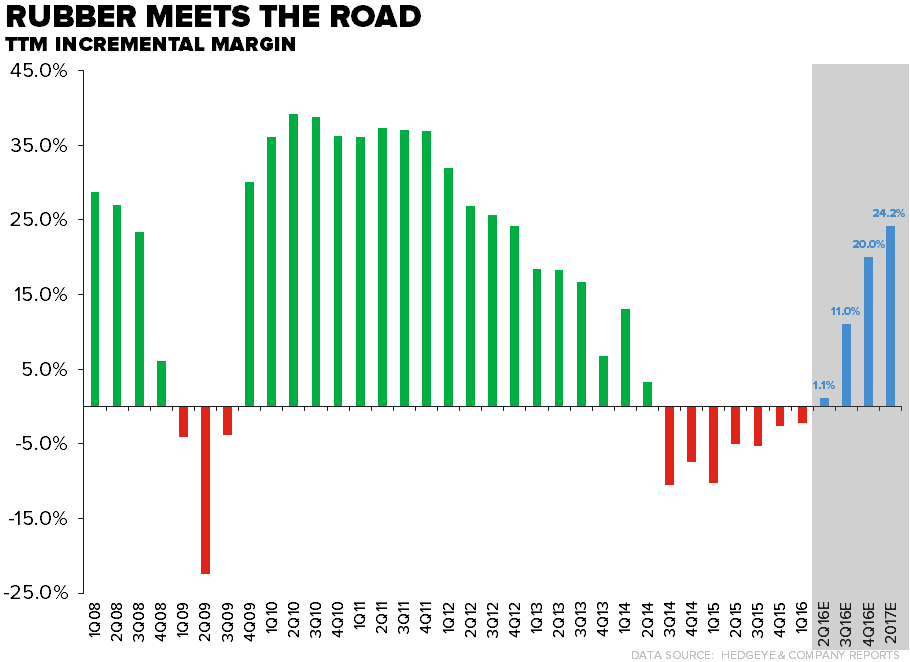

The TTM incremental margin in this quarter was under 4%, and expectations – even after weaker guidance -- are calling for that to accelerate to a whopping 24% over the next three quarters. We think that LULU will flat-out miss this target. Even if we’re wrong, the incremental buyer needs to ask if there is any potential upside from these aggressive targets? We think No. We would love to engage in that debate, and we’re pretty sure we’d win (see note below for details).

To be fair, LULU put up absolute EPS growth of 12% -- which is actually good for a retailer in this day and age (though not worthy of nearly a 3x PEG ratio). In addition, it just put up the best Gross Margin improvement since 2Q 2011 on top of a downright impressive move in the SIGMA – that is nearly a lock for some level of gross margin improvement in the coming quarter. That’s the biggest, and perhaps only real positive from this print.

But the whole thing does not sit well with us, for several reasons…

- Management is hinging this story on a long-term comp of at least 9% -- the level needed to leverage SG&A, but it admits that customer traffic continues to be a problem (in 3Q to date as well), and is banking on higher Average Unit Retail (AUR -- i.e. price/mix per item) and Units per Transaction (UPT). We don’t see how anyone can rely on this given the longer-term competitive pressures from solid brands with far better strategic visions, management teams and Boards.

- Above all that, the fact (and it is a fact) that with the absence of a wholesale model – one that we think LULU is likely not capable of executing alongside its DTC business – and real estate growth outside its core markets, the company is simply not ‘fishing where the fish are’. Of COURSE traffic will be a problem in this scenario. Why should that turn around?

- LULU took up capex slightly this quarter (2-3%) and moderated its SG&A leverage expectation to spend on the brand – but we need to see a lot more than the ~22% it is spending on the margin. We need at least an incremental $150 million in annual spend, or about another 75bps in margin – and we could even argue something closer to $250mm to meaningfully accelerate top-line growth to the levels needed to grow consistently and profitably. We heard no part of the strategy on the conference call that makes us think otherwise. Potdevin can talk about the ‘Feathered Designs and Technical Silouettes’ all he wants…the fact is that expectations are very high, growth is slowing, and the cost of growth is heading up. That means lower returns – structurally – which hardly synchs with the stratospheric multiple.

Below is our previous note from 8/30/16

08/30/16 02:33 PM EDT

LULU | The Rubber Meets The Road

Takeaway: Next year’s #'s look 10-15% too high – setting up for a big miss/guide down, just not tomorrow. We’re comfortable shorting more post-print.

