Editor's Note: Below is a brief excerpt and chart from today's Early Look written by Hedgeye Senior Macro analyst Darius Dale. Click here to learn more.

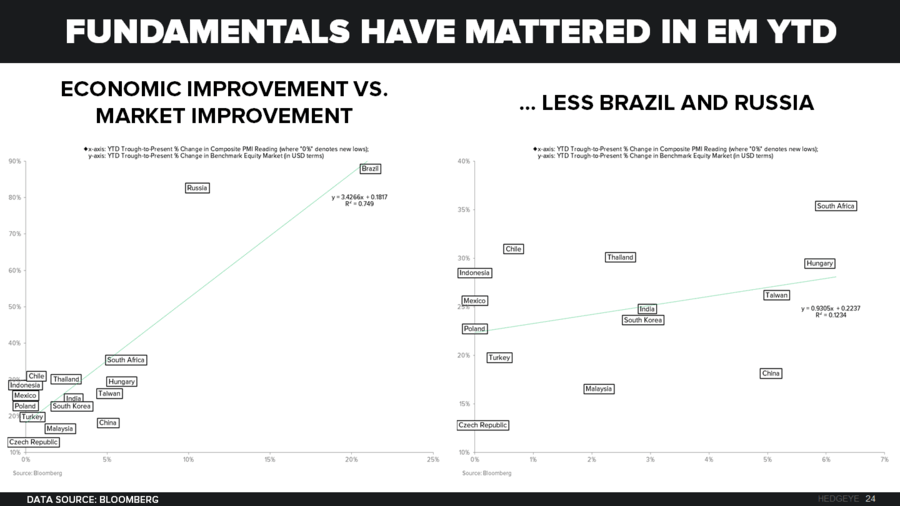

"For brevity’s sake, however, we’ll focus on one quick and dirty way to accomplish this, which is by regressing dollar-denominated equity market returns off of their respective YTD lows vs. the delta in composite PMI readings off of their respective YTD lows.

Does the market improvement match the economic improvement? If not, what is the probability the latter catches up to the former?

Regressing the aforementioned factors across the 16 emerging market economies we could find with available data yielded a positive correlation of +0.87. Even excluding outliers Brazil and Russia yielded a positively-sloping regression line with a correlation of +0.35 (see: Chart of the Day below for visualization)."