THE ZEITGEIST: SEPTEMBER 12, 2016

9/11. The precedent has emerged that on September 11 presidential candidates shut down their campaign ads and media appearances in order to showcase America’s unity in face of adversity. Despite a bitterly polarizing campaign season, that new tradition was followed yesterday on the fifteenth anniversary of the event. Both Clinton and Trump showed up the Trade Tower ceremony, watched respectfully, and said nothing to the public. Politics did however intervene when Clinton felt faint, left early, and was put on antibiotics for pneumonia by her doctor. While Trump declined to comment on her early departure, Trump supporters for the last several weeks have been raising questions about Clinton’s overall health.

DO WE COUNT WORKERS OR HOURS?

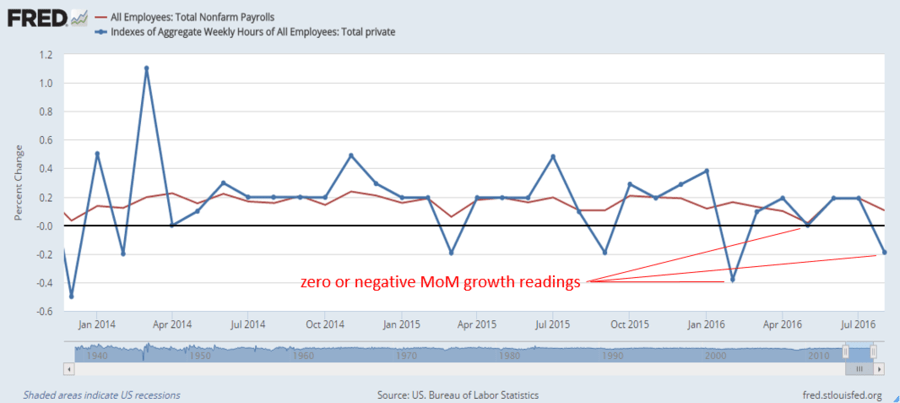

According to the media consensus on the BLS employment report a week ago, the +151,000 added NFP in August was a good if not great number. Admittedly it’s not up to the monthly average of the last two calendar years, 2014 and 2015, when the NFP growth number averaged +220K per month. But that’s OK, we are told, because it’s inevitable that this body count delta will shrink as employment approaches its natural limit (whatever that is) as a share of the labor force (whatever that is). All told, +151,000 represents “continued progress.” Many economists chimed in that it exceeds the number (around +120K, depending on how you calculate it) required to keep employment constant as a share of the population.

If we look at worker hours rather than workers, however, a different picture emerges. This is because average weekly hours have lately been tumbling. In August, for example, average weekly hours dropped from 34.4 to 34.3 hours per week, or by nearly -0.3%. This transformed a +0.1% employment gain (the 151,000 new bodies) into a -0.2% change in aggregate hours worked. And we’re not just talking about August. Since the December of 2015, while employment has gained by 0.13% per month, aggregate hours have gained by 0.06% per month—less than half the growth rate.

In fact, aggregate hours growth has been zero or negative in three of the last seven months, while employment growth has always been positive.

The gap between these growth trends is precisely accounted for by the steep decline in average weekly hours since the beginning the year. You’d have to go back to 2011 to find a month in which average weekly hours was lower than August’s 34.3. The full decline in average hours since January is -0.87%, which is the equivalent of nearly one million workers assuming unchanged average hours.

Most economists regard worker hours, not workers, as the fundamental unit of labor which drives GDP. So when average hours rapidly change, we need to re-adjust our thinking: Maybe the employment situation is not as “warm”—not even as Goldilocks “warm”—as everyone is telling us.

What’s behind the average-hours drop? Perhaps it’s the rising share of workers in the service and retail sectors, which have long experienced a lower and faster-declining average work week. Also, as I have argued for the last several months, the rise of the “gig economy” is certainly playing a role--everything from permatemping by 20somethings to Uber driving by 60somethings. A growing minority of semi-employed Americans is starting to pop in and out of the economy on shorter work schedules, significantly pulling down the national average. If the employment outlook were really as strong as the media suggest, we should be seeing enough workers putting in longer hours to more than compensate for this decline. But we’re not.

