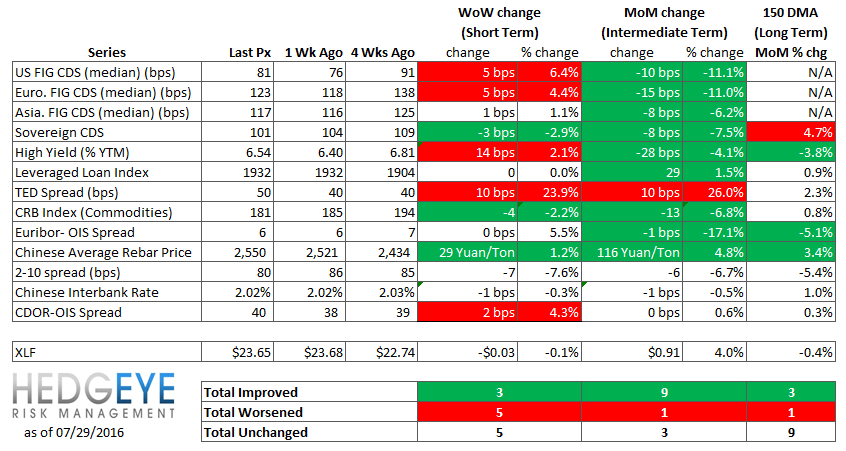

Key Takeaway:

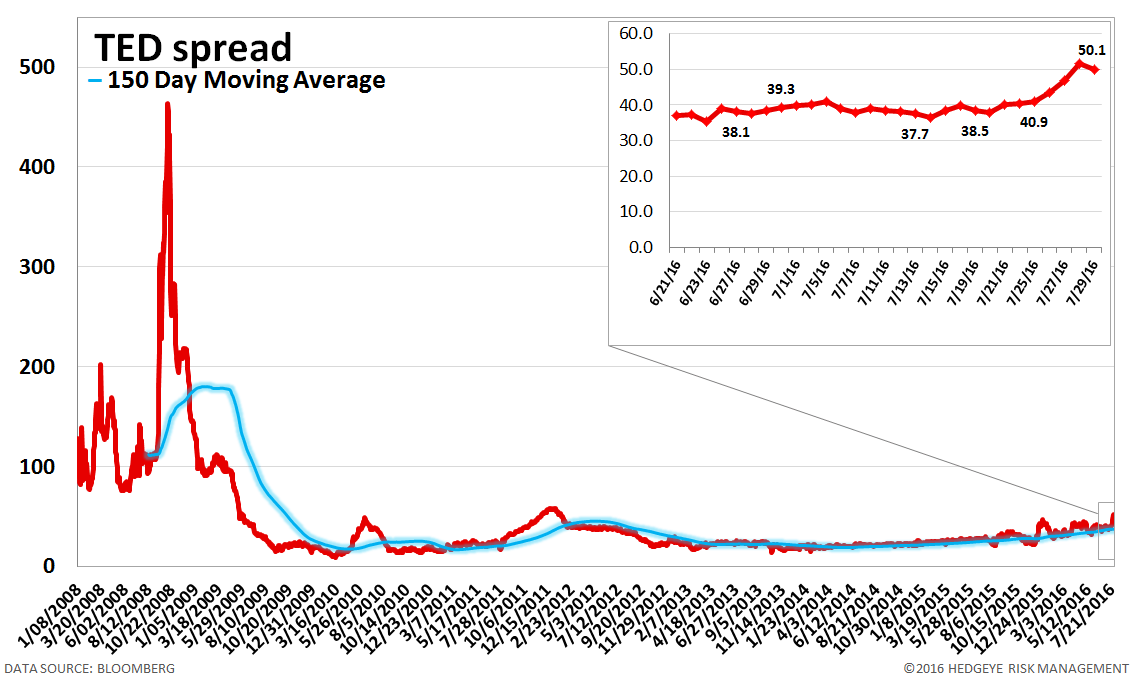

Friday's disappointing U.S. GDP reading broke the streak of optimistic risk readings; U.S. financials CDS widened by 5 bps to 81, the high yield YTM rose by 14 bps to 6.54%, and the usually stable TED spread (a measure of bank counterparty) spiked by 10 bps to 50. Interestingly, the TED Spread just hit a 4-year high - the last time it was north of 50 bps was January, 2012. Additionally, in Europe, financials CDS widened by 5 bps to 123 as mostly positive results from banking stress tests were not enough to ease investor worry.

