“When all is said and done, more is said than done”

-Lou Holtz

Unfortunately, when your primary “tool” is communication, “saying” pretty much = “doing”.

In the last 6 months, the Federal Reserve has pivoted from Hawkish (DEC hike) to Dovish (on market down), to Hawkish (April), back to Dovish (May Jobs Report bomb), and now Hawkish again!

For High-Frequency Flopping enthusiasts that equates to a rhetorical policy pivot approximately every 6 weeks.

And for a Fed pre-occupied with dampening volatility and pro-actively leading markets via carefully crafted rhetorical gradualism, they certainly seem to be running the uncertainty promulgation machine near full productive capacity.

As a thoughtful reader opined about the prevailing, domestic productivity malaise yesterday following the Fed Minutes:

Imagine all the collective speculation, all the sunken search and research costs, all the spurious activity surrounding “fed watching” was, instead, directed towards innovation and tangibly productive activity.

Then do the same for all the superfluous activity surrounding the manic forecasting of the unforecastable monthly NFP figure.

Viola, step function increase in productivity.

Doing instead of saying …. whoda thought!

Back to the Global Macro Grind…

Dude, you’re not long Latvia!

C’mon, everyone’s doin’ it. It’s a no-brainer, I think it’s in Central America too, so its gotta be good. I know a guy if you wanna get some!

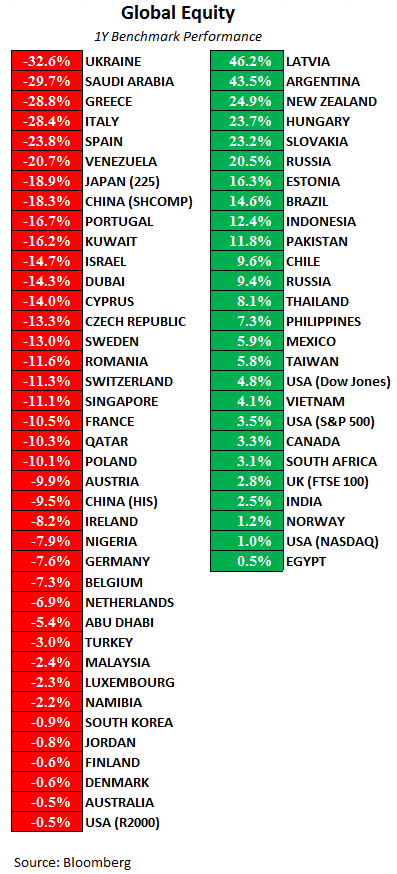

The table below, which we recently tweeted out, is a simple reminder that “the market” ≠ 1 domestic equity index. Macro investing is cross asset class and global.

Q. What do you call Helen of Troy after sunset?

A. Nitrogen (night Trojan)

Chemistry humor is rare, you take it where you can get it.

Q: What’s the most ironically named macro metric YTD?

A: Durable Goods ... where the early 2016 improvement has proved neither Durable nor Good?

Headline Durable Goods for June reported yesterday declined -4.6% sequentially and -6.4% YoY.

While the -59% MoM/-60% YoY decline in private sector aircraft orders was an outsized drag, most of the subaggregates mirrored the headline.

Indeed, Durables ex-Defense and Aircraft – which aligns most closely with what actual households buy – remained negative year-over-year (-1.8%) for a 4th consecutive month.

Core Capital Goods Orders, meanwhile, declined for the 17th time in the last 18 months, dropping -3.7% YoY while extending the most epic non-recessionary run of negative capex growth ever.

That number will drive a downward revision to tomorrow’s advance GDP estimate for 2Q but only modestly. With Retail Sales having its best quarter since 2014 (up +7.2% QoQ annualized), the growth juice remains in household spending as Consumption remains the only GDP Expenditure Bucket game in town.

Elsewhere across domestic macro yesterday, we got the latest update on sales activity in that forgettable, $22.5T asset class that is residential real estate.

We provided a summary update on Housing to Institutional clients yesterday. Since I haven’t touched on it in a bit in the Early Look, below is a recap of that note:

Pending Home Sales: Pending Home Sales rose +0.2% sequentially and +1% YoY. On an NSA basis, year-over-year growth decelerated to a 19-month low at +0.3% YoY.

With growth making new lows the last couple months, it’s worth quickly reviewing our expectations around demand in the 90% of the market that is existing sales.

Our Call: Our process is generally rate-of-change centric as being lazy long a negative 2nd derivative trend and an expectation for a conspicuous deceleration in growth is typically a losing proposition, as is the converse setup.

