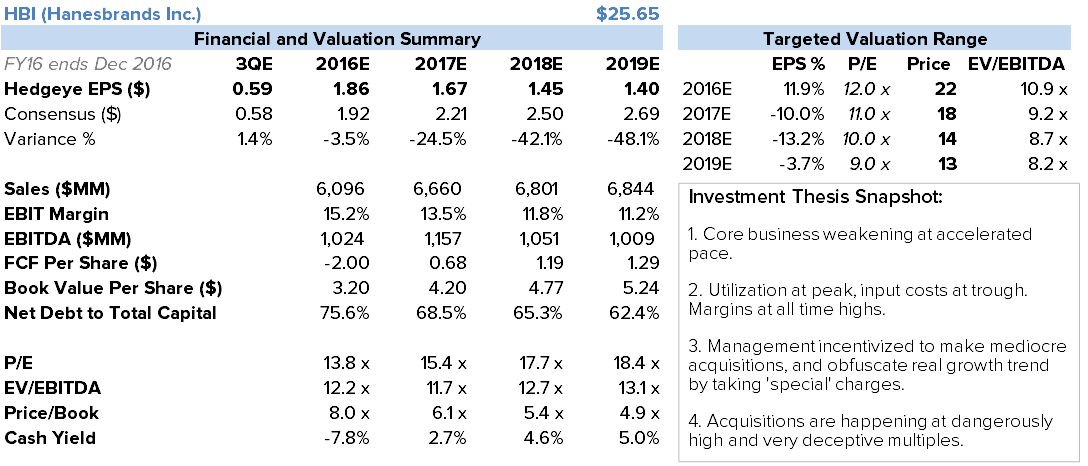

Conclusion: HBI remains our top short, and despite the after hours weakness in the stock and 17% decline since announcing the Pacific Brands acquisition, we’d press the position here. To be clear, this is a company that has no (and perhaps negative) organic growth opportunity, as it is facing increased competition from both the high and low end and at the same time it is staring down the barrel of an over-inventoried US wholesale channel. As such HBI turned into a serial acquirer and is buying companies in jurisdictions where it has neither scale, brand, expertise, nor competitive advantage. Importantly, HBI is sitting at peak margins due in large part to unsustainable capacity utilization levels, which we think will give way and expose the operating leverage inherent to this model that most retail investors don’t acknowledge. And to boot, HBI has the most egregious spread between GAAP and ‘adjusted’ earnings than any company in its class – and is backed by a board and a compensation structure that encourages management to act in a way that we think is inconsistent with long-term shareholder interests. All in, we think that HBI has another 40% downside until the risk/reward looks more balanced in our model, with the possibility of yet a bigger move in the worst case scenario.

FULL DETAILS

HBI’s salesmanship was on another level this quarter as Richard Knoll took his 10yr victory lap before officially handing the reins over to Gerald Evans. But, salesmanship on the conference call can't mask lack of sales dollars on the P&L, as HBI missed sales expectations for the 8th time in 10 quarters, and posted the 3rd worst organic growth rate since the company became a serial acquirer. Margins showed the first crack we’ve seen in over 2 years -- down 75bps YY as competition and the effects of bloated inventories began to rear their heads. Despite all the talk about inventory reduction actions, core inventory grew 11% on -3% sales growth – even more troubling when we consider the tepid demand from the company’s wholesale partners. The flexibility to financially engineer earnings growth is all but done now that the two new acquisitions have closed and HBI has added $1.2bn in long term debt. And oh by the way the two combined will add 14% of growth to the top line but only $0.07 (+4%) in annualized adjusted earnings accretion to the bottom line.

Organic & Acquired Growth:

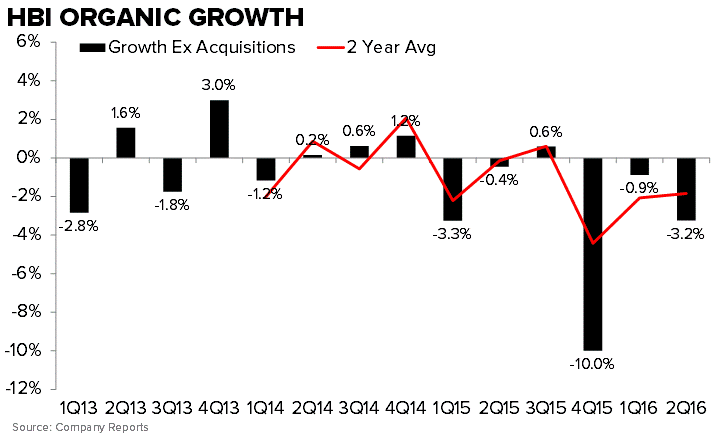

We got a look behind the kimono this quarter as HBI was in a unique position where it had zero benefit from acquisitions for the first time in 3 years. And the trend was less than inspiring. Champion Europe and Pacific Brands will be consolidated into the P&L next year, and will give the illusion of growth, but we think the trend in the underlying business is perfectly clear, without acquisitions 2Q growth was -3%, and has now been negative for 5 of the last 6 quarters.

