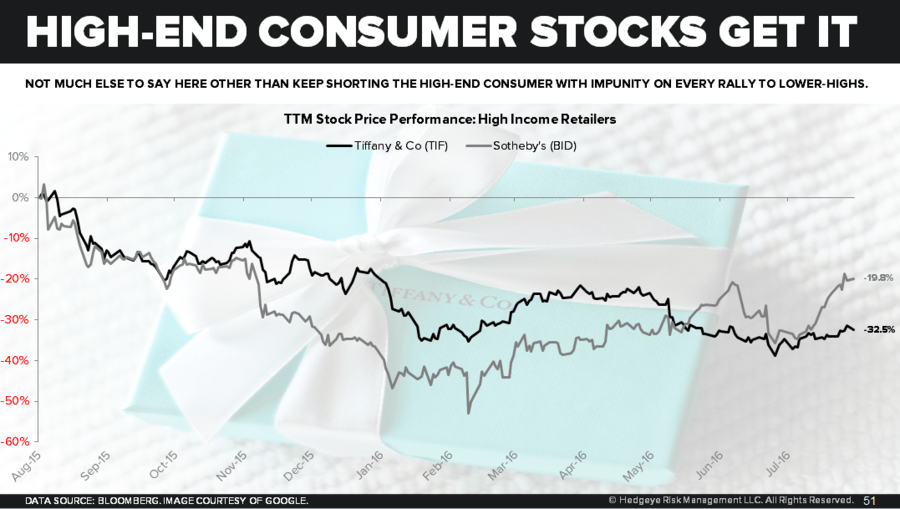

Rich In Retreat: Estimates on the impact of the wealthy on consumer spending vary but all put the share of consumer outlays by the top quintile at greater than 40%. In short, and regardless of estimate precision, it's significant.

We use spending on Luxury Goods - a composite of series from the underlying PCE data - as a proxy for the state of high end consumerism. The updated June detail data released this morning suggest the rich remain in retreat or, at the least, reluctant to accelerate high-ticket discretionary purchasing.

Luxury Goods consumption fell -0.2% YoY in June following the -1.3% YoY decline recorded in May with the duo of negative prints marking the first months of negative growth since 2011. With spending up just +1.0% YTD, 2016 represents the slowest pace of expenditure growth for the composite since 2010.

Volatility Sensitivity: High-end Consumption (unsurprisingly) carries a higher sensitivity to asset market volatility than does total consumption. To the extent wealth effect benefits have crested alongside the multi-year middling in global equities performance and/or recurrent bouts of elevated volatility continue to characterize late-cycle conditions and the diminished effectiveness of monetary policy, high end consumption growth is likely to remain constrained.

VIX Model for Dummies (like us): The simple, prevailing reality since cross asset class volatility troughed in 2014 is that VIX <13 is always (and closely) followed by VIX >13 and equity performance hiccups. A gradual reduction in exposure as VIX moved towards sub-13 has, almost universally, provided the opportunity to buy back that exposure lower. At the least, it’s proved prudent to not be ramping exposure at VIX 10/11/12.

NIRP, China, Brexit and the breakdown of the central bank #BeliefSystem in Japan are separate events but are all outcroppings of the same slow growth reality and similar types of events will continue to manifest. Increasing net/gross exposure at VIX 11 implicitly embeds an assumption that those events either won’t happen, won’t matter in terms of impact on prices, or won’t matter until there has been some latent build-up of stress to some critical threshold that the market decides that it cares.

We don’t advocate myopic, 1-factor model decision-making but calibrating exposure in counter-VIX fashion has proven to be about as tractable a low-intensity, common sense risk management strategy as there’s been the last couple years.

Christian B. Drake

@HedgeyeUSA