It was only 10 months ago that WMT came out and ripped the band-aid off at its Fall 2015 Analyst Day. There was a lot of detail embedded in that day (the transcript alone is 42 pages), but the key takeaway was that WMT wouldn’t hit 2015 earnings levels again until 2019 due to investments in three key buckets: Employees, E-commerce, and to a lesser extent, Price. While a struggling WMT has been a terrible barometer for all of retail, the company re-upped its commitment to the e-commerce bucket with the acquisition of Jet.com.

Let’s get it out up front and say that we think purchasing an unproven e-commerce business for ~6x sales, when AMZN trades at 3.7x, at the tail-end of an economic cycle is a poor use of shareholder capital. With that out of the way, we think that WMT just threw down the gauntlet for a second time to the rest of its competitive set, doubling down on the e-comm channel by bringing in outside assets. That lays down a precedent for everyone that the company competes against, telling its competition that WMT is willing to spend up in order to seek out new growth. We think the roadmap for the space from here gets increasingly more difficult as companies fight for dollars online and spend up to hold/win market share. That has obvious implications for TGT, KSS, M, etc.

Additional Details:

1) What’s Growthy? E-comm: This isn’t new insight by any means, but we think this provides a compelling visual to both a) explaining WMT’s decision to spend up in order to purchase talent/technology in the form of Jet.com and b) the need for the rest of retail to compete in the new e-comm arms race. In 2015, the average reported growth rate ticked down to just 1%. But what we think is even more damning to retail as we know it (or once knew it) is the fact that Brick and Mortar growth excluding e-comm went negative for the first time during this economic cycle and the spread between the two opened up to 3% – the widest margin ever.

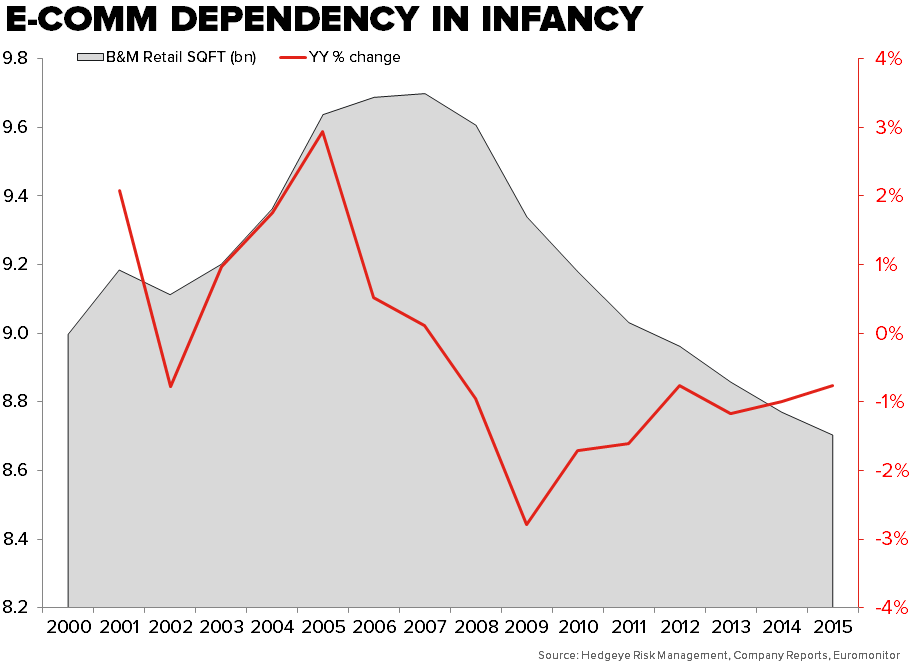

2) One Reason…Unit Growth Done: Outside of the consumers’ willingness to shop for a bigger percent of more categories online – the other obvious explanation for the bifurcation between reported growth and brick and mortar growth for traditional retail is that the sq. ft. has all but dried up. The decline in aggregate sq. ft. began in 08/09, but that didn’t trickle up the supply chain to WMT/TGT and mid-tier department chains until 2015. There have been periodic closings along the way (JCP, SHLD) but not to the extent we saw at the end of the last fiscal year in the form of a) Macy’s closing 40 doors about 4x a normal year, b) KSS closing 18 doors for the first companywide closing in history, and c) WMT closing 102 Neighborhood Markets and 52 Supercenters (the first closing since calendar 2006).