Current Ideas:

Financial Risk Monitor Summary

• Short-term(WoW): Negative / 3 of 13 improved / 5 out of 13 worsened / 5 of 13 unchanged

• Intermediate-term(WoW): Positive / 9 of 13 improved / 1 out of 13 worsened / 3 of 13 unchanged

• Long-term(WoW): Positive / 3 of 13 improved / 1 out of 13 worsened / 9 of 13 unchanged

1. U.S. Financial CDS – Swaps widened for 12 out of 13 domestic financial institutions. With Friday's disappointing read on GDP, which grew only 1.2% in Q2, the median U.S. financials swaps widened by 5 bps to 81.

Widened the least/ tightened the most WoW: COF, GNW, ACE

Widened the most WoW: AIG, JPM, BAC

Tightened the most WoW: HIG, BAC, C

Widened the most MoM: MTG, AON, CB

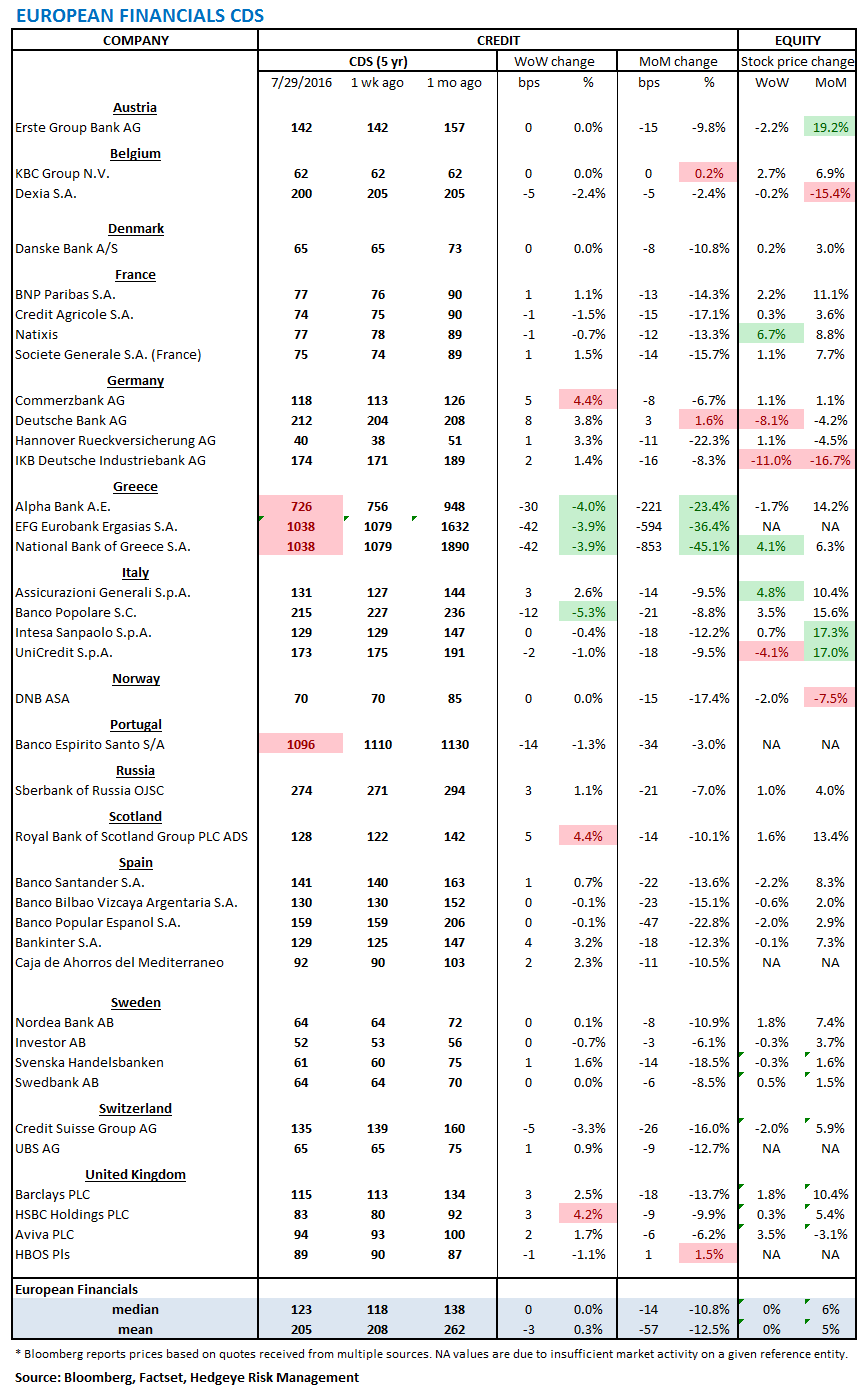

2. European Financial CDS – Financials swaps were mixed in Europe last week. While the European Banking Authority cleared most banks after evaluating their stress tests, Italian UniCredit, British Barclays and German Deutsche Bank suffered hits to their capital buffers, pushing