Our expectation since the beginning of the year was for demand growth in the existing market to continue to converge towards 0% against peak comps and subsequently run +0-2% during the mid-year period. With PHS printing negative YoY growth for the 1st time in 2-years on a seasonally-adjusted basis last month and NSA growth printing a 19-month low in June, that expectation has largely been realized.

So now what?

Comp-sternation: From here, PHS comps get modestly easier over the next 6-months which, at current levels of activity, equates to ~2.4% YoY growth over the balance of the year. While the potential for further reemergence of entry level buyers may provide some modest support over the nearer term, sales in the existing market having already mean reverted back to average levels of activity and the inventory environment will remain an upside constraint. In other words, what we think you’re playing for over 2H in a neutral-to-bullish case is low to mid-single digit demand growth. Also, notably, June PHS suggest modest downside risk to July EHS when the data are officially reported next month (8/24)

Reality's Reflection: If we were to Occam’s razor an explanation on the prevailing trend in housing it’s that it is largely reflecting the current underlying macro reality - which remains an underwhelming, stubbornly crawling expansion. Flat-to-mid single digit growth doesn’t necessarily make for a sensational fundamental “call” but it probably correctly characterizes current domestic fundamental macro and housing conditions.

With a relatively benign near-term comp setup, without a discrete large-scale catalyst (regulatory, fundamental or otherwise) and absent another outsized move in rates, we’d expect housing fundamentals and housing related equities to trade largely in step with economic and market beta over the nearer term.

And a last quick highlight…

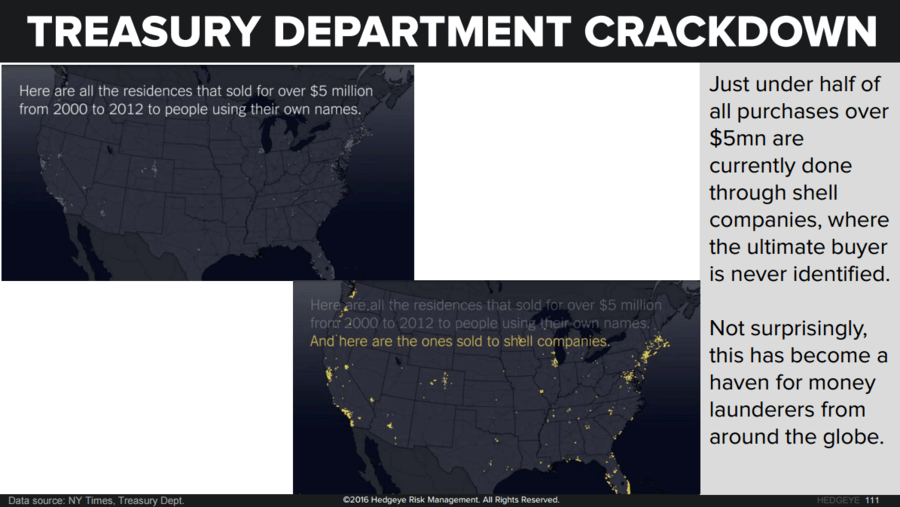

High-End Hit List Expansion: A couple weeks ago, I highlighted a Treasury Department initiative aimed at tracking high end real estate transactions in Miami and Manhattan in an attempt to crackdown on money laundering in the ultra high-end real estate markets.

With foreign demand having an outsized impact on prices in select markets and nearly 50% of foreign buyers purchasing properties over $5mn doing so through shell company LLCs, someone thought illegal activity was getting a little too frothy.

After just 4-months of investigation and evidence of significant criminal activity, the Treasury department announced yesterday that it will expand the program to all the boroughs of New York City, Miami-Dade and surrounding Counties, Los Angeles County, San Francisco and surrounding Counties, San Diego County and Bexar County in Texas. An Order that will take effect on August 28th.

Notably, the Treasury Department announcement came just a day after the British Columbia government unveiled a new 15% tax on Vancouver-area property purchases made by foreigners along with a capacity to tax vacant properties. (note: Vancouver = ground zero for speculative foreign capital flow). As our financials team highlighted, the impending foreign buyer fallout in the Vancouver area sits as a key component of the future deflation of the Canadian housing bubble.

Governments taking action, eh.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.47-1.62%

SPX 2134-2176

RUT 1185-1221

VIX 11.71-15.35

USD 96.47-97.97

Gold 1

To action above oration … and a shot for every time the media says what Janet will say at Jackson Hole over the next few weeks.

Christian B. Drake

U.S. Macro Analyst