"You can't put a limit on anything. The more you dream, the further you get."

-Michael Phelps

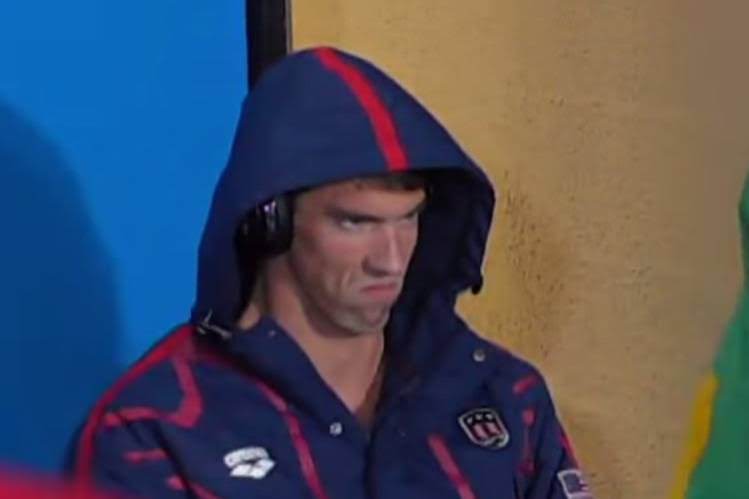

The bear was poked at the Olympic Games in Rio earlier this week. A South African swimmer foolishly decided to taunt Michael Phelps before the 200 meter butterfly semi-final. Specifically, Chad le Clos cockily shadowboxed and danced right in front of Phelps.

In the middle graphic below, we feature the stare down that Phelps gave his opponent before the race. The look is very clear: le Clos had poked the bear. No surprise the bear awoke and responded in kind by crushing his competition in the race to win gold in the event.

With that win, Phelps broke an Olympic record for individual medals in a career. The record was previously held by Leonidas of Rhodes who set the record more than 2,000 years ago. Over the course of his Olympic career, Phelps has won (so far) 25 medals. Not a bad career, Mr. Phelps.

Back to the Global Macro Grind…

The SP500 is currently up about 6.4% on the year. Within that, sector performance has been very diverse. One of our favorite sectors, Utilities, continues on a gold medal pace and is up more than 17.0% on the year. Meanwhile, the Financials sector is picking up the rear and is up barely 0.2% in the year-to-date.

As we all know, not dissimilar to the Olympic Games, there will be plenty of performance surprises before the end of the year. One sector we have front and center in that regard is Energy. Currently up 11.6%, admittedly after having a dreadful year last year, energy has the potential to finish out of the medals as supply and demand turn bearish.

On the supply front, our colleague Joe McMonigle, formerly Vice Chair of the International Energy Agency, wrote a note yesterday addressing the fact that OPEC was unlikely to agree to any supply freeze. According to McMonigle:

"The same script is being used again after prices dipped into bearish territory in July. But the freeze proposal is again not serious because OPEC is producing at record levels. Ironically, OPEC's record July production of 33.41 million barrels a day is a major contributing factor in the current weakness in crude prices."

Take a look at this video from HedgeyeTV to get McMonigle's succinct thoughts on what OPEC might or, more likely, might not do. (Click here to watch.)

While supply has been an ongoing concern, the river card for oil bears through year-end may be demand. In OPEC's report yesterday, the cartel highlighted this fact that oil demand increased at lower than expect rates.

The IEA also tempered expectations for demand in 2017 on the back of economic growth slowing in 2017. While the Paris-based agency still has demand growth at historically healthy +1.2 million barrels per day in 2017, that will be lower than 2016 and below prior expectations. And in the oil markets, as in most markets, expectations are the root of all heartache.

Flipping back to the equities, the resilience of the SP500 has certainly surprised many-a-bear this year despite economic data generally coming in lower than most "pundits" predicted at the start of the year. On that front, the non-farm worker productivity numbers again highlighted dismal long-term growth prospects.

As we've highlighted in the Chart of the Day, productivity, which is a proxy for the goods and services produced each hour by Americans, has now declined for three straight quarters. As the chart shows, productivity declined both sequentially and year-over-year. This was also the first time since 1979 that productivity has declined for three quarters in a row.

To the extent you still believe the numbers being reported by the government, this is just another reason to accept that rates will be lower for longer. Without productivity gains, it is very difficult to see inflation, other than monetary inflation, increasing much, if at all.

On the topic of long-term growth and productivity, the United Nations came out with an interesting report yesterday on global aging. According to the report, by 2030 there will be close to 60 nations globally in which there will be more people over 65 than under 15. Interestingly, this aging phenomenon, of more 65-year olds than 15-year olds, began in a single country, Italy, in 1995.

In part, this increase in the older cohort is due to people living longer, which is a good thing, but in practice it also creates future imbalances in the economy. Productivity in aggregate will be lower as the less productive segment of society, those who are older and retiring, will be increasing. There will also be a shrinking workforce to support the growing retirement and pension costs.

In thinking about the really long term, governments will have few choices to get out of this quagmire - cut benefits, higher taxes, or borrow - and none of them lead to particularly healthy growth outcomes. We are such a believer in the long-term implications of demography, that we recently brought on renowned demographer Neil Howe to lead our research in the area. If you haven't met with Neil or aren't receiving his work, please contact .

In his book The Fourth Turning, published in 1997, Howe wrote the following:

"Wherever we're headed, America is evolving in ways most of us don't like or understand. Individually focused, yet collectively adrift, we're wondering if we're heading toward a waterfall. Are we?"

That's a sentiment that is certainly as true today as when he wrote it.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.44-1.60%

SPX 2154-2189

VIX 11.01-14.83

EUR/USD 1.09-1.12

Gold 1

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research