CDS for Barclays and Deutsche wider by 3 bps to 115 and by 8 bps to 212, respectively. Interestingly, UniCredit CDS actually tightened by -2 bps to 173.

3. Asian Financial CDS – In Japan, the BOJ's modest easing announcement was not enough to significantly move the country's financials CDS, although Sumitomo Mitsui swaps did stand out, tightening by -2 bps to 84; the central bank stated it will buy ¥6 trillion of ETFs annually but leave its key interest rate unchanged. Meanwhile, Chinese and Indian bank CDS mostly widened.

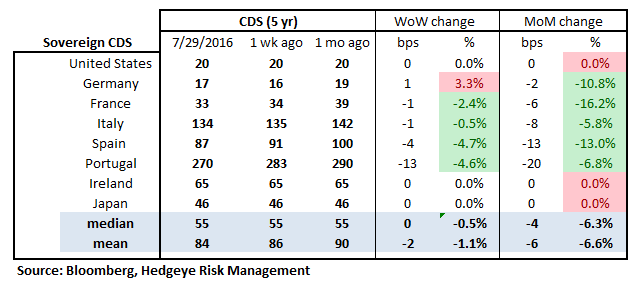

4. Sovereign CDS – Sovereign swaps mostly tightened over last week. Portuguese swaps tightened the most, by -13 bps to 270.

5. Emerging Market Sovereign CDS – Emerging market swaps mostly widened last week. Mexican sovereign swaps widened the most, by 12 bps to 152, followed by Russian swaps, which widened by 11 bps to 239.

6. High Yield (YTM) Monitor – High Yield rates rose 14 bps last week, ending the week at 6.54% versus 6.40% the prior week.