Principal component analysis indicates that average weekly hours is a strong cofactor in explaining the overall labor market strength. The Fed gives it a strong weight among its 19-factor Labor Markets Conditions Index (LMCI). Yes, that’s the index which has been favored and promoted by Fed Chair Janet Yellen—and which, not coincidentally, has been performing poorly this year. (In August, the change in the LMCI again went negative.)

More seriously, average weekly hours shows a fairly reliable business cycle pattern. It generally rises steadily during expansions, peaks at the expansion peak, then falls during recessions. For those of us who have been waiting (thus far in vain) for the typical expansion peak signals—not just in average weekly hours, but also in average wage gains, temp employment, employment ads, and so forth—we are beginning to see some disconcerting evidence that all these peaks may not be ahead of us after all. They may already be behind us. Over the next couple of months, average weekly hours will merit our close attention.

WAITING FOR THE APPLE TO FALL

On Wednesday, CEO Tim Cook unveiled Apple’s new product line—and wow, it totally underwhelmed. The biggest new iPhone 7 feature was the removal of a feature (no more audio jack). The other improvements were narrow gauge (a somewhat better battery life and a fancier camera). Oh, and yeah: Apple wants its new iWatch to go head-to-head with FitBit. Good luck with that. Cook is also pushing new growth in services—everything from digital music (where no one is making any money) to education platforms and cloud capacity (ditto).

Here’s the bottom line for Apple. Every one of its major product lines is now showing declining revenues, both sequentially and YOY. It’s flagship iPhone product (accounting for over half of total revenue) has reached saturation in the high-income world and has little chance of strong penetration into the developing and market economies with so many low-priced producers of quality phones (like Samsung, Huawei, and Xiaomi) entering the mix. And all this is in an industry where profit margins (outside Apple) are paper thin or negative and competitors are hungry for market share. What’s more, the telecoms are no longer subsidizing Apple customers by helping them buy their phones.

Sure, Apple is a popular prestige brand that will continue to generate tons of cash for years to come. Its historical ROIC has been stellar (thanks, Steve), making it one of the epic momentum stocks of all time. Millions of people will continue to buy expensive iPhones for the same reason they still buy Microsoft software: path dependence. No one wants to bother to relearn something that’s very complex and that seems to work pretty well. Moreover, Apple does have some positive if speculative opportunities on its horizon, such as using Apple Pay to achieve growing dominance in the credit card/payments sector or leveraging its early starring role in the spread of augmented reality apps (see: Pokemon Go!).

But the bottom line is that Apple’s sales are declining without any certainty of a turnaround in an IT device world in which consumer preferences can shift rapidly and all the fundamentals can shift rapidly with them—market share, profit margin, and economies of scale. Does Apple, under Tim Cook, really have a second act? This is a company—unlike Samsung—that spends less on R&D than on patent lawyers. Does a P/E over 10 really make sense for a firm with a negative PEG ratio? On the FAANG hierarchy of strategic opportunity, I now put Apple in last place. Let me spell it like this, best to worst valuation: ANFGA. The first “A” of course is Amazon.

TRUMP RESURGES

It may just be the yin and yang flow of campaign energy. Or Trump’s unexpected string of strong and “presidential” speeches (about immigration in Mexico City; to “values voters”; and on national security). Or Clinton’s recent mishaps, most recently her overreaching reference to Trump voters as a “bucket of deplorables.” It may also be due to a more disciplined focus by the Trump campaign, now under Steve Bannon’s leadership, on Clinton’s weaknesses.