Conclusion: Our LULU short call is admittedly at a polarizing point in its decision tree. On one hand, we think that this company represents one of the weakest management teams with very little brand vision and strategy that is coasting on the heels of a strong category and an unsustainable capital and margin structure. We think that earnings next year approach $2.20 vs the current consensus estimate of $2.54. In fact, the Street’s $3.00 number for 2018 might not happen for another 3-4 years. The problem is that the quarter to be released tomorrow – at least as we see it – looks fine relative to expectations. There’s very little chance we’ll get a guide down for another 13 weeks until 2017 is staring the company in the face. Even then it might not guide down until an all-out miss becomes a reality in 1H17. With the stock trading at 35x what we think it will earn next year, we think there’s up to 50% downside over 9-12 months as the multiple compresses on a lower earnings base (20x $2.20 = $44). That’s flat-out dangerous with the stock over $75 today. But until then, we’ve got near-term margin tailwinds, a double digit EPS/cash flow algorithm (tough to find in retail today), and short interest at 18% of the float – definitely not something we want to make a big call on the day before the quarter. But if people become even more elated by a near-term pop in growth, we’re confident enough in the eroding return and growth profile that we’d short more.

The Rubber Meets The Road:

For the first time in the better part of 2yrs, there are some serious expectations embedded in the LULU story. While there are some comparison tailwinds to consider as the company laps an investment phase primarily focused on the back of house, we think that’s more than represented in the 35x P/E and 19x EBITDA forward multiples. This quarter should – and probably will – provide the management team with all the ammunition it needs to talk up its margin expansion story Heck, the first quarter of Gross Margin expansion in over 14 quarters is worth a slap on the back. And should (assuming that the demand equation doesn’t completely fall apart) give the bulls enough to latch onto.

Then we fast forward to 2017 and we need to assume 2012-esque incremental margins – in the range of 25% – to get to current consensus numbers. We think that’s a high hurdle rate for any company at the tail end of an economic cycle, and even more ambitious for a company like LULU which… i) has some of the biggest question marks in the C-Suite out of any company that we cover and ii) continues to invest in non-core businesses in the shape of Men’s, Intl, and Ivivva in order to prop up the top line.

And It’s Not Just One Year

Past 2017, LULU’s current plan (which closely mirrors consensus expectations) assumes an incremental margin in the range strikingly similar to what it experienced in Stage 1 of its growth cycle (which we define as the years 2005-2011). During that time period, the company added nearly $1bn in sales, created a category, and scaled it across the top markets in the US and Canada. All in, that was good for an incremental margin of 30%.

Today, LULU’s core business (which we characterize as the US and Canada) accounts for 92% of sales and 104% of EBIT. From here, the company is investing a boatload of capital into the non-core future topline growth vehicles (Men’s, Int’l, ivivva), which will take the revenue mix from 90%+ core to 75% by 2020. Don’t get us wrong, there is nothing wrong with diversifying a business model (we think LULU should do wholesale). But the problem herein lies in the expectation that LULU can get both topline reacceleration AND margin recovery as it moves the mix away from the most profitable and mature parts of the business in the US and Canada

The punchline is that as LULU shifts incremental growth away from the core businesses, we will see an offset to the margin recapture over the near and long-term. We get to steady state margins in the teens vs. the Street approaching 20%. That translates to an ultimate (4-5 year) earnings number barely hitting $3.00 vs the Street marching blindly towards $4.00.

E-Comm, Ho-Hum

There are puts and takes by quarter, but we think the overarching trend in the e-commerce growth rates can be defined as lower lows and lower highs. The 17% reported growth rate in 1Q16 was the 2nd lowest the company has ever reported, and based on our analysis of the traffic trends it doesn’t appear that there has been a meaningful inflection through 2Q. The Street’s numbers don’t appear to be at risk as the company normalizes traffic flow after the website refresh in 1Q, but we think the company will need to re-accelerate this channel meaningfully in order to hit MSD comp expectations through the year in light of the next section.