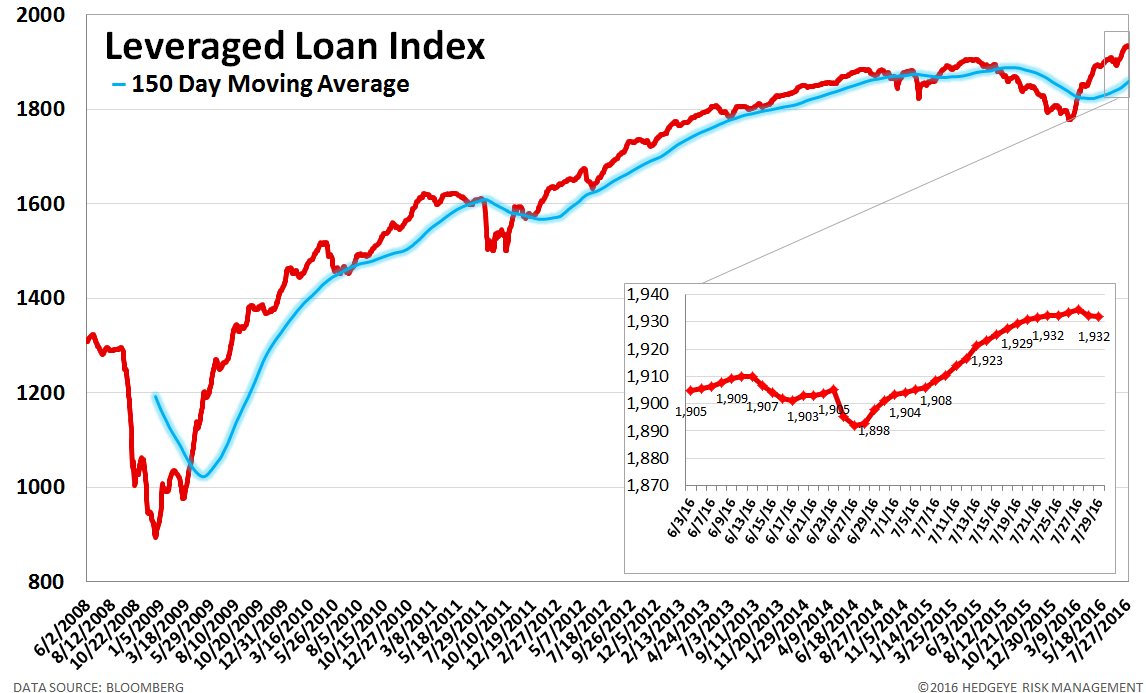

7. Leveraged Loan Index Monitor – The Leveraged Loan Index was unchanged last week, ending at 1932.

8. TED Spread Monitor – The TED spread rose 10 bps last week, ending the week at 50 bps this week versus last week’s print of 40 bps.

9. CRB Commodity Price Index – The CRB index fell -2.2%, ending the week at 181 versus 185 the prior week. As compared with the prior month, commodity prices have decreased -6.8%. We generally regard changes in commodity prices on the margin as having meaningful consumption implications.

