Below are our analysts’ new updates on our eleven current high conviction long and short ideas. As a reminder, if nothing material has changed in the past week which would affect a particular idea, our analyst has noted this. We will send Hedgeye CEO Keith McCullough's refreshed levels for our high-conviction Investing Ideas in a seperate email.

IDEAS UPDATES

TLT | GLD | UUP

To view our analyst's original report on PowerShares DB US Dollar Index Bullish Fund click here and here for Gold.

Eurozone GDP, reported Friday, signaled more of the same, stagnation. With that being said there were small but marginal Euro tailwinds against a U.S. retail sales report and PPI release that was likely dovish on the margin (USD -~20bps on Friday and -~60bps on the week).

In line with our #EuropeSlowing theme, Q2 preliminary GDP slowed across the Eurozone to +0.3% vs. +0.6% in the prior quarter and +1.6% Y/Y for Q2 which was flat on a rate of change basis from Q1.

Looking at specific country results:

- German (0.4% vs 0.7% sequentially) GDP accelerated to +1.8% Y/Y from +1.6% which was probably a minor Euro FX tailwind

- Italian GDP came in at +0.7% Y/Y which was a deceleration from +1.0% in Q1

- Greece GDP accelerated to contraction again, printing a measly -0.1% Y/Y from -1.3% in Q1

- The Southern Eurozone states continue to implode

Recall that a strong retail sales report for June, driven by a positive trend in goods consumption, was a large contributor to our GDP revision for Q2. The headline number, for June, was up +0.6% sequentially with the sequential acceleration in the control group accelerating +7.2% (annualized).

Friday’s retail sales report was a different story, and probably a dovish data point for the USD on the margin :

- The control group printed flat sequentially, +0.0%

- Retail sales ex. auto and gas printed -0.3% sequentially

Next to retail sales, July headline producer prices decelerated -0.4% vs. +0.5% in June sequentially and -0.2% Y/Y vs. +0.3% Y/Y in June. PPI ex. food and energy came in at 0.0% sequentially vs. +0.4% in June and +0.7% Y/Y from +1.3% in June. #Deflation

Overall it was a sleepy summer week for the most part. But don’t get complacent with all-time equity index market highs and a near re-testing of all-time lows in volatility. The VIX is just one-handle from its summer 2014 all-time low. Meanwhile, the Treasury bond volatility index is now at a level not seen since December of 2014. Like the set-up in Q3 2014, when we introduced our theme of #Volatility’sAsymmetry, it’s a one-way street off all-time highs in complacency.

HBI

To view our analyst's original report on Hanesbrands click here.

Hanesbrands (HBI) is facing bloated inventory levels. In 2Q, it spent an incremental $12mm on inventory reduction initiatives, but hey, the inventory clean-up plan is tracking according to plan… right?

Nah, not even close.

The sales-to-inventory spread only went from -16% to -14% after adjusting for the $51mm increase created by the closing of Champion Europe around quarter end. This high inventory level means organic growth and margins are likely to be under pressure as the level normalizes.

ZBH

To view our analyst's original report on Zimmer Biomet click here.

We know at this point that hospital admissions have slowed to ~0% year-over-year. We also know that Healthcare job openings are now growing at the slowest rate in over 2 years. We know too that Nurse layoffs and discharges have spiked to growth rates not seen since the financial crisis in 2009.

Now, will this impact orthopedic surgery?

We think so, but know we have been wrong in the last year. If the relationship holds and inpatient surgeries, which are dominated by orthopedic cases and affected by the #ACATaper, drives hospital admissions into negative territory, we will see this show up in Zimmer Biomet's (ZBH) results.

At a minimum, ZBH has closed much of the multiple gap between their stock and SYK, at least taking out one leg of the long thesis. Additionally, 2Q16 earnings season was one of the worst in 5 years and the multiples investors are willing to pay for healthcare stocks and the S&P 500 Healthcare Index generally, as growth continues to deteriorate into 3Q16 and 4Q16, will continue to come in as well. That should take ZBH’s multiple lower from here.

LMT

To view our analyst's original report on Lockheed Martin click here.

Friday, Lockheed Martin (LMT) closed up $1.61 within $1 of its 52-week high spurred by news that the Pentagon is releasing nearly $1B to pay for work already performed by LMT on 57 Low Rate Incremental Production (LRIP) Lot IX F35 aircraft ordered in FY 2015 but still not yet on contract. The money comes via an Undefined Contract Action (UCA) which allows payment by the Government for ordered work that has been completed but not yet finalized in a contract.

In its Q2 earnings report, LMT announced that it had spent nearly $1B of its own funds to keep Lot 9 production on track and suppliers on board and that it was approaching its tolerable limit while negotiations drag on. Usage of UCAs and dependence on LMT’s access to cash has essentially enabled annual F35 negotiations to be perennially dragged out and has become the unfortunate norm in the F35 program. The Government and Lockheed have been negotiating ~140 Lot 9 and Lot 10 orders as a package worth nearly $14B for over a year. The first Lot 9 aircraft are due to be delivered in late 2017.

While there is no specific information as to why these particular negotiations are dragging out, the F35 program is nearing completion of development with the commencement of full rate production and the first multiyear contract planned for 2019. LRIP contracts between now and 2019 thus take on greater weight since they will form the negotiating basis for what will probably be a series of five year multiyear contracts.