Fast forward to where we are today for WMT, and it’s pretty clear why the company made the decision to pay up 6x sales to buy Jet.com. Yes, AMZN is a threat and sq. ft. growth will never be part of the equation again, but WMT recognized that it had to shake things up after years of underinvestment in digital. Will it work? We’re not convinced that it will. But at the very least, WMT laid its battle plan down for everyone to see, and the rest of retail can either ante up or continue to lose relevance.

3) Margins A Consideration: By making this strategic decision, WMT all but confirmed where all of its growth could be attributed. Instead of sticking to the original build-it-internally plan, the company decided to bring in talent and technology to supplement what the company has been trying to build internally for 15 years. The difference here is that WMT, unlike just about every other competitor, has the balance sheet flexibility to absorb a deal of this magnitude without skipping a beat – we think it speaks volumes when we consider what type of investment is necessary from the rest of competitive set to keep pace.

From here, the setup for the space looks like this: i) net sq. ft. decline as concepts reconcile footprints and invest incremental capital to grow online biz, ii) brick and mortar growth continues to head negative with e-comm adding a buffer to prop up the top line, iii) margins head lower as companies continue to invest in e-comm precipitated by the moves from WMT and AMZN while deleveraging on the fixed cost of the vast store networks. We’ve already begun to see that roadmap take hold as the e-comm penetration ramped ~500bps over a two year time period after pretty measured growth from 2008-13. In turn, margins came off ~200bps as the reliance on e-commerce stepped up considerably.

That margin drag has been exacerbated by the fact that e-commerce has proven to be, for the most part, cannibalistic instead of incremental (despite what management buzz might suggest). That’s a problem when the e-commerce channel comes in at a gross margin well below that of a brick and mortar sales. In the case of KSS, there is an 1000bps delta between the two channels – a heavy headwind to absorb when there isn’t a lot of fat to trim on company expense lines now facing wage inflation. Layer on the need to invest in DTC now that WMT upped the ante, paints a pretty bearish picture for the margin trajectory of this space over the near and long term.

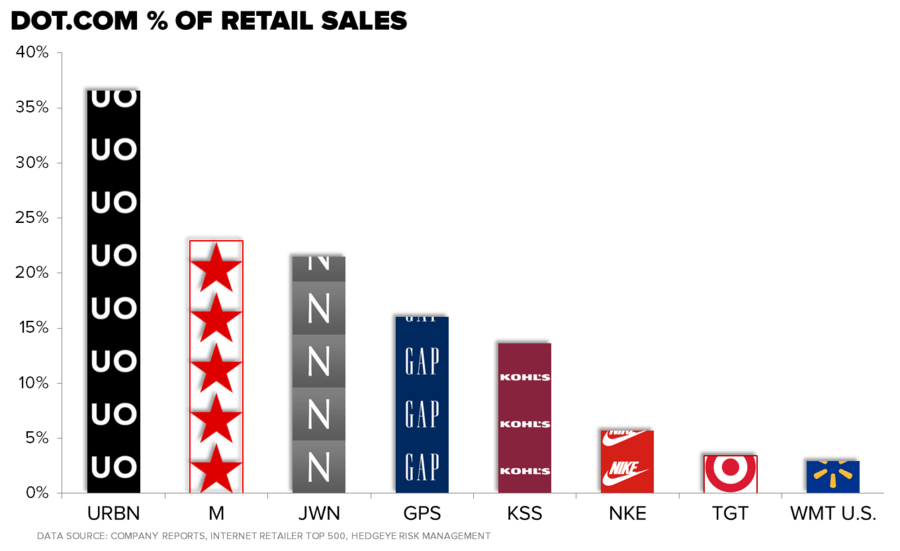

4) Its not just WMT That’s Far Behind: WMT has the lowest e-commerce penetration in the group, which the company all but confirmed provided the impetus for the Jet deal yesterday. Fair enough, but the company isn’t the only laggard in the space. The obvious callout is TGT, with sales penetration in the ballpark of WMT-US, and well below 5%. TGT already backed off it’s 40% online growth CAGR targets it articulated at the 2015 Analyst day, and talked down the need to invest more heavily in that channel back in March. The WMT decision to spend up is the new data point, and we think the combination of pressure at both ends of the spectrum – WMT on the low end, AMZN on the high end – will make incremental growth from here more difficult. And that’s not just for TGT. As everyone (KSS, JCP, M) that competes with WMT/AMZN in this space must continue to invest in the direct channel in order to keep its share of the market.