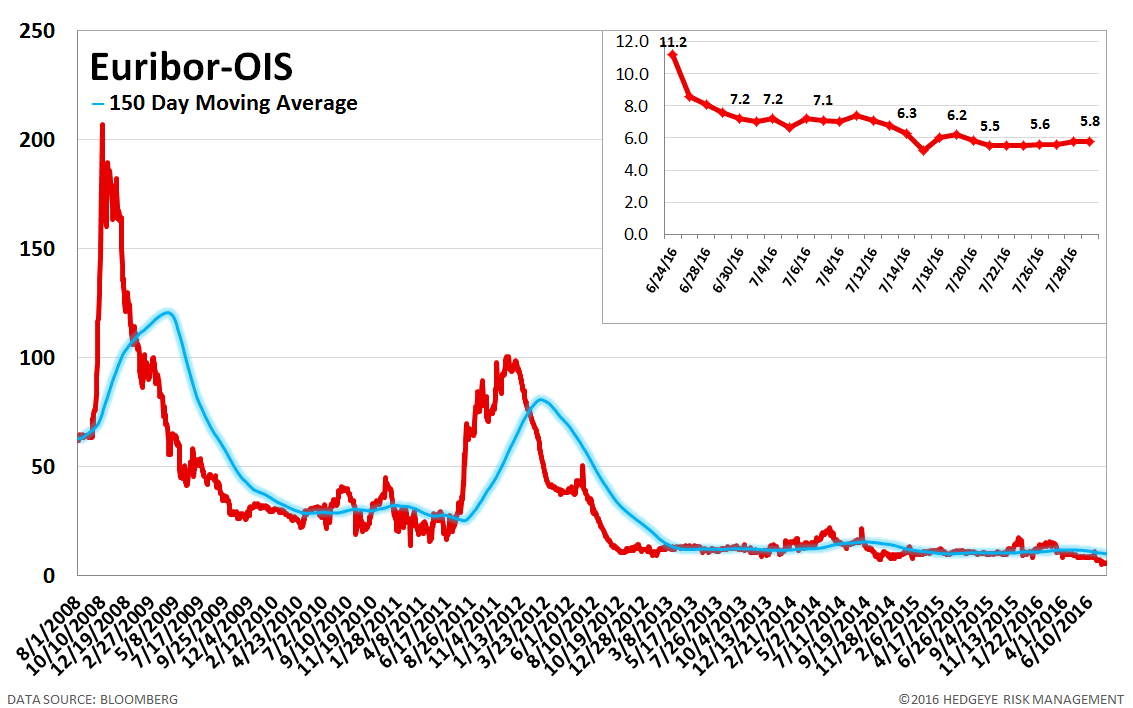

10. Euribor-OIS Spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread was unchanged at 6 bps.

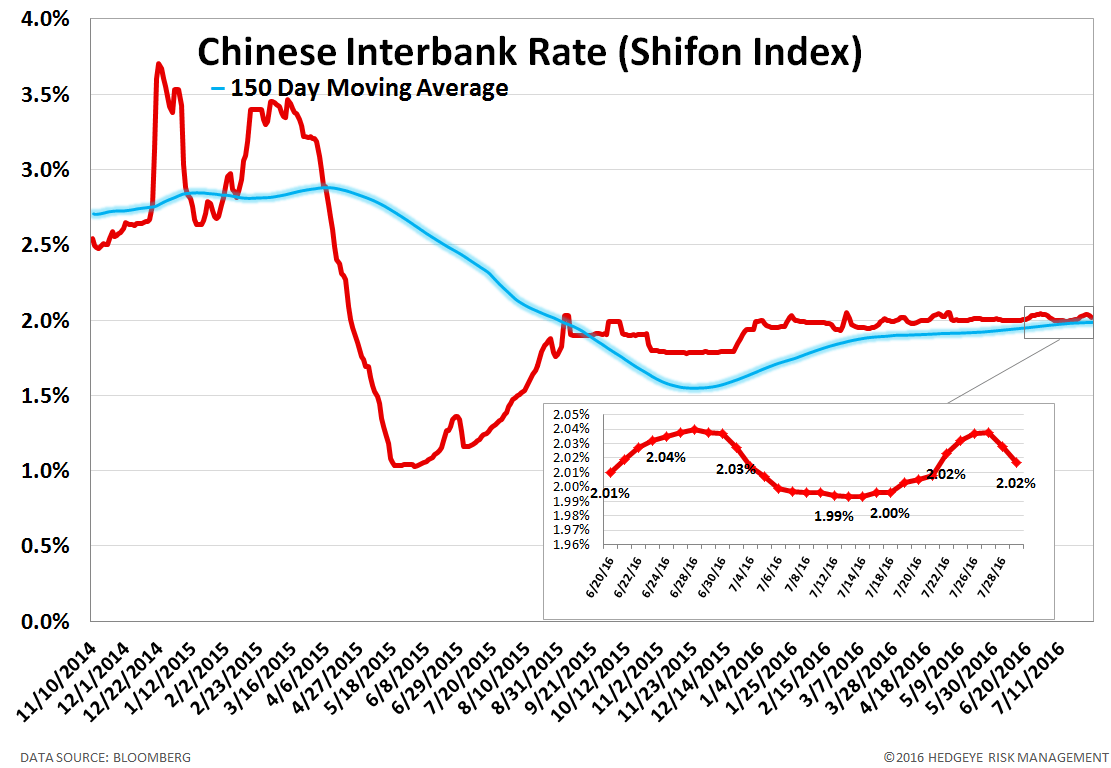

11. Chinese Interbank Rate (Shifon Index) – The Shifon Index was unchanged last week, ending at 2.02%. The Shifon Index measures banks’ overnight lending rates to one another, a gauge of systemic stress in the Chinese banking system.

