Below are our analysts’ new updates on our eleven current high conviction long and short ideas. As a reminder, if nothing material has changed in the past week which would affect a particular idea, our analyst has noted this.

Please note that we added PowerShares DB US Dollar Index Bullish Fund (UUP) to the long side of Investing Ideas and removed Junk Bonds (JNK), Dunkin' Brands (DNKN), Allscripts Healthcare Solutions (MDRX) and Treasury Inflation-Protected Securities (TIP). We will send Hedgeye CEO Keith McCullough's refreshed levels for our high-conviction Investing Ideas in a seperate email.

IDEAS UPDATES

TLT | GLD | UUP

To view our analyst's original report on TIPs click here and here for Gold.

We made some changes in this week's edition of Investing Ideas, with the removal of Junk Bonds (JNK) on the short side and Treasury Inflation-Protected Securities (TIP) on the long-side.

With the epic move in ten-year yields to all-time lows, corporate credit spreads (JNK) have floated off the “risk-free” rate. The pull-back in cross-asset volatility from the February highs in the VIX, OVX (oil volatility index), and the MOVE Index (Treasury volatility index), likely exacerbated the tightening in spreads.

The credit cycle WILL cycle, and deterioration in consumer and corporate credit remains an important Hedgeye Macro theme. This week the Q2 Fed Senior Loan Officer Survey was released which confirmed deterioration in credit conditions (see the chart below for our credit cycle indicator; the chart is busy but it’s worth a hard look).

Our team’s macro process is both fundamental and top-down, and we get the top-down signals in real-time. The bottom-line is that both the CRB Commodities Index and crude oil have recently broken down from a quantitative risk management perspective. While this is a key factor contributing to our recent addition of the PowerShares DB US Dollar Index Bullish Fund (UUP), it also signals that TIP does not have as much upside as we thought. As Keith McCullough wrote to subscribers this week:

“Changing my mind on longer-term longs has happened infrequently this year, but it should happen. That’s how the game goes.”

Getting out of a position if it’s not working is much more prudent than stubbornly sticking with it when your process signals otherwise.

Back to growth ... we’ll refrain from commenting on Friday’s headline non-farm payrolls number in isolation, and rather offer some perspective on the cyclical nature of the non-farm payroll data series (you’ve heard it before):

- On a Y/Y rate of change basis, Non-Farm Payrolls peaked in February of 2015;

- Once growth in this series peaks and rolls over, it doesn’t return and we move toward economic contraction on the margin. Read: Bullish for Long Bonds (TLT);

- A print of +282K jobs was needed for July to avoid another Y/Y sequential deceleration in the series. NFP additions were +255K. While this beat expectations of +180K (which was cheered by just about every mainstream media outlet), the TREND in this series remains slow-moving, predictable, and most importantly past peak

HBI

To view our analyst's original report on Hanesbrands click here.

Hanesbrands (HBI) reported 2Q earnings this week. Salesmanship was on another level this quarter, as Richard Knoll took his 10-year victory lap before officially handing the reins over to Gerald Evans. But, salesmanship on the conference call can't mask lack of sales dollars on the P&L, as HBI missed sales expectations for the 8th time in 10 quarters, and posted the 3rd worst organic growth rate since the company became a serial acquirer. Margins showed the first crack we’ve seen in over 2 years – down 75bps Y/Y as competition and the effects of bloated inventories began to rear their heads. Despite all the talk about inventory reduction actions, core inventory grew 11% on -3% sales growth – even more troubling when we consider tepid demand from the company’s wholesale partners.

Even with some recent weakness in the stock, we like the short even more after this print. All in, we think that HBI has another 40% downside until the risk/reward looks more balanced in our model, with the possibility of an even bigger move in the worst case scenario.

ZBH

To view our analyst's original report on Zimmer Biomet click here.

