This evolving TGT/WMT relationship has all the makings of a backyard brawl. The only problem is…it’s not a fair fight. Don’t get us wrong – it could be, but as highlighted in our note following the TGT print (full note: TGT | Losing at Defense), we think the management team at Target is playing defense – badly. Think the ‘rope-a-dope’ without the Ali endurance or uppercut. That’s at the same time that the competitive dynamics around the retailer are evolving faster than at any point we can remember in large-cap retail.

In one corner you have AMZN scooping up 25% of the incremental dollars up for grabs in US retail – that’s 2x the rate we saw at the same time in 2015. In another corner is WMT, who saw a meaningful traffic inflection starting in 1Q14 and has been able to hold the upward trajectory for 2+ years as it invests its way to a flat earnings CAGR over the next 4 years. And in the 3rd corner there’s TGT, who has effectively managed expenses to hit near term expectations at the expense of long-term share, with no clearly articulated plan to win in any environment and a stunning lack of insight as to why the business is struggling in the face of otherwise solid prints by its two closest competitors.

In the series of charts below, we walk through what we think are the key callouts from the evolving TGT/WMT relationship and why we think TGT is the ultimate loser in this royal rumble. That will ultimately manifest itself in either a) lost market share and pressured margins taking earnings into the mid-$4s, or b) a meaningful reset in expectations as the company doubles down on the investment line to compete with its peer group.

WMT Out-Trafficking TGT

We positioned this chart first in the queue because we think it clearly demonstrates that WMT is winning what we coined the ‘backyard brawl’. To be clear, this is the effect and not the cause of the broader strategic decisions each team is making in order to ultimately drive traffic and win market share. There has been a clear deviation in the trend, with the spread between the two opening up to 1.2% in 1Q and 3.4% in 2Q, both in favor of Walmart. The most recent metric is good for the biggest spread we’ve seen since the TGT data breach in 4Q13, and the widest gap over the past 5 years in a normal environment. Most importantly, we don’t think this a near term statistical aberration, as WMT is putting the dollars behind the up-tick in traffic which will continue to propel outperformance while TGT sits on the sidelines.

Two Different Investment Cycles

This is the cause we referred to earlier, as we’ve seen a huge investment spread open up between TGT and WMT. It started back in mid-2014 around the same time Cornell started his tenure in Minneapolis, and has held steady at nine-points over the past two quarters. That’s important given that Cornell is now two years into his tenure at TGT, and now has his team and strategy in place. Based on what we’ve seen to date, it can be characterized by prudent decision making when it comes to cutting Canada/Rx biz and a reluctance to spend in order to keep pace with the competition. Ultimately, we think the spread between the two needs to change dramatically – and that’s not going to be gifted to TGT from WMT as the latter company has a free pass to invest after it lowered expectations 10 months ago. That means either TGT needs to open its pockets or be content with taking what comes its way.

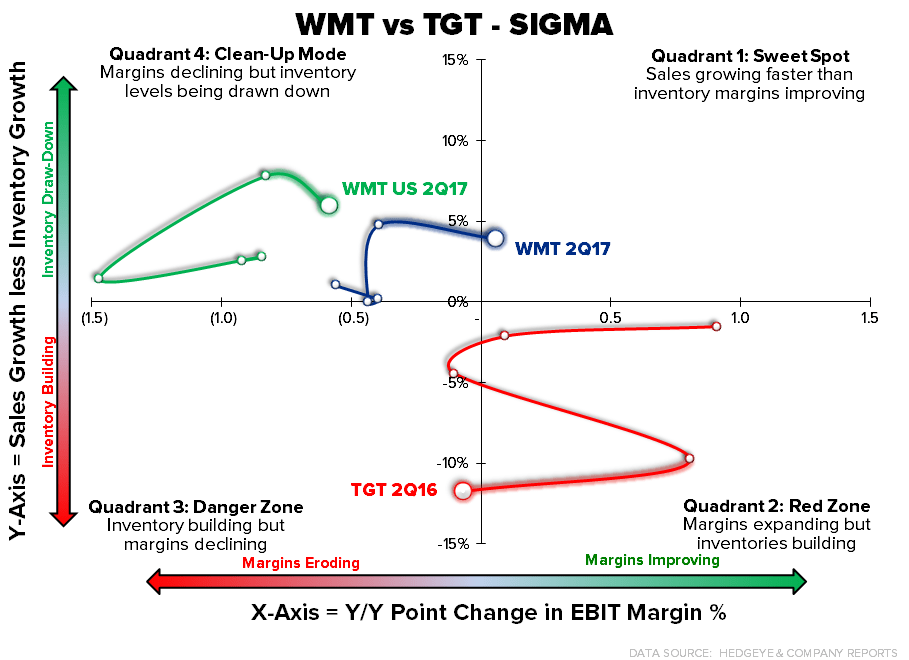

WMT Lean, TGT Bloated

The SIGMA trajectory for each company couldn’t be more different. For WMT: we are looking at a sales/inventory spread of 5% in the US which is a positive set-up for GM going forward and this leverage should continue to offset some of the SG&A pressure felt from investments. For TGT: inventories are building into a slowing sales guide, which we think could add additional pressure on GM in addition to the e-commerce headwind and promotional pressure already being felt.

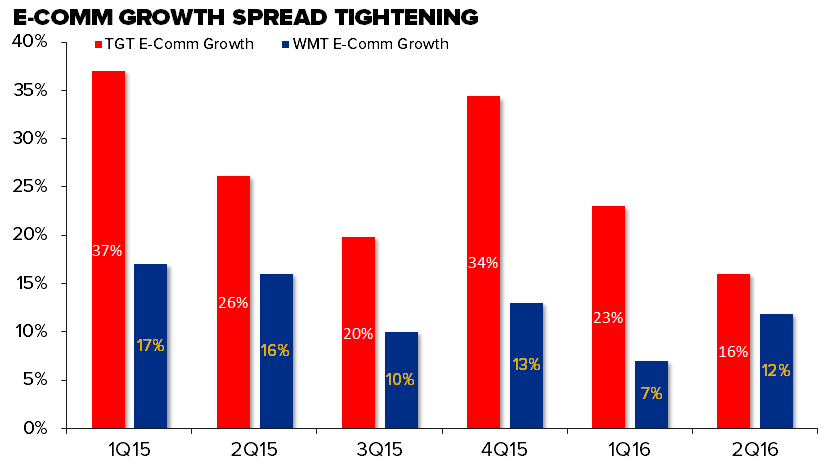

Win For TGT

This is the one metric where we will declare victory for TGT in 2Q. Though at 16% growth it’s not going to win a medal. There have been flashes of brilliance over the past 18 months for TGT, but not the sustained growth at a 40% CAGR that management thought was achievable 18 months ago. The key here is that while TGT continues to pull back on capital outlays to fund its e-commerce growth both on the P&L and the balance sheet, WMT went out and spent $3.3bn to acquire talent and technology in the form of Jet.com. The ante chip to compete for brick and mortar retail just went up tremendously.