Editor's Note: Our Industrials analyst Jay Van Sciver hosted an in-depth presentation on his Caterpillar short call today. He recently added CAT back to his Best Ideas list. Below are key discussion points he covered during the call.

KEY DISCUSSION POINTS:

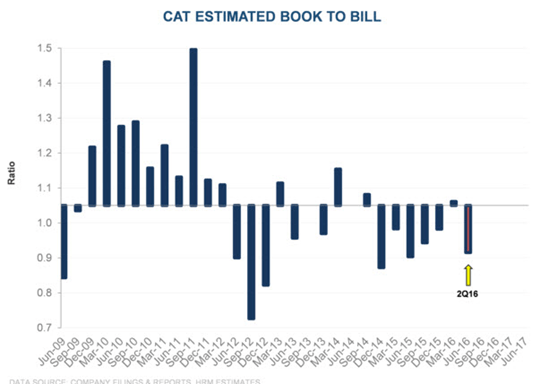

- Orders vs. Sales: Do order rates support current 2H16 & 2017 consensus estimates?

- Mutually Exclusive Goals: Can CAT maintain its dividend and its credit rating?

- Materials Cost: What do higher steel prices mean for future manufacturing decrementals?

- CAT Financial: Is the decline in allowances appropriate and sustainable?

- Aftermarket Cycle Stability: Do improvements in mining equipment aftermarket move the needle for CAT?

- Valuation: Are CAT shares pricing in a cyclical rebound in Mining and Oil & Gas capital spending?