Below are our analysts’ new updates on our fifteen current high conviction long and short ideas. As a reminder, if nothing material has changed in the past week which would affect a particular idea, our analyst has noted this.

Please note that we added PowerShares DB US Dollar Index Bullish Fund (UUP) to the long side of Investing Ideas. We will send Hedgeye CEO Keith McCullough's refreshed levels for our high-conviction Investing Ideas in a seperate email.

IDEAS UPDATES

TIP | TLT | GLD | UUP | JNK

To view our analyst's original report on Junk Bonds click here, here for TIPs and here for Gold.

Friday’s GDP report was ugly any way you slice it. GDP grew +1.2% on a Q/Q Seasonally-Adjusted Annual Rate basis (SAAR). Of equal importance to the number is that GDP for Q1 was negatively revised to +0.8% vs. +1.1% previously. So GDP by the preferred consensus methodology is tracking +1.0% in the first half of 2016. On a Y/Y basis, our preferred methodology, GDP came in at a meager +1.2%. #GrowthSlowing?...

In last week’s report we wrote that the Q/Q SAAR number could beat consensus expectations by a wide margin, which could be taken by the market as incremental hawkish information. Well, the GDP print was a bomb. As mentioned last week:

“With growth continuing to track a decelerating trend in our model in Q3 and Q4, with 1) difficult PCE comps (consumer expenditures) and 2) easy inflation comps, we want to stick with our allocations to growth slowing.”

To summarize our active ideas, long Gold (GLD) and long U.S. Dollar position (via PowerShares DB US Dollar Index Bullish Fund (UUP), which we added this week) netted out Friday, with gold catching a bid against a USD that got crushed on the report. (Part of the reason we added UUP to Investing Ideas was the expectation of a GDP print that may have sent a hawkish message to the market.) Think of Gold and the USD as a position against a basket of other currencies.

The good news for #GrowthSlowing bulls is that the Treasury rate curve will likely get pushed lower over the coming days as investors take stock of this week’s ugly data. That's good for Treasury Inflation-Protected Securities (TIP) and Long Bonds (TLT).

It could also be good for our short Junk Bonds (JNK) call to the extent that JNK can continue to shake the decline in commodity prices over the last month (it has exposure to multiple sectors). So far high yield energy credit (materials and industrials included) has been immune to sharply lower commodity prices over the last month, partly because the Treasury curve has also moved lower.

Below is a deep dive into Friday’s GDP report:

- Consumption was strong, as expected, but slightly below expectations

- Investment tanked, driven by a big -1.2% drag from inventories and a modestly soft Resi investment number

- Government Expenditures also contributed negatively for first time since 4Q14

- GDP deflator was revised higher from last quarter which put a lid on the print. The deflator ticked up to 2.2% in 2Q (vs. 0.5% prior) with the Core PCE price index coming in at 1.7%

To recap, here's what we missed: The government telling the truth finally on the deflator and the subtraction in inventories. But we did not miss the multi-quarter TREND in growth slowing. See the table to the extent you want to dig deeper to contextualize Friday’s report:

Click images to enlarge

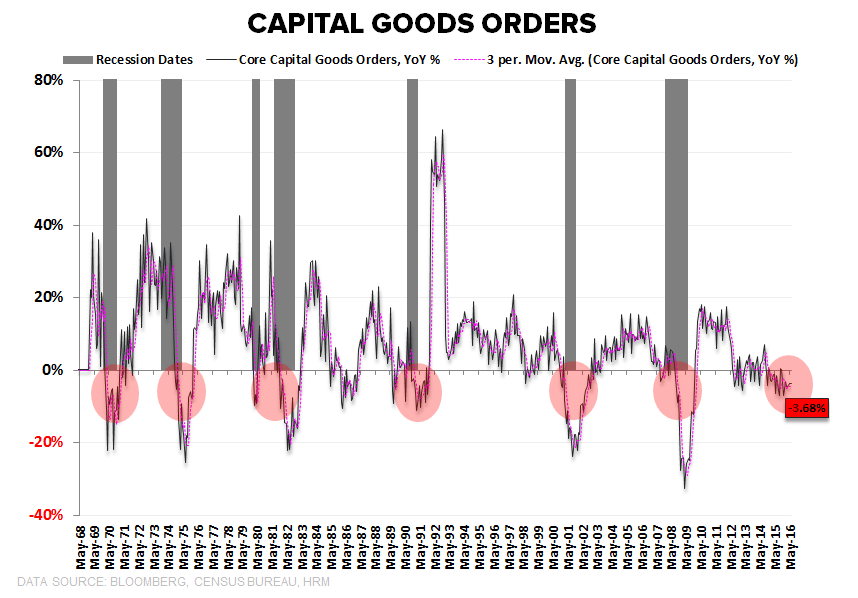

And finally to add in another summary of domestic #GrowthSlowing economic data released this past week, durable and capital goods orders released for June continued to look downright recessionary:

- Durable Goods: -4.6% sequentially in June and declined to -6.4% YoY

- Capital Goods: +0.2% M/M but the recession in core capex remains ongoing at -3.7% Y/Y, extending its epic run of negative growth to 17 of the last 18 months

DNKN

To view our analyst's original report on Dunkin Brands click here.

