“After the Show is the After Party”

-Jay-Z

My after-party life is past peak.

I’ve had some solid late night sessions with some unlikely characters ….. DMX, Dave Chappelle, Snoop Dogg, Pat Morita (Mr. Miyagi), that homeless guy I always used to see down the street ….

I’m pretty sure I wasn’t even old enough to be where I was for some of those but no harm, no foul and all that. Life is a collection of moments and I’ve made an effort to amass a menagerie of covetable memories.

The after-party can be the funnest part of the night.

It’s also the nursery for ill-conceived antics and subsequent regret.

Back to the Global Macro Grind…

We’ve been on this whole #GrowthSlowing thing for ~6 qtrs now.

Frankly, it’s getting kind of lame. Not wrong or unprofitable, just progressively less exciting.

My enthusiasm is stagnating, secularly.

Over those 6 quarters, there’s been a certain recurrent rhythm to my macro inbox flow.

For instance, there’s the recurrent, occasional tendency towards an overbearish interpretation of our messaging.

When that inbox sentiment crescendo’s I have to offer the gentle reminder that we are in post balance sheet recession expansion and expansions following Financial Crises are almost always longer in period and lower in amplitude than normal business cycle expansions (i.e. slow & lower for longer) - that is one of their defining characteristics.

Growth slowing is part of the cycle. It takes time to play out. Just because we harp on that reality regularly doesn’t mean we expect a recession to start this afternoon. That’s not how #TheCycle works.

We are in month 87 of the current expansion. That compares to a mean and median duration of 50 and 59 months, respectively, over the last century of cycles. And with the Fed projecting continued policy normalization through 2018, they are implicitly forecasting the longest expansion ever.

As rate cuts, QE, QQE, Forward Guidance and NIRP exhaust their utility and the collective global central banking chorus shifts the policy siren song towards fiscal expansion, the cyclical expansion show is coming to a close.

The expansionary after-party is beginning. After-party’s aren’t known for being low-volatility, at least not the good ones.

As Keith highlighted yesterday, the deep simplicity is that for #GrowthSlowing allocations to really stop working you need growth to accelerate.

Since it’s jobs day, let’s take a labor-centric perspective on that.

First, a quick review of what we already know. The goal here is not to spin a narrative, it’s to just quantitatively frame the set up and the implied growth implications. Remember, I’m a bored growthslowing bear and closet optimist. This is simply the context embedded in the math:

- Employment = Consumptions Middle-Man | the health and dynamism of the labor market is the primary proxy for the health of the broader Macroeconomy. In a more narrow sense – and the one that matters to GDP accounting and policy makers - Employment is the means to a Consumption and Investment End.

- Employment Growth = ↓ | Employment growth peaked in February of last year and has been progressively decelerating. Historically, once we roll off of peak rate-of-change, it’s a one way street towards convergence with zero and economic contraction. We need to add >282K jobs in July to avoid another sequential deceleration in NFP growth. That is unlikely.

- Income = ↓ | Income growth defines the capacity for sustainable consumption growth for most households. With payroll growth slowing and weekly hours largely flat, the modest increase in wage growth has not been enough to offset the deceleration in employment and aggregate income growth has slowed. Remember, wage growth needs to move at a pace equal and opposite to employment slows to maintain the same capacity for consumption.

- Income + Credit = ? | While Income growth has slowed, revolving credit growth continued to accelerate until March, helping to support consumption growth in the facing of slowing aggregate income growth. Revolving credit has slowed in each of the last two months but will need pick up to maintain the current pace of spending growth, particularly if the emergent acceleration in wage inflation fails to extend.

Let’s consider another dynamic. Policy is labor market dependent both directly and indirectly as an explicit aim of policy is to foster maximum employment and labor market tightening drives the evolution of growth and inflation conditions to which policy must respond.

What is maximum employment?

The employed share of the prime working age population (25-54 year olds) is currently 77.8%.

The average over the last 30 years is 78.7% with cycle peaks of 80.2%, 80.3% and 81.9% over the last 3 cycles.

So, unless the argument is that a structural shift has occurred, we seemingly still have some hay to bail to get to maximum employment. But the unemployment rate is already at the generally accepted NAIRU rate of 4.9%.