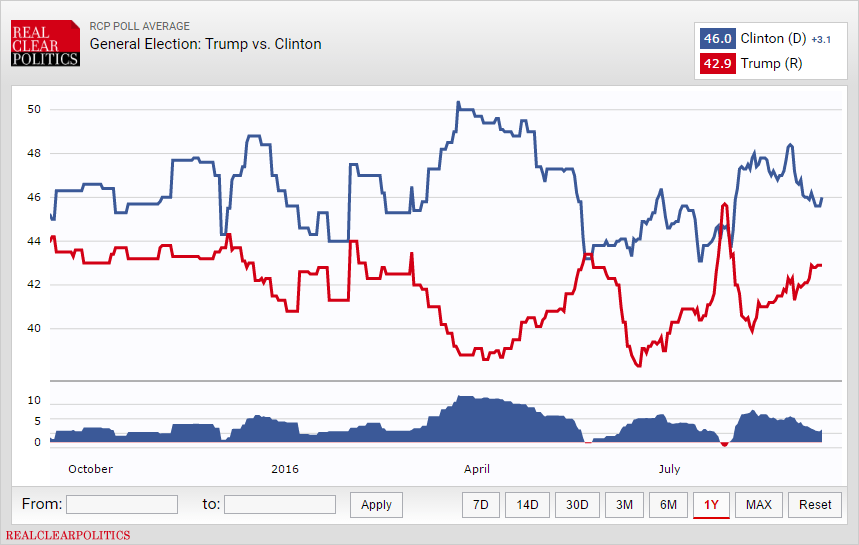

Whatever the reason, the opinion tide has shifted back in Trump’s direction. In mid-August, at the lowest point, Trump trailed Clinton by 7 to 8% points in the survey averages. Today, according to the latest indexes from The New York Times and RealClearPolitics, Trump trails by 2 to 3% points.

Back then, the futures market odds were up around 75-25 Clinton. Now they are back to 66-33 Clinton, according to PredictIt. Hypermind, the superforecasters’ future market, now puts the odds at 56-42. The big-name analytical forecasters have also been rejiggling their numbers. Nate Silver’s FiveThirtyEight now says the race is 70-30. And the New York Times, as ever marking the pro-Clinton edge of the odds bracket, says it’s 79-21, which is the first time it has put Trump above 20 in more than a month.

As the national polls tighten, so do the polls in most of the swing states: including Ohio, Florida, Pennsylvania, Virginia, and North Carolina. While state-watching is entertaining, it is unlikely to generate further insights on the outcome since (as I’ve pointed out before) the odds of electing a President who loses the popular vote are so historically remote. Nate Silver adds that, should this happen in 2016, it may be more likely to go Trump’s way. This is because Trump, compared to other recent GOP candidates, actually has smaller margins in the deep red states that will almost certainly go for the GOP in any case. Holding the national results constant, this means Trump may get more support in the midwestern battle states he so desperately needs to win.

To be sure, Trump is still behind. But now that he’s within striking distance, the upcoming candidate debates loom very large in importance. According to a new Washington Post-ABC News poll, his odds may be further helped by the relatively large share of voters (30%) who remain undecided—and by the higher share of Trump supporters who say they are “absolutely certain” to vote. In this respect, at least, the race may resemble the Brexit vote.

NewsWire

- Recent statistics show that fewer Japanese youth are joining the bosozoku gangs, “rowdy [uniformed] youths that blatantly and conspicuously break traffic laws… usually while riding motorcycles.” While some investigators say that this is due to young people hating “hierarchical relationships” in gangs, it’s more plausible that Millennials just want to follow the rules and avoid unnecessary risks. (RocketNews24)

- Columnist Alina Tugend highlights the growing market for personal memoirists who can document the life stories of people in old age. She misses a key generational driver behind this industry: Personal memoirs appeal to family-centric Boomers who are intent on passing on their values (and their family history) down to future generations. (The New York Times)

- Amazon is reportedly pursuing the rights to stream live sports such as tennis, soccer, and golf through its Prime Video service. If successful, Amazon would be chipping away at the last stronghold of traditional cable companies: live sports broadcasts. (Bloomberg Business)

