Editor's Note: Below is a brief excerpt and chart from today's Early Look written by Hedgeye CEO Keith McCullough. Click here to learn more.

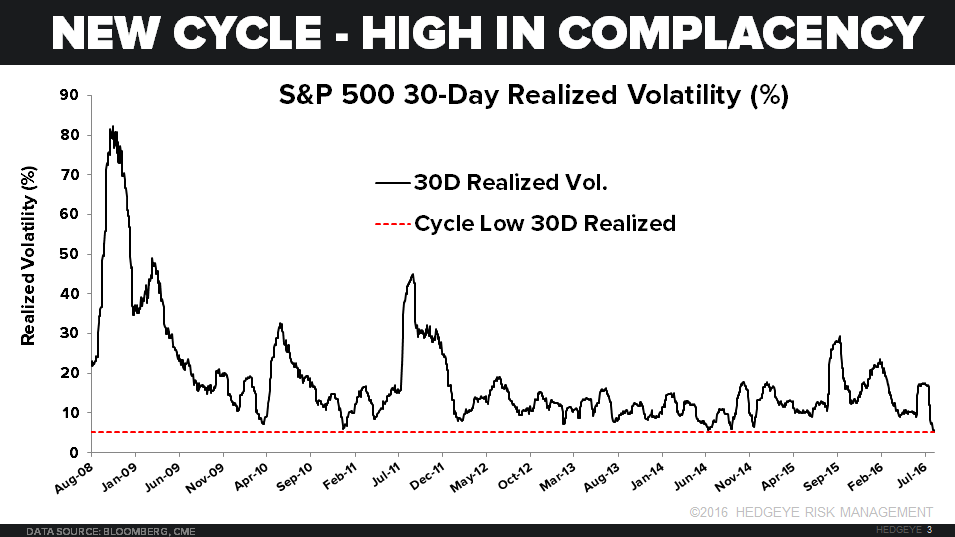

"... Looking a little deeper into how the latest all-time high in SPY has become:

- VOLUME: yesterday’s Total US Equity Market Volume (including dark pool) crashed -26% vs. its 1yr avg

- VOLATILITY: remained like a ball-under water (sub 14-15 on front month), sucking everyone back to VIX 10-11

- PRICE: SPY has only moved > +/- 0.5% in 5 of the last 31 trading days (will day 27 of complacency be today?)"