![]()

Brick and Mortar Going The Wrong Way

On a 3yr basis, constant currency store comps went flat in the quarter the company reported 3 months ago. We think that’s a meaningful metric for LULU, as there has been a lot of noise associated with the quarterly sales trends – particularly the Luon recall and Chip’s ‘our customers are fat’ comments. Comps get more difficult, going from a -1% compare in 1Q16 to +5-6% comps for the balance of the year, that’s pretty straight forward. What we think is far more important is that lack of new productive square footage coming into the sq. ft. base needed to stimulate Brick and Mortar comps. That’s glaringly obvious when you consider the following…

1) Int’l and ivivva will account for a greater percentage of new doors in 2016 (at 58% of the 40 units) than North America lululemon doors. That’s the new normal. And translates to higher investment and lower returns.

2) US growth is now centered around less productive/affluent markets. Whether you measure on athletic participation trends, income distribution, or population density the new markets LULU has entered over the last 3 years are less productive. Sq. Ft. growth opportunities in the top MSA’s are all but gone, hence the need to scale up square footage. This may be oversimplifying, but Albany, NY ≠ Houston, TX.

3) The math suggests that 2015 was the peak year of new sq. ft. comp benefits. Stores aged 0-3 years (i.e. in the key part of the maturation curve to drive comp growth) accounted for 40% of the portfolio in 2015. That ticks down in every year from here on out – to 20% of the portfolio by 2020. That means we will need to see either a) outsized category growth, or b) outsized market share gains at LULU amidst stepped up competition from copycat brands and women’s investment at NKE and UA.

As comp tailwinds from sq. footage growth dry up, we think it has encouraged return dilutive behavior, including accelerated Int’l growth and entering markets in the US where the spending and population demographics do not support the 4-wall model we have come to expect from LULU.

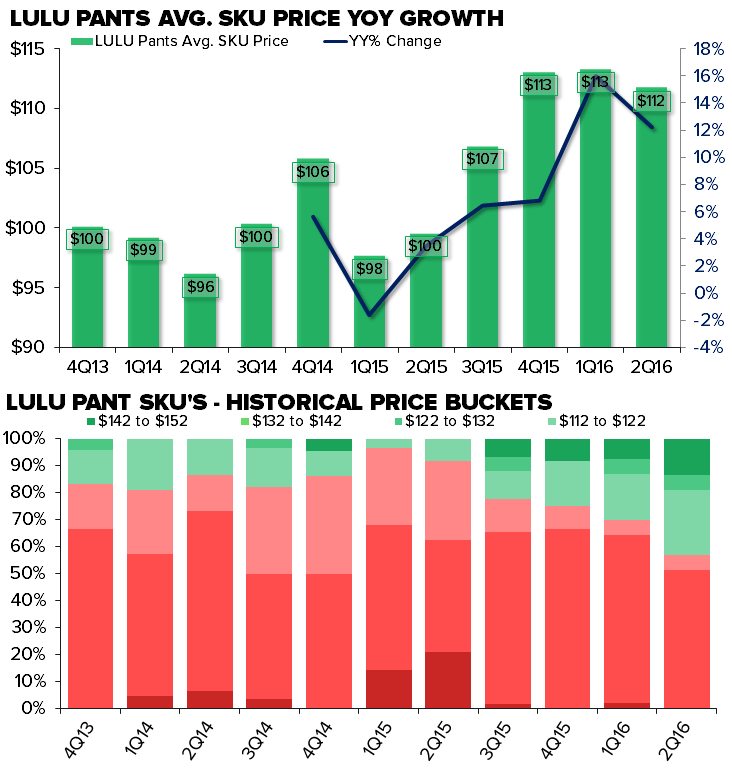

Still Another Quarter Of Price Benefit

Here’s a win for LULU – at least through the end of the year. The company repositioned its pants wall in September 2015 and took price at the same time. Since we’ve seen the average price of LULU bottoms SKU tick up by as much as 15%. The top of the pricing spectrum (over $110) now accounts for 30% of the total category. The company will start to anniversary those price increases in a few days but will have another two quarters of benefit.

On the tops front – there has been some press discussing the increase in price for some of the top selling SKUs. That appears to be the case on the high end, but based on our analysis, looks as if the company is building out its selection at the mid-tier price point between $52-$62. That bucket accounts for nearly 80% of the total selection on LULU’s website, taking average SKU price down by 2% in 2Q16.

What that means for the call is that the pricing bullet has already been fired, meaning LULU will have to consistently drive traffic to its doors. Given the volatility in traffic patterns for LULU historically, we’re not convinced that the company can win on traffic alone.