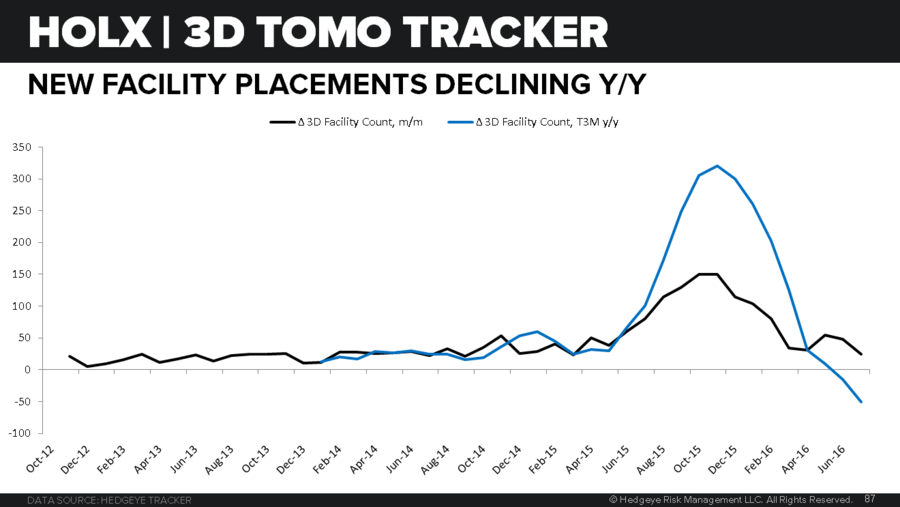

HOLX

To view our analyst's original report on Hologic click here. Below is an excerpt from an institutional research note written by Hedgeye Healthcare analyst Tom Tobin.

HOLX | 3D TOMO-TRAcKER UPDATE | PLEASE DEFINE "TOUGH COMP" AND OTHER LESSONS IN NARRATIVE CONTROL

SUMMARY

Hologic (HOLX) management described future growth available to 3D Tomo adoption as "stronger for longer" on the F3Q16 earnings call. It was a clever marketing tag line that soothed investor concerns about F2017 growth after concerns emerged with F2Q16 earnings and the "Tomo-Cliff." But "stronger for longer" will come after a diminutively termed "tough comp" for 3D Tomo in the upcoming F4Q16.

Based on our data (charts below), we'd describe management's "tough comp" as "reputation breaker," "disaster," "major fail," or any number of alternatives that capture the moment when investors realize Hologic's growth and margin prospects for 2017, as well as the truthiness of the management, are not as good as they believed. After the stock price debacle of F2Q16 driven by the weak results and the narrative of the "Tomo-Cliff," the "stronger for longer" and vigorous denials made by management over the course of F3Q17 have provided what we see as only a temporary reprieve, and what looks like a suspension of reality.

TOMO TRACKER IN DECLINE

The year-over-year change in facility counts has turned negative through July 2016 and appears likely to remain negative for some time. As we described in our Black Book presentation, declines in 3D will put significant pressure on gross margins and company growth going forward. The number of facilities converted to 3D according to MQSA, which recently began disclosing 3D facility and unit placements, would further suggest HOLX is conceding market share in recent months after dominating the market for 3 years. Consensus Breast Health revenue is at $290M for F4Q16 versus $286M a year ago, and $283M last quarter. We see steep declines as far more likely.

LAZ

To view our analyst's original report on Lazard click here.

Year-over-year corporate credit costs remain at elevated levels which is limiting merger and acquisition (M&A) announcements and continue to outline a short case for the boutique M&A advisors. Although credit costs have compressed slightly with 10 year Treasury yields recently, a 4-quarter moving average of corporate funding has only improved marginally, which continues to create negative comps for M&A through July.

Until funding costs decline substantially we are comfortable with our ongoing short recommendation on Lazard (LAZ) and the boutique advisory group overall. Forward earnings estimates for LAZ and the group still do not reflect the extension of negative comps into the second half of 2016.

TIF

To view our analyst's original report on Tiffany click here.

We have been watching Macy's to get a sense of TIF sales within its Americas segment. Macy's reported second quarter earnings this week and comps improved sequentially. This would appear to be good for Tiffany (TIF), but as the below chart shows, there is already the expectation of improving comps for Tiffany similar to that of M.

Macy's noted that tourist sales improved vs 1Q, but were still down double digits year-over-year, so the tourism headwind remains.

TIF may be able to hit the relatively low expectations in its upcoming quarterly earnings, but we don’t believe the back half acceleration that management and the street are looking for will ever materialize. EPS expectations for the next 12 months need to come down.

FL

To view our analyst's original report on Foot Locker click here.

Foot Locker (FL) reports 2Q earnings on Friday, August 19th. We feel there is a high probability that FL will see a significant miss or guide down before the books are closed on 2016.

Expectations are high in the quarter with the Street looking for 3.7% comparable sales growth, when management reported May was running negative as of the 1Q conference call. To beat numbers given at the start of the quarter, FL will have to see one their biggest intra-quarter accelerations ever. The bulls have pointed to strong Jordan shoe launches as a postitive but we're not convinced they will be enough to offset declines in the rest of the business. Even if we are reading this completely wrong and the Jordan launch success creates the needed boost, how does FL replicate that in the back half and hit numbers against compares that are just as hard, if not harder?

We remain short FL on all durations.

WAB

To view our analyst's original report on Wabtec click here.

No update on Wabtec (WAB) this week but Hedgeye Industrials analyst Jay Van Sciver reiterates his short call.