THE HEDGEYE EDGE

Key points to the Hedgeye long thesis for Expedia (EXPE) center around executing on its recent M&A initiatives, which we see as the most important part of the story moving forward.

Here are the three key takeaways on our long call:

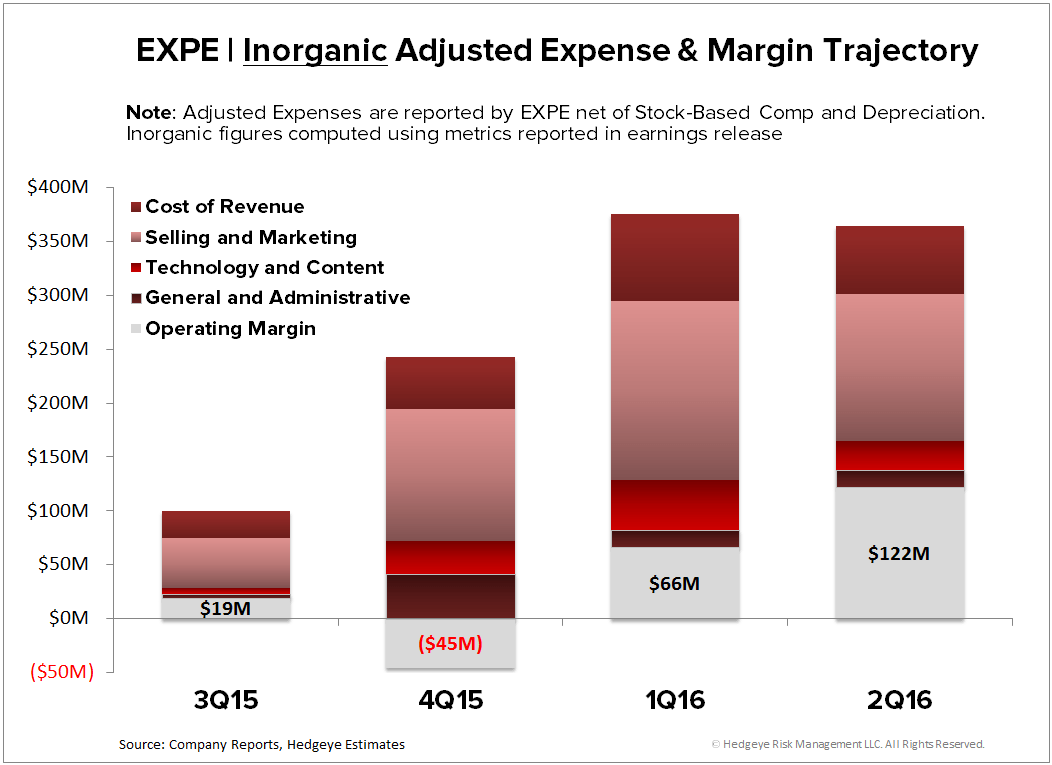

- “IT’S LARGELY A COST STORY” - EXPE guided to 35%-45% EBITDA growth in 2016, but after considering 2015 purchase accounting headwinds, its effective organic guidance is actually in the low 20% range. Management can get there largely on the cost side alone, with two big levers it can pull in addition to cutting redundant/duplicate costs

- PAY TO PLAY (AWAY) - The Homeaway (AWAY) model transition presents considerable near-term opportunity. While there’s some execution risk on the opt-in, we suspect EXPE holds all the cards here. Timing issues will limit the total 2016 opportunity, but management only needs to show progress to propel that story forward

- MAJOR RISK ON THE TABLE - We suspect the risk of decelerating travel trends is already on the table given EXPE’s 2Q deceleration in hotel room nights, which reset the bar for street expectations for the remainder of the year and essentially mitigated the last major risk to the story.

INTERMEDIATE TERM (TREND)

We expect 3Q16 results to refuel optimism in both the OWW & AWAY stories, especially since seasonality will have a greater inorganic impact that should optically amplify their 3Q results. We also do not see any major blow-up risk in the core business on the 3Q16 print since EXPE’s 2Q mishaps, which were largely self-inflicted and non-recurring, have rebased expectations for the rest of the year.

OWW transition on track: Looking to 2H 2016, management expressed that the heavy lifting is largely behind them and that they are incrementally optimistic that a large portion of OWW cost synergies will be realized. (Note: Despite the room nights whiff in 2Q, EXPE beat EBITDA estimates and maintained guidance for the year). Regarding OWW, roughly 40% of OWW’s annual EBITDA is historically concentrated into 3Q. The 3Q15 OWW purchase accounting headwind effectively means EXPE doesn’t really have an OWW comp from last year, and the early leverage we’ve seen on cost savings YTD will only amplify the YoY impact into 3Q16.

HomeAWAY ahead of schedule: Prior to EXPE’s 2Q 2016 print we had highlighted that AWAY’s transition from a pure subscription model to a transactional model was both misunderstood and underappreciated. The 2Q release confirmed our work as AWAY’s robust revenue acceleration of +37% YoY vs. +17% in 1Q, and the positive color on the conference call served as a meaningful offset to their headline room nights miss. Additionally, management did a good job of mitigating fears of user base churn - highlighting that they had grown their online bookable listings inventory to 1 million, and reiterated that they are executing ahead of schedule. Further, the transition to a transactional model introduces a seasonality component that wasn’t there in 2015. Much of the +200% growth in AWAY online booking transactions in 2Q16 should flow over as revenue growth into 3Q.

Core Risk on the table: The Orbitz integration acted as an unintended bookings headwind in 2Q 2016, as internal mishaps may have limited the flow of its inventory to meta-search channels (non-recurring issue). Further, calendar timing issues appeared to have pulled forward booking volume to 1Q16 out of 2Q16, exacerbating the YoY growth deceleration we saw in 2Q. All in, both these issues are largely non-recurring, and more importantly have lowered the bar for expectations for the remainder of 2016. Granted, headlines will affect intra-quarter trading, but despite softening macro trends, EXPE should be a relative outperformer vs. hotels and definitely Hotel REITs given its higher proportion of leisure travel, which is slower to react to softening macro trends. Finally, EXPE’s merchant model limits cancellation risk should demand soften on any sudden negative events (e.g. Brexit, terrorism, etc.).

LONG TERM (TAIL)

EXPE’s potential stock price appreciation (over the longer term) will be contingent upon the company’s ability to show continued progress out of both the Orbitz and HomeAway integration. So far, we believe management is effectively controlling each of these stories, especially in 2016. But we will be reassessing the setup for 2017 moving forward.

ONE-YEAR TRAILING CHART