No update on Dunkin Brands (DNKN) but Hedgeye Restaurants analyst Howard Penney reiterates his short call.

HBI

To view our analyst's original report on Hanesbrands click here.

An outlier threat to organic growth for Hanesbrands (HBI) has been the pressure applied at the low end by Gildan. Gildan launched its own branded underwear in 2013 and has been a thorn in HBI’s side ever since. The original belief was that GIL would likely consume private label market share, but as of this week's 2Q16 earnings release, Gildan's unit share hit 9% in the Men's underwear market. That's up 60bps sequentially from 1Q, and 180bps Y/Y.

The men’s underwear market in the US is $5bn. That’s broken down into 28% market share for HBI, 24% market share for Fruit of the Loom, and 5% private label on a dollar basis. The newcomer GIL has taken 9 points of share of units (5-6% in $) in its first 3 years of existence. That’s 5-6% of share in HBI’s largest single category that:

- Represents about 17% of the business; and,

- Has come directly from the HBI’s key wholesale partners, which any way you slice it = lost market opportunity for HBI, with more pressure to come.

On the flip side, the appetite for additional inventory in basics appears to have dried up – GIL management cited negative unit volume growth in Specialty/National chains and flat to slightly positive in the mass channel.

Demand down + Competition up = continued pressure on HBI organic growth.

MDRX

To view our analyst's original report on Allscripts click here.

We attended the Becker’s Hospital Review 2nd Annual CIO/HIT + Revenue Cycle Conference in Chicago earlier this week. Over the course of two days, 175 total speakers representing 95 Hospital and Health Systems, presented on topics ranging from data analysis for population health to best practices in revenue cycle management. This was not a widely attended event by the investment community and unlike HIMSS, not vendor centric and therefore provided uncompromised insight into the challenges and opportunities facing CIOs and users of Healthcare IT.

One of the main themes of the conference was a focus on the people and process to help drive efficiencies in the revenue cycle, and the need for culture change to successfully implement a population health strategy. There was very little discussion regarding demand for new technology, with most CIOs satisfied with their current technology setup and vendor relationships.

More importantly, there was no discussion or topics related to EHR implementations and adoption, a topic that would have dominated the discussion only a few years ago. When a room full of 200 C-Suite level Hospital personnel, industry consultants and doctors were asked to raise their hand if they have been through an EHR implementation in the last three years, it was no surprise that everyone raised their hand. This confirms our view, and others, that the EHR market is saturated and the replacement market anemic.

There were two sessions dedicated solely to “Getting the Most of Your…” Epic and Cerner EHR, with the Epic session having 2x the attendees as Cerner, but little-to-mention of Allscripts (MDRX). We were surprised by how often athenahealth was brought up in the same breath as Epic, Cerner and MEDITECH, with many CIOs watching their inpatient progress closely and noting how well their #LetDoctorsBeDoctors marketing campaign resonates.

Allscripts is scheduled to report earnings next week after the close on 8/4. We continue to believe that expectations related to an Allscripts bookings beat is unfounded, and that if management had a beat up their sleeve, they would have pre-announced positive like they did in same quarter last year.

Meanwhile, Allscripts' competitor in the ambulatory market, Quality Systems (QSII) reported weak earnings this week and took down guidance for the year on weak order volume in the quarter. While not all of the weakness at QSII is attributable to market conditions, we include Allscripts ambulatory EHR and Practice Management solutions in the market share loser category along with QSII, and therefore we view this as a negative read into Allscripts ambulatory bookings.

ZBH

To view our analyst's original report on Zimmer Biomet click here. Below is an update from Hedgeye Healthcare analyst Tom Tobin.

I have been answering emails and tweets about our short call on Zimmer Biomet (ZBH). It has not been successful by any measure. While we are tempted to cover and move on, the data keeps piling up that we are on the right track, at least over the intermediate term.

ZBH put up a solid quarter in 2Q, the stock is up appropriately, but we do believe the #ACATaper is emerging on schedule into 3Q16.

Depending on your time frame, we do not see a catalyst specific to ZBH until later next week with the employment and subsequent JOLTS report. We are working on getting access to specific hospital claims data that will show us orthopedic procedures, but that may be beyond your tolerance or timeframe. One could cover and re-short later, although we have never been good at timing. In healthcare, trends are stable until they’re not, and it is very often tough to stay with a thesis when the price is telling you everyone thinks your’re wrong.

HOLX

To view our analyst's original report on Hologic click here.

