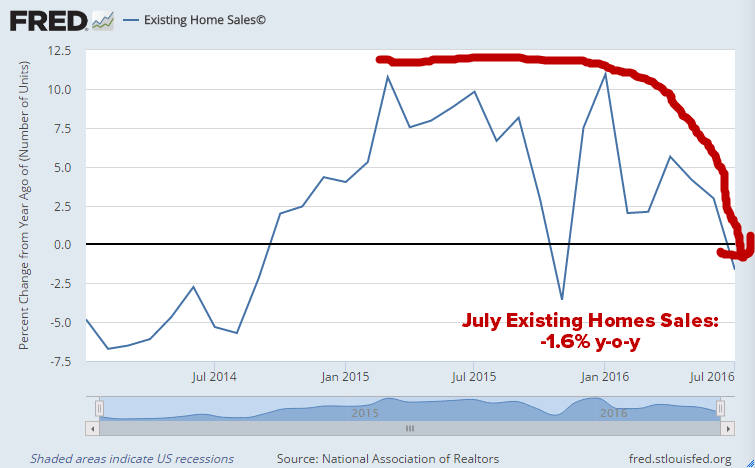

Today's Existing Home Sales data showed July down -1.6% year-over-year. That's the worst level of demand since November. That matters because EHS makes up 90% of total transaction volume.

We're not surprised by this month's EHS downside and were largely expecting a July slowdown. Here's what Hedgeye Housing analysts Josh Steiner and Christian Drake in an institutional research note on July 21 following the much ballyhooed June data (which was largely the result of a holiday distortion):

"In aggregate, growth in EHS slowed to +3.0% YoY but made a new cycle high at 5.57M units. The gain wasn’t particularly surprising given the trend in PHS and noise in the relationship between the two series (PHS vs EHS) stemming from the March Easter distortion. We’re more interested in next week’s Pending Home Sales data for June. Absent a moderate pickup and/or positive revision to May, the risk to EHS for July is to the downside."

In other words...

Additional thoughts...

QUESTION: How does declining Existing Home Sales fit into the hawkish Fed's rate hike calculus? Could they raise rates with 90% of the U.S. Housing market down 1.6% year-over-year?

ANSWER: Sure. They've been known to obfuscate the truth before.