Here's a preview of the next issue of "About Everything." You're welcome to join a Hedgeye Q and A on credit cards next week, date and time soon to be announced.

What's the outlook for the credit card industry? When you look at the central players up close--focusing, say, on the latest revenue and earnings numbers for the key network providers (V and MA)--the outlook appears pretty bright.

But when you step back and take a broader view, several large warning lights appear. Let's start upstream, where growing price competition for consumers and retailers is forcing acquiring banks to cut back on fees, thereby pinching margins. Tellingly, the most "premium" brand of all (AXP) is now in real trouble: Hip hop and HBO stars are no longer bragging about their titanium black card. Then let's focus on today's frozen credit cycle, which is depriving the acquirers of the "revolver" interest income they usually enjoy as the recovery matures. Finally, let's look ahead to the seemingly unstoppable growth in debit cards, prepaid cards, and ACH as a share of all noncash payments. Or further ahead to the even faster growth in mobile payments.

What about opportunities abroad? Sorry, that window is closing as well. Indeed, there is growing worry about threats from abroad. If there is one specter that wakes up credit card executives in the middle of the night, it is the image of millions of 30-year-old Americans tapping on WeChat (the English-language version of "Weixin," the single most used mobile app in China). Looking ahead, some analysts already prefer to talk not of the credit card industry but rather of the "payments" industry.

Pushing all of these challenges is a strong and adverse generational tide. Quite simply, as you go younger than the 1970 birthyear, you will increasingly find Americans who don't like credit cards, don't like banks, and in fact don't really care for much of the financial services industry. A revolution is brewing.

Credit Cards Lose Their Charge

WHAT’S HAPPENING?

Credit card companies are on edge. In June, Synchrony Financial (SYF) warned of higher-than-expected defaults—prompting JPMorgan Chase (JPM), Wells Fargo (WFC), Capital One (COF), and Discover (DFS) to bolster their reserves for credit losses.

To be sure, these firms tell just a portion of the overall story. The credit card industry encompasses a wide range of players who assume various roles in the transaction. There are the “issuing banks”—like Citigroup (C), JPMorgan, Bank of America (BAC), and Capital One—that receive 1% to 3% of every transaction plus a base rate (often $0.05 or $0.10) depending on the type of card, what network was used, and where the item was purchased.

Then there are the “acquiring banks” (overlapping with the issuing banks) that process payments on behalf of the merchant. These companies earn a “merchant discount rate” worth between 1% and 3% of the transaction value.

Finally, there are the “networks”—Visa (V), MasterCard (MA), American Express (AXP), and Discover—that act as middleman skimmers between the issuing and acquiring banks. Though they make just a sliver of a percentage from each transaction (0.11% to 0.14%), these fees generate $30 billion annually for Visa and MasterCard, or a whopping 30 percent of their revenues.

On the surface, the industry should be thriving. General purpose credit card spending grew from 10% of GDP in 2000 to 15% in 2014. In 2014 alone, the number of processed transactions increased 10% YoY for Visa and 13% for MasterCard.

However, a closer look at the major players reveals some stark divides. While stock prices are up for most of the major networks (Visa, MasterCard, and Discover), they are down for American Express, a “premium” network whose business model may not survive in today’s newly price-pressured environment. They are also down for most of big issuing banks (like JPMorgan Chase, Bank of America, and Citigroup). To be sure, big banks globally have had plenty of bad news unrelated to credit cards. But look at Capital One, an issuing bank that makes most of its money from its credit card business—and whose stock has unperformed the S&P 500 since the Great Recession.

WHY IT’S HAPPENING

The credit cycle is stuck in a rut. After economic downturns, the industry only extends credit to individuals with excellent FICO scores. As time passes, companies gradually take on higher-risk customers with lower scores. These customers are more likely to carry revolving balances and pay higher interest rates—bolstering industry revenues. When these borrowers ultimately default on their debts, the customer base shrinks and the cycle repeats.

Or at least, that’s how it’s supposed to work.

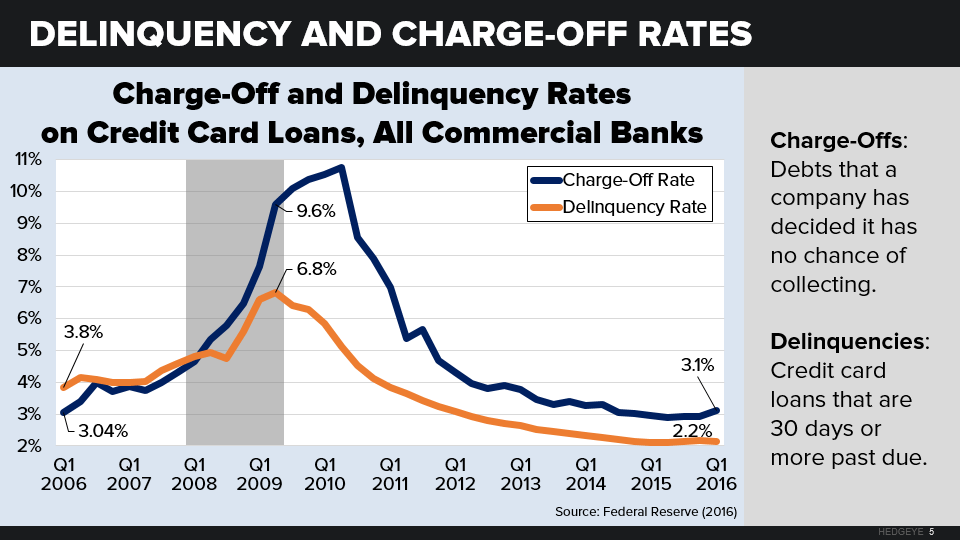

Today, as we might expect late in the economic cycle, credit card transaction volume by type of card continues to rise. Balances held by issuing banks are nearing their pre-recession peak, while charge-off and delinquency rates—though still at historic lows—are beginning to rise. Credit card default rates are on the rise as well, which is an indication that we’re nearing our peak number of credit card holders.