If we use the average peak employment-to-population ratio over the last three cycles (~81%) as our maximum employment bogey, that implies an additional 4.04MM jobs from current levels.

- Assuming a static labor force, that 4MM incremental jobs implies an Unemployment Rate of 2.4%. That doesn’t seem plausible.

- Under a more reasonable assumption that half the jobs gains come from the currently unemployed and half come from re-entry of workers into the labor force, the implied Unemployment Rate = 3.6% with an uptick in the Labor Force Participation Rate to 63.5% (from the current 62.7%)

Maybe that’s more realistic but any residual labor slack would transition to full tautness and ….

- The NFIB’s Jobs Hard to Fill Index remains at cycle highs

- Job openings per available worker (Unemployed + Not in Labor Force but want a job) are already at an all-time low

- Small Business Compensation plans are at cycle highs

Can we gain anywhere near that amount of jobs without wage inflation accelerating? Probably not.

But doesn’t that development become self-defeating if accelerating wage inflation drives tighter policy and a probable kibosh on what’s left of the labor cycle - taking the fledgling recover in the employment-to-population ratio with it.

The employment participation party would end before it really started and as the employed share of the prime working age population peaked and rolled over before even getting to trough levels observed over the prior three cycles.

Also, remember that domestic employment growth is coming in the face of decelerating global growth, an ongoing recession in capex spending and tightening corporate and consumer credit conditions (per the 3Q Senior Loan Officer survey).

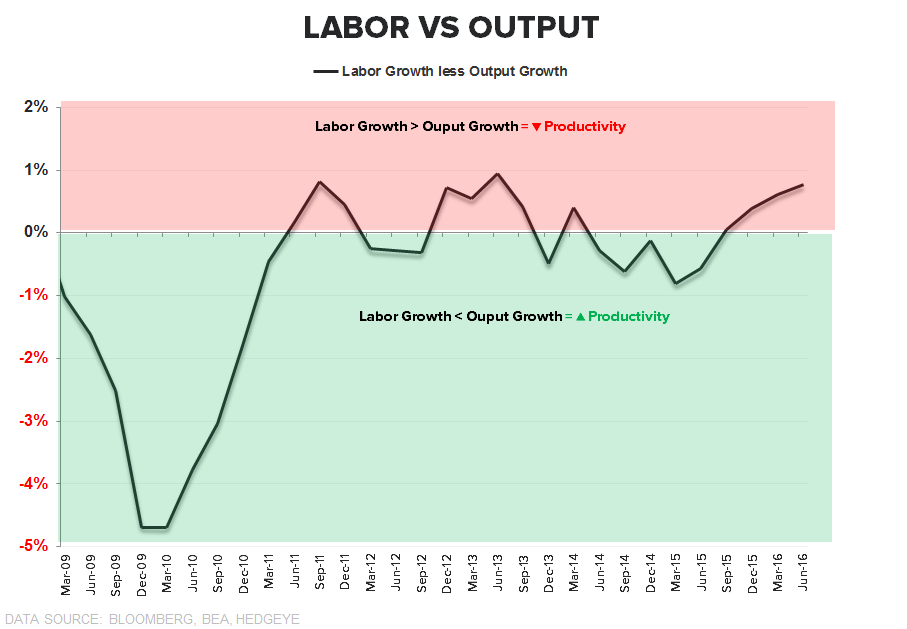

Global demand and domestic output growth are down. And employment growth in excess of output growth – which remains the case currently- is paid for via lower corporate profitability.

Absent improved productivity, “strong” employment trends = further margin compression = continued profitability pressure against a backdrop of forward earnings growth estimates in the mid-teens. We continue to think those expectations need to be marked lower.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.40-1.60%

SPX 2145-2177

VIX 11.75-15.16

EUR/USD 1.09-1.12

Oil (WTI) 39.08-43.62

Gold 1

Hit the dance floor, take a shot for every rhetorical pivot from the Fed, enjoy the after-party. It might not be easy to navigate but it definitely won’t be boring.

Christian B. Drake

U.S. Macro Analyst