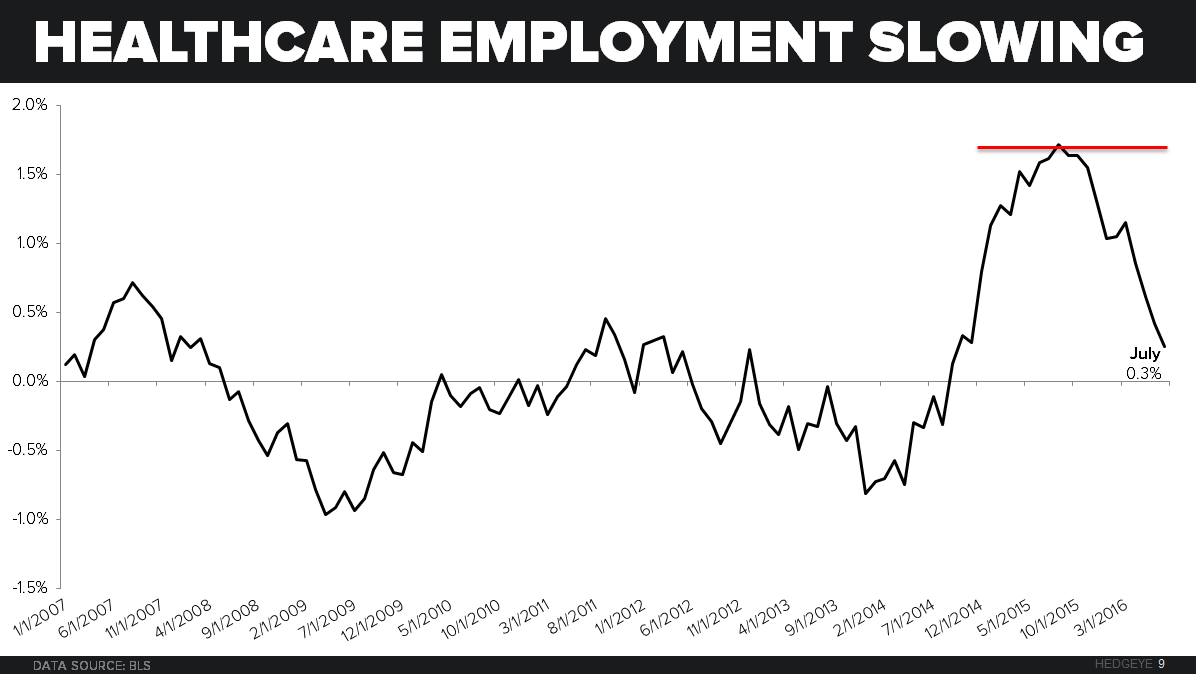

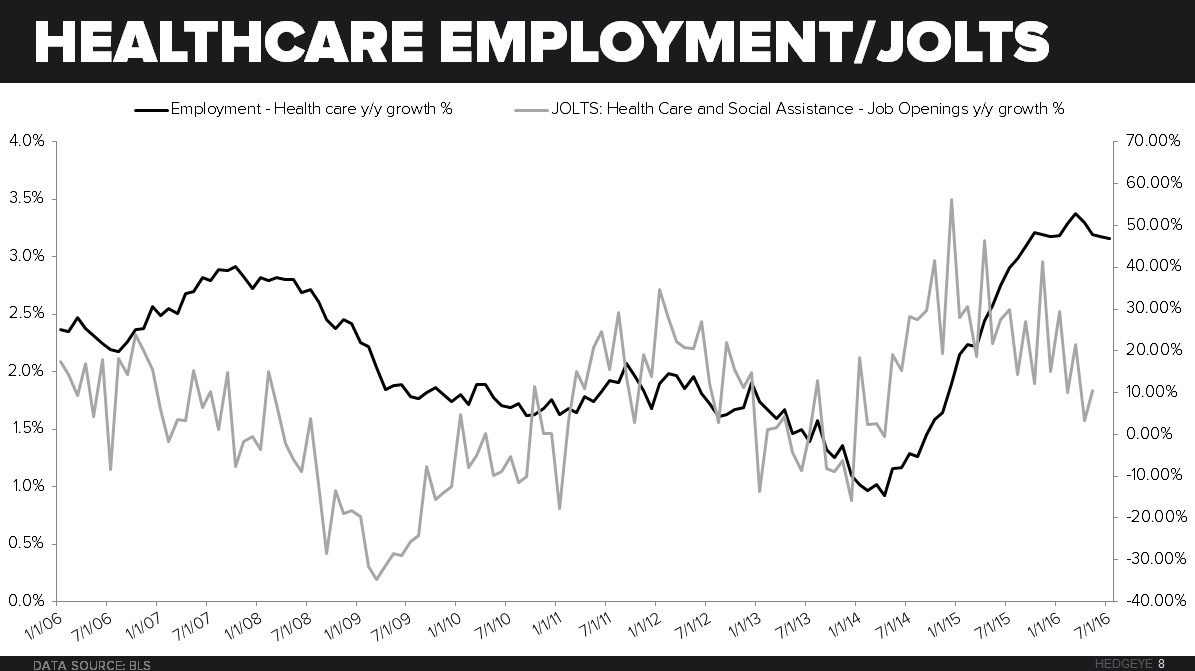

As we detailed in our Healthcare Themes deck this past month, the US medical economy is on the edge of a massive deceleration. July Helathcare employment, which is a lagging factor, slowed again. Next week, we will get the leading/coincident indicator of demand in the Job Openings and Labor Turnover series on August 10th.

Since growth in insured medical consumers has slowed to 1.5% currently, and managed care payors are withdrawing from Obamacare Public Exchange business, we expect growth in this series to deteriorate further. Hospital admissions continue to slow through 2Q16, with operators cutting guidance.

While Orthopedic and surgical demand appears positive, we still expect declines to emerge and pricing to accelerate to the downside. The CJR has already hit post-acute care, reducing admissions by 40% anecdotally across joint replacements. The next step, again anecdotally, will be to pressure device costs.

HOLX

To view our analyst's original report on Hologic click here.

In the latest data from MQSA, which has recently begun reporting placements of Digital Breast Tomosynthesis systems, it would appear that growth is slowing and Hologic's (HOLX) share of the incremental facility is dropping. According to the data, the market added 109 facilities in July after adding 107 in June, this conversion pace is similar to the 2D adoption curve post peak.

As it relates to our data, which shows 33 and 22 facilities converting to Hologic, the implication is that Hologic is losing out. In fact when we spoke to a former sales representative who sold mammography for Hologic, the benefits of one manufacturer over the other were scant at best. Going forward, we expect a slowing US Medical economy, as forecast using the slowing number of insured medical consumers, will provide the second leg of disappointing growth for our thesis.

Next Wednesday on August 10th BLS will update the JOLTS data for healthcare, a time series tightly correlated with market growth. We expect a declining number sequentially and slowing overall which will impact Hologic’s Diagnostic segment, the standout this past quarter.

LAZ

To view our analyst's original report on Lazard click here.

No update on Lazard (LAZ) this week but Hedgeye Financials analyst Jonathan Casteleyn reiterates his short call on the company.

TIF

To view our analyst's original report on Tiffany click here.