In our view, Hologic's (HOLX) 3Q16 was as expected, where it mattered. Breast Health was disappointing in terms of product sales, showing a massive deceleration in year-on-year sales growth from the prior quarter. The #ACATaper continues to unfold away from HOLX as Hospital providers and other companies lowered guidance and missed expectations.

The #ACATaper will likely hit HOLX in their Diagnostics segment which had another good quarter, particularly for Cytology. We believe the US medical Economy will be showing material weakness next quarter beyond what we saw this quarter. We’ll update you next week on the Tomo-Tracker results for July. We think growth peaked in June, and sequential and year-over-year declines will be evident in the coming months.

TIF

To view our analyst's original report on Tiffany click here.

Tiffany (TIF) comps correlate pretty tightly with moves in the luxury PCE category.

TIF Comps have already led the category to the downside to date, but we think the important point to focus on is the fact that most of that underperformance has been due to poor demand for TIF in particular and less about the category (maybe the lack of Tourism traffic explains away a part of it). From here, we think the potential for meaningful downside is clear as the category, which has held up considerably well, weakens to the downside. That adds another leg down for the comp numbers at TIF. As a reminder, real luxury spending turned negative in the May PCE release.

LAZ

To view our analyst's original report on Lazard click here.

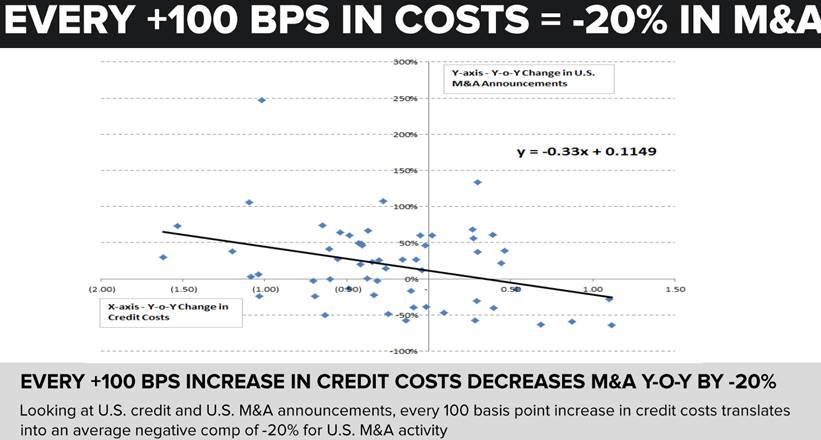

Lazard (LAZ) was unable to navigate the macro environment in its 2Q16 earnings print this week with a -26% year-over-year slowing in its main M&A advisory business. Our regression model flagged this outcome at the beginning of the year with corporate credit costs on the rise, cresting over a +100 basis point increase to start 2016. Based on 14 years of data, this outcome has resulted in a -20% decline on average in hyper-cyclical advisory revenues. Thus, the result was in-line with our expectations but well below Street estimates.

Lazard is still swimming upstream, with 1/3 of its M&A practice in Europe and it battling the new uncertainty caused by the U.K. referendum to exit the European Union. We think this will stifle deal volume in an already uncertain geography.

Furthermore, the Street estimates are still wildly high with 2017 at $3.30 per share, over +25% higher than our number. Thus, we don’t see the stock breaking substantially higher outside of bouncing around broadly with U.S. equities. Annualizing this quarter’s earnings results puts the EPS opportunity at $2.40 or $2.20 per share for 1H16. Either way, we don’t see a stock with lots of upside considering estimates need a substantial haircut.

WAB

To view our analyst's original report on Wabtec click here.

Our Wabtec (WAB) thesis continues to play out. We would caution longs that this is only the third quarter of down freight revenue, and both railcar and locomotive deliveries in the quarter remained well above likely ‘normalized’ demand.

FL

To view our analyst's original report on Foot Locker click here.

The emphasis NKE is placing internally to grow it’s DTC business (mainly e-comm) is bad for the traditional wholesale athletic space. We've done the math to see what this risk means for Foot Locker (FL).

What are the options for the retailer? It can either...

- Take a larger share of NKE’s incremental wholesale business, or

- Spend to grow the less relevant footwear brands like UA and AdiBok.

The first ain’t going to happen as FL has hit its limit with Nike. The 2nd requires both additional investment and something we haven’t seen in a long time which is NKE losing market share.

Based on our math for FY17 (that’s 2Q-1Q for FL), using the Street’s estimates, FL needs to add an incremental $330+mm to its US business to hit numbers. We think about $130mm comes from NKE, meaning we need to see an incremental $200mm from other brands. Hint – it’s not a slam dunk.

We continue to see FL as a short with multiyear growth headwinds as the Nike paradigm shifts.

LMT

To view our analyst's original report on Lockheed Martin click here.

No update on Lockheed Martin (LMT) but we reiterate our long call.