Since Japan is the playground of central planners and economic orthodoxy, here's some of the more interesting recent developments out of Japan that should give pause to any honest economist (oxymoron?) or investor.

"Japanese companies are expected to issue 3.3 trillion yen ($32.9 billion) worth of bonds during the three months ending in September, double the amount from the year-earlier quarter, as businesses capture demand from yield-hungry investors to finance growth spending," Nikkei reports.

Clearly, Japanese companies are taking advantage of the country's interest rates hanging out near record lows. Take a look at Japan's steadily pancaking yield curve.

Got #GrowthSlowing?

The Failure of Central Planning...

A survey of Japanese companies conducted after Prime Minister Shinzo Abe announced the 13.5 trillion yen fiscal stimulus package reveals unsurprisingly underwhelming expectations:

"Less than 5 percent of companies believe the steps will boost the economy near-term or raise its growth potential, according to the Reuters Corporate Survey, conducted August 1-16... Corporate Japan was also cautious about fresh monetary stimulus, with over 60 percent saying the BOJ should not ease further or should even start to wind down its massive stimulus."

Interestingly, in the open-ended portion of the survey, one general machinery firm wrote: "Helicopter money must be avoided." Clearly, Japanese companies aren't as sanguine as the hopes and dreams put forth by the country's central planners.

Macro markets have already sniffed out the folly of central planning. Pick your indicator...

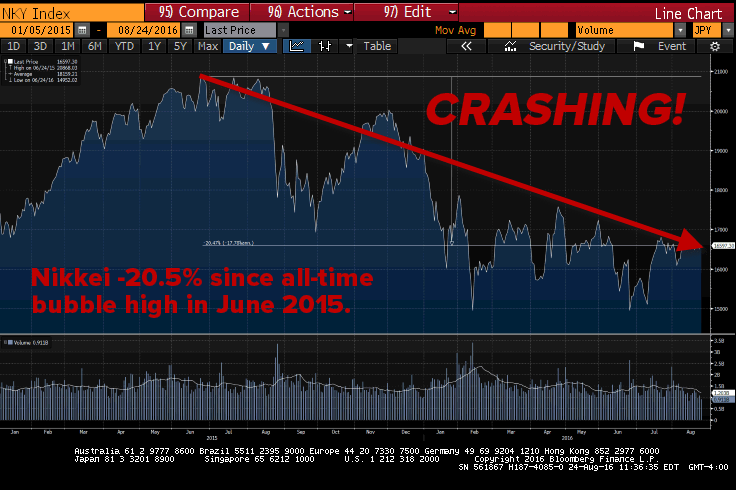

The NIKKEI Crash Continues...

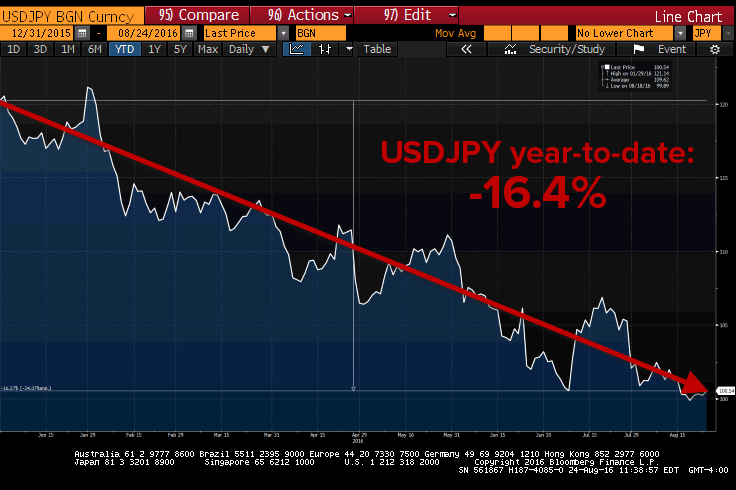

Or Yen strength...

(which according to economic orthodoxy should weaken with more stimulus)

How this ends is anyone's guess but one thing is clear, the Japanese people aren't happy with all of this meddling. And yet, the cries for more stimulus keep flowing.