Historically, the compensating advantage for reaching full credit card capacity has always been a growth in interest payments from borrowers who don’t pay off their debts (so-called “revolvers”). But that isn’t happening during this cycle. In fact, the number of revolvers is actually falling, while the number of people who immediately pay off their debts (“transactors”) is rising.

In other words, credit cards are experiencing all of the costs of a late-cycle economy with none of the benefits.

Alternative payment methods are gaining ground. Sure, credit card transactions as a share of all noncash payments have remained relatively stable in recent years. But this situation likely won’t last.

Why? Credit card payments have held steady only by cannibalizing check payments, which have dropped off from 46% of all noncash transactions in 2003 to just 15% in 2012. There’s simply no more room for credit cards to grow.

Meanwhile, all other forms of noncash payments—prepaid cards, debit cards, and Automated Clearing House transactions—have become vastly more popular and their growth shows no signs of slowing. This is bad news for the industry, which takes a much larger cut from credit card transactions than any other type of transaction.

Mobile payment options are also giving credit cards a run for their money. Apple Pay currently takes a 0.15% cut of the 2% interchange fee, while other rivals like privately held LevelUp aim to get rid of fees altogether. Merchants like Starbucks (SBUX) and Walmart (WMT) have even developed their own systems that circumvent per-swipe fees.

While these “digital wallets” are working within the existing payment system for now—that is, cooperating with the networks—it’s the nature of technology to squeeze out the middleman in the long run.

GENERATIONAL DRIVERS

Both the stagnating credit cycle and the rise of competing payment methods have been driven by generational change.

Many Generation Xers and most Millennials don’t like being in debt or being punished with interest rates and fees. That goes double for the “prestige” of showing off your AmEx card—which, in any case, is losing any meaning in the era of online payment.

While older generations are comfortable paying off purchases over time, risk-averse Millennials would rather pay off purchases immediately to avoid ruining their credit score. It doesn’t help that the gap between credit card interest rates and interest rates on any other form of consumer debt has never been wider.

Together, according to Fed data, Xers and Millennials account for the vast majority of the drop-off in credit card use since 2008. (Xer credit card use was soaring before plunging steeply during the Great Recession, while Millennials have been moving away from credit cards since 2001.) Indeed, the percentage of adults under 35 who hold credit card debt has fallen to its lowest level since 1989. Many Millennials who watched their parents struggle during the Great Recession have long since cut up their credit cards—if they ever had them to begin with.

In fact, Millennials don’t want to take on consumer debt of any kind: While student loan debt continues to rise rapidly for young adults, every other form of indebtedness (housing, autos, as well as credit cards) is falling. As Millennial Rebecca Liebman stated, “I don’t want to use a credit card irresponsibly, and because of that, it’s scarier to use. I grew up—I saw 2008—I saw my dad get laid off. I don’t trust the financial market.”

More fundamentally, many Xers and Millennials don’t much like the banks who issue credit cards. A rising share of households headed by these consumers are either “underbanked” (rely on alternative financial services in addition to banks) or “unbanked” entirely.

Xers see financial technology startups as an attractive alternative to the banks that cost them their net worth during the Great Recession. Millennials, meanwhile, see them as a convenient part of their lifestyle: Why risk late fees and interest charges when you could use PayPal, LevelUp, and WeChat, apps that offer everything from easy bill payment to social networking?

The possibility that such mobile services might someday soon become as popular in America as they now are in China is a specter that haunts the credit card industry.

BROADER IMPLICATIONS

Credit card companies are pulling out all the stops to win over consumers. Most are making image tweaks to mimic their cool Silicon Valley competitors. MasterCard, for example, unveiled a new logo with lower-case letters to deemphasize physical cards as it shifts gears to digital payments.

Plenty of issuing banks are even cutting down on the number of fees they charge. Fewer are charging annual fees, foreign transaction fees, and balance transfer fees.

But it will take more than a new logo and a discount for Millennials to change their habits and give credit cards a chance.

Don’t expect payment networks to find long-term success abroad. For decades, one steady source of revenue growth has been to expand credit card use abroad—especially in developing markets. But that avenue may be closing.

In 2014, EU courts forced MasterCard to cap its interchange fees. Now, U.K. consumers are preparing a $24.5 billion class-action lawsuit against the company over its cross-border processing fees. Walmart Canada has stopped accepting Visa in three stores over “unacceptably high” fees. China did open its markets in June to foreign payment card companies—but not without implementing strict capital requirements.

The underdeveloped world is hardly a sound bet, either. Many late-developing countries won’t even go through a credit card phase. Countries in sub-Saharan Africa and southeast Asia are already leading the world in mobile payments. In 2013, a massive 43% of Kenya’s GDP flowed through M-Pesa. In the Philippines, where more than a third of the country’s cities and municipalities are bankless, there were 217 million mobile-phone transactions in 2013.

TAKEAWAYS

- The credit card industry is being squeezed from all sides. Growth in interest fee revenue is stagnating thanks to a frozen credit cycle, while alternative payment methods threaten to marginalize credit cards.

- The forces bearing down on the industry are being driven by generational change. Many Xers and Millennials are flocking away from credit cards and banks in general—and toward risk-free, convenient fintech options.