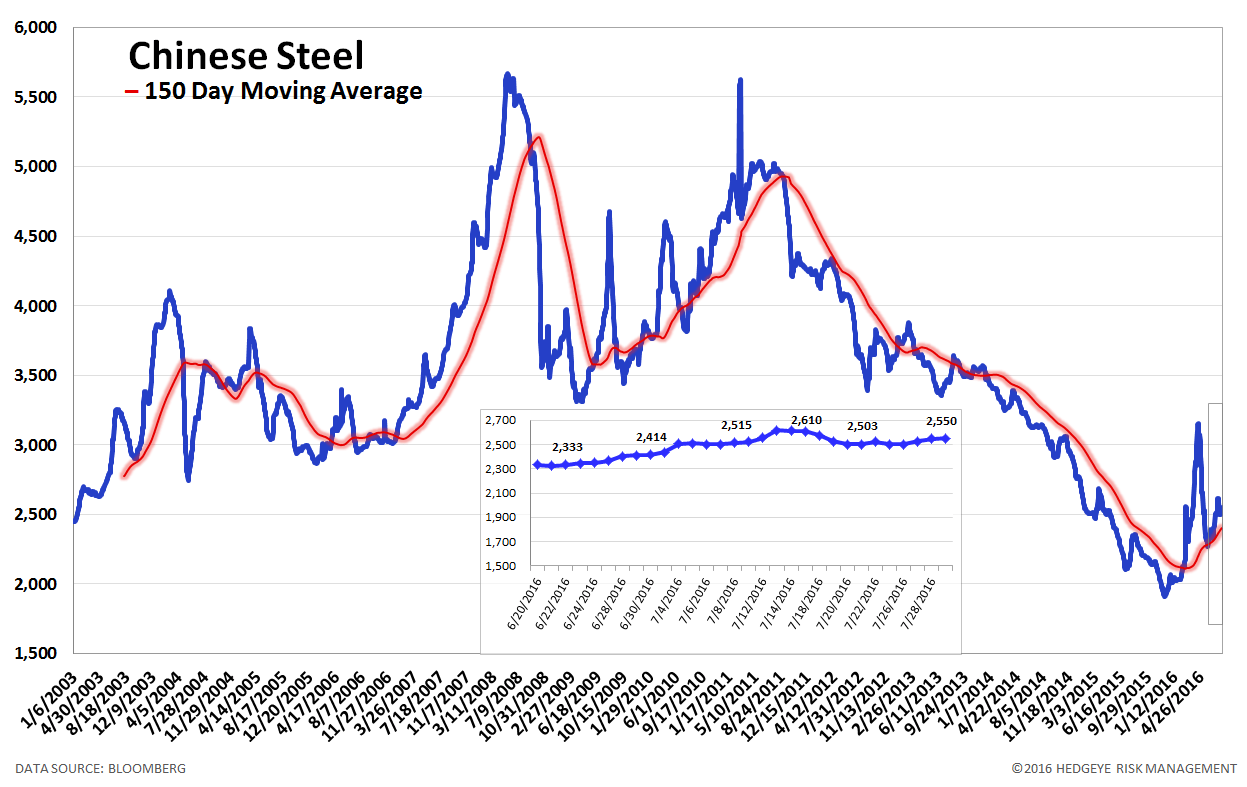

12. Chinese Steel – Steel prices in China rose 1.2% last week, or 29 yuan/ton, to 2550 yuan/ton. We use Chinese steel rebar prices to gauge Chinese construction activity and, by extension, the health of the Chinese economy.