HBI's core Innerwear business slowed to -2.5% from 1.3% in 1Q. As we outlined in our note last week HBI | Gildan A Thorn In Its Side (LINK: CLICK HERE) we think an outlier threat to organic growth for HBI has been the pressure applied at the low end by Gildan within Innerwear. Gildan has climbed to 9% share in units within the US men's underwear space in just 3 years after its launch of Gildan branded. And not only is Gildan taking share, but share gains accelerated in 1H16 which means we don’t see this headwind waning for a long time. Competition is rising on the high end as well with dozens of new brands playing in the higher priced performance underwear space along with the lineup of heavy hitters of Nike, UnderArmour, and Lululemon continuing to invest in their underwear businesses.

The two new acquisitions that closed over the last month will add about $800mm to the top line over the next year. Management sees about $350mm in flowing through in 2016, our math suggests the number may end up closer to $400mm.

We have broken out our estimate of the benefit by quarter and the corresponding growth contribution below. 3Q should see about 12% growth from the new businesses, which HBI will need as it will be facing one of its toughest "core" organic growth compares of the last 3 years at 3% as reported by the company last year.

High Inventory:

HBI spent an incremental $12mm in inventory reduction initiatives, but hey the inventory clean-up plan is tracking to plan…right? Nah, not even close as the sales to inventory spread only went from -16% to -14% after adjusting for the $51mm increase created by the closing of Champion Europe around quarter end. When asked about how Pacific inventory might end up impacting 3Q inventory, management chose not to give an estimate. This would leave room for underlying inventory to remain in the fog of acquisition for at least another quarter.

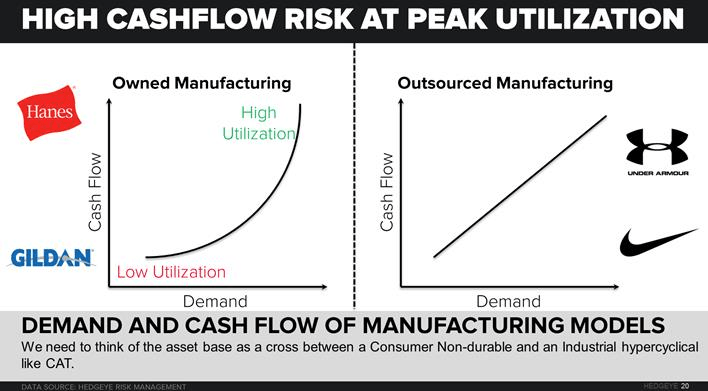

The elevated inventory is bearish for margins on two levels: First being the need to spend or cut price to bring levels back to normal, and the second being the utilization impact of slowing production. To review, HBI currently sits at peak utilization while at the same time we are seeing organic growth slowing, and the sales to inventory spread around the worst levels in nearly 5 years.

Referring back to our Black Book, the cashflow & margin risk is significantly higher at peak utilization for a company that owns a majority of production like HBI. Negative moves in demand can have exponential flow through implications for profitability.

Pacific Brands is a Potential Disaster:

One common pushback for our HBI short is that there are still plenty of brands out there to buy and plenty of charges to be taken. However HBI may have already overstepped its bounds in this area. Not only have the multiples gotten desperately high, but we think the macro risk associated with Pacific Brands is immense.

Hedgeye Financials and Retail teams have done some deep dive work on the Australian economy. Simply put, our work suggests that Australia is currently at the tail end of a housing/property bubble that is worse than what the US saw in 2007/2008. Given the role home equity withdrawal has played in discretionary spending, the consumption impact is likely to be much greater than what was experienced in the US.

Pacific has about 15% share in the Australasia underwear market (#1), and it will undoubtedly be significantly impacted by the impending financial crisis/recession in Australia. HBI is already paying 12.5x EBITDA for the Pacific assets, which now make up about 10% of sales post acquisition. When all is said and done the real multiple paid could end up being 20x plus. We think this has the potential to be the straw that breaks the camel's back as it relates to HBI stock should the economic situation down under play out as we expect.