- UC Berkeley professor Alison Gopnik outlines a recent Child Development study that argues that protecting children from saws and knives can actually hurt them in the long run by creating exaggerated fears. Despite these findings, protective Xer and MIllennial parents aren’t likely to allow their Homelander children to play with scissors or a set of matches unsupervised anytime soon. (The Wall Street Journal)

- This fall, Vera Bradley is overhauling its product offerings and redesigning its stores to win over older Millennials. Amid slipping sales, the brand known for its colorful cotton purses is hoping that leather offerings will appeal to young professionals who want to be taken seriously at the office. (The Washington Post)

- Columnist Keith Humphreys notes that 45- to 54-year-olds and the 55+ are getting arrested much more than people the same age were 20 years ago. Although he overlooks Xers, he does make a solid point: “[Boomers], who drove up the American crime explosion in their youth, are apparently continuing to outdo prior generations in their late-life criminality.” (The Washington Post)

- An upcoming House subcommittee hearing will investigate how the nation’s colleges are addressing soaring tuition costs, and will determine what further action needs to be taken. One plan would create a fund to help middle-income families pay tuition bills, with the money coming from school endowments. (Bloomberg Business)

- What started as a Boomer-Xer joke, #howtoconfuseamillennial turned ugly when lighthearted jabs gave way to intense criticism. However, young people quickly caught on and turned the hashtag around, as one Millennial caught in the crossfire tweeted: “#howtoconfuseamillennial have them wake up Sundaymorning to a hashtag like this where you vilify them for no reason.” (Cheezburger)

- Many job seekers over age 40 are taking drastic steps to land Silicon Valley gigs, like wearing sneakers to interviews or even having plastic surgery to look younger. Out-of-work Xers and Boomers—many of whom need the money to ensure a comfortable retirement—are forced to compete in the “dressed-down,” youthful world of Silicon Valley tech. (Bloomberg Business)

- In a new Oscar Mayer back-to-school commercial, kindergartners take a page from Mom’s playbook by leaving comforting notes in their parents’ lunches. Homelanders who have been taught the art of self-regulation are now often the ones providing emotional support to their own parents. (MediaPost)

Did You Know?

Big Alcohol Goes Healthy. The nation’s foremost breweries and distilleries are going on a health kick. In May, Boston Beer (maker of Samuel Adams) released Truly Spiked & Sparkling, made using fermented cane sugar and natural flavors. MillerCoors has invested in two of its own natural drinks—Easy Tea and Zumbida Mango. Meanwhile, Diageo will soon unveil its 90-calorie, gluten-free Smirnoff Spiked Sparkling Seltzer line. These firms are prioritizing not only low-calorie, natural offerings, but also transparency: Member companies of industry trade group Beer Institute—which include MillerCoors and Anheuser-Busch InBev—will soon list detailed nutritional information on product labels. The movement is designed to appeal to today’s consumers, especially Millennials, who make health a part of their day-to-day lifestyle. As AB InBev marketing executive Valerie Toothman points out, “There’s a reason you see people in yoga pants all over New York City…It’s this idea that a kind of health and well-being is the new premium.”

Ugly is in Stock. Cosmetically challenged produce is in: Starting this week, Walmart will begin selling weather-dented apples at 300 of its Florida locations. The move is hardly a one-off. Back in April, the retailer started marketing “Spuglies” (a brand of misshapen potatoes) in select Texas stores, while its U.K. chain began selling “wonky veg” boxes filled with 11 pounds of misshapen vegetables earlier this year. Other grocers have also gotten onboard: In April, Whole Foods began a pilot program to sell visually unappealing fruits and vegetables in many Northern California stores. In one respect, the trend is an effort to curb food waste: Blemish-related losses can hit as high as 30 percent for items like apples. But the move also spans beyond the produce aisle. As we’ve written before (see: “Ugly is the New Beautiful”), everyone from restaurant chains to beauty companies has been touting the unpolished nature of products designed to appeal to authenticity-driven shoppers.