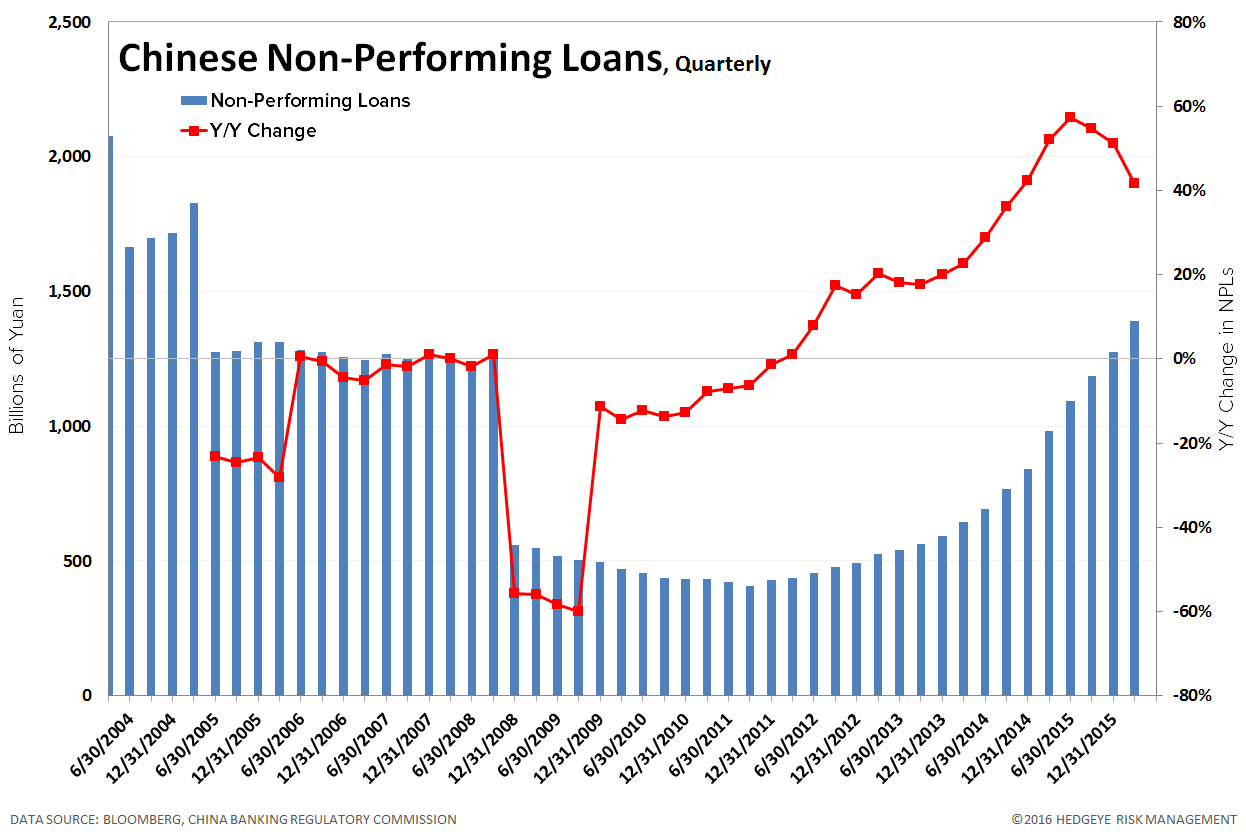

13. Chinese Non-Performing Loans – Chinese non-performing loans amount to 1,392 billion Yuan as of March 31, 2016, which is up +41.7% year over year. Given the growing focus on China's debt growth and the potential fallout, we've decided to begin tracking loan quality. Note: this data is only updated quarterly.