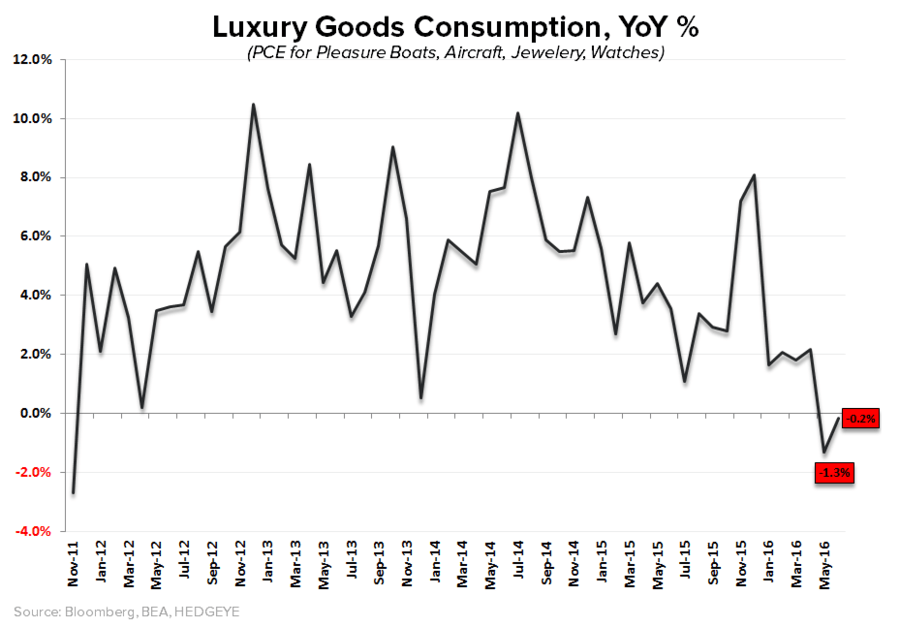

The government released June PCE data this week. As it relates to Tiffany (TIF), we again are looking at the spend in the luxury sector. Real luxury spending went negative in May for the first time since 2011 and the June number, which showed a slight inflection (lower highs and lower lows), was in negative territory once again. That marks the first time we’ve seen negative spending data at the high-end.

The comp sales trajectory has been one of the worst we’ve seen in retail at Tiffany, and some may argue that the company is facing easy compares. But we think that’s a simplistic analysis, given the weakness we are starting to see in the category. We think the negative macro pressure here will compound the already big demand issues TIF is facing. That means… more sales and earnings surprises to the downside.

FL

To view our analyst's original report on Foot Locker click here.

Diving in on what the Nike Wholesale and DTC dynamics mean for Foot Locker (FL), we outlined last week that given the likely Nike US wholesale growth scenario, FL needs an incremental $200mm from the likes of UA and AdiBok to hit current Consensus Estimates. This means that UA would need to grow FW 60% and AdiBok 20% with 50% of that growth coming from wholesale with the over arching assumption that FL captures 40% of the incremental share from each of the brands.

The only problem with those type of growth and channel assumptions is that Nike isn’t the only brand navigating around its wholesale partners. AdiBok is the worst offender with 70% of its incremental growth over the past 4 years coming from the direct channel. UA is at 32%, and we think FW growth for UA is more heavily weighted to the DTC channel. That means from here, the likes of AdiBok and Under Armour would need to take share from NKE, allocate over 40% of its wholesale growth to FL, and (not or) redirect a portion of its more profitable retail growth to the wholesale channel. A lot has to go right for that to happen.

WAB

To view our analyst's original report on Wabtec click here.

No update on Wabtec (WAB) but Hedgeye Industrials analyst Jay Van Sciver reiterates his short call. Hedgeye CEO Keith McCullough had this to say about the company in a Real-Time Alerts signal sent earlier this week:

"Again, our Best Ideas research list of SELL ideas is a lot longer than my live SELL list in Real-Time Alerts. Main reason for that = patience. I realize consensus is chasing US Equity Beta, so I'm happy to wait and watch for selling opportunities.

Wabtec (WAB) has been an excellent SELL idea by Jay Van Sciver. We like it when we don't like a stock and it goes down when the market is going up. Jay's most recent comment on WAB was:

"We will let others summarize the WAB quarter, but would note that our WAB thesis continues to play out reasonably well. We would caution longs that this is only the third quarter of down freight revenue, and both railcar and locomotive deliveries in the quarter remained well above likely ‘normalized’ demand."

To Patient Bears,

KM"

LMT

To view our analyst's original report on Lockheed Martin click here.

On Tuesday, the Air Force declared that Lockheed Martin's (LMT) F-35A has officially achieved “Initial Operational Capability” (IOC). Specifically, this means that the Air Force now has "an operational squadron of 12-24 aircraft with Airmen who are trained, manned, and equipped to conduct basic Close Air Support (CAS), Interdiction, and limited Suppression and Destruction of Enemy Air Defense (SEAD/DEAD) operations in a contested environment.”

It is hard to overstate the importance of this milestone for the largest Defense acquisition program in history. There is now a clear sense of momentum for the program and the operational milestones are coming in bunches. The commander of Air Combat Command declared that he would be getting the F-35A into operations either against ISIS or to Europe in the “near future.” The Marines now have two operational squadrons and with the first deploying next year to Iwakuni, Japan for potential operations in Korea. This week also saw the Navy beginning its third and final phase of developmental testing at sea on the George Washington.

With operational flight data now available, speculative criticism of operational capability has almost completely withered away. Concern for costs is still present but it is based on the volume of jets needed/desired (2,443 for US) rather than the unit cost of $80-85M for the A (B&C models cost 10-15% more).