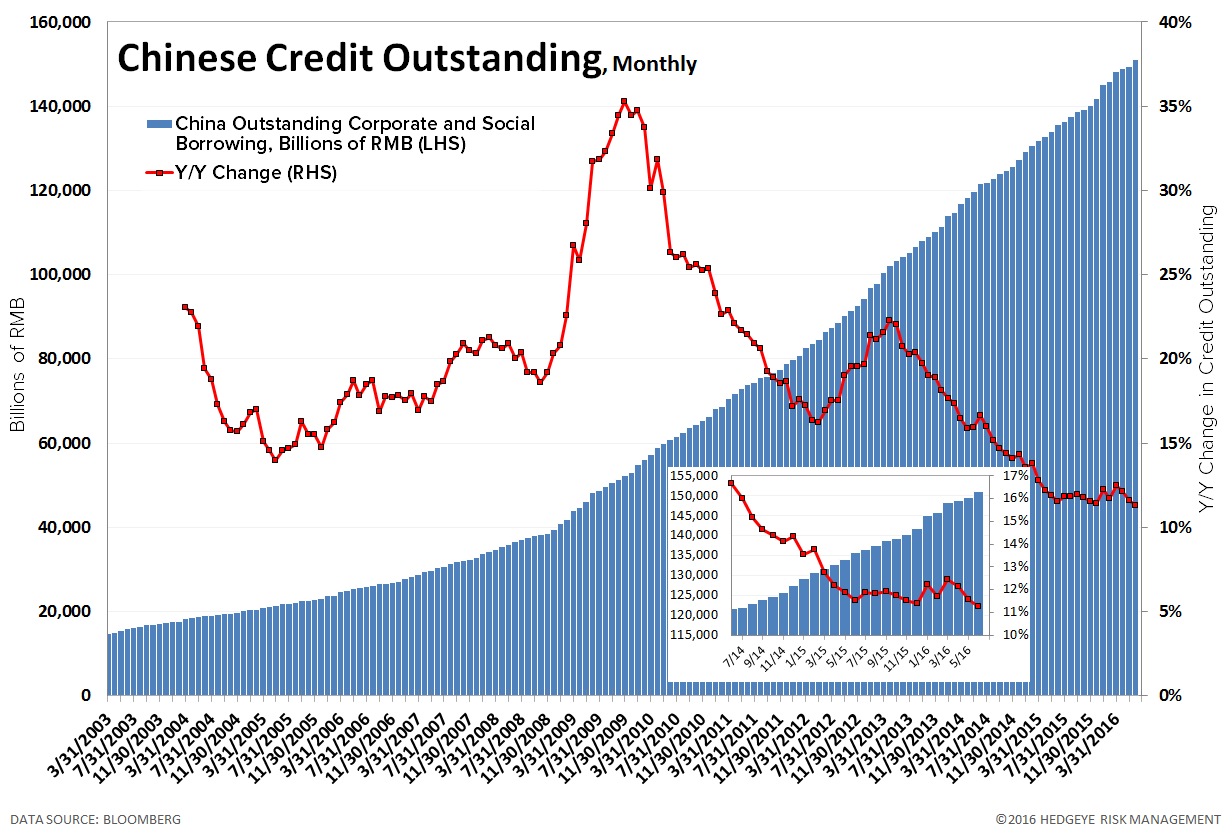

14. Chinese Credit Outstanding – Chinese credit outstanding amounts to 151.0 trillion RMB as of June 30, 2016 (data released 7/14/2016), which is up +15.3 trillion RMB or +11.3% year over year. Month-over-month, credit is up +1,514 billion RMB or +1.0%. Note: this data is only updated monthly.

15. 2-10 Spread – Last week the 2-10 spread tightened to 80 bps, -7 bps tighter than a week ago. We track the 2-10 spread as an indicator of bank margin pressure.

16. CDOR-OIS Spread – The CDOR-OIS spread is the Canadian equivalent of the Euribor-OIS spread. It is the difference between the Canadian interbank lending rate and overnight indexed swaps, and it measures bank counterparty risk in Canada. The CDOR-OIS spread widened by 2 bps to 40 bps.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT

Patrick Staudt, CFA