HBI is our top short idea. We don’t like the Brands, don’t like Management, and don’t like the Company, but that alone is no reason to short a Stock (For an overview of our call see our May Black Book - Short the Tighty Whities: CLICK HERE). What is, however, is the fact that margins are at peak, on peak utilization rates and trough cotton prices, with competition accelerating on the high and low end, growth through acquisitions has become more expensive and higher risk, and the only CEO this brand has had as a public company is now stepping down after selling ~$90mm in stock over the last 2 years at peak prices. We have to ask…who is the incremental buyer of HBI with the stock trading at 12x EBITDA at the tail end of the economic cycle? We think once the dust settles on acquisitions and special charges, margins are headed lower to the tune of 400bps and we see 40%+ downside from current levels.

That’s the overview of our HBI call, with the relevant news being GIL’s earnings release this morning. The most important data point from our perspective is the trend in GIL’s branded underwear business which just stole an additional ~180bps of share YY taking the total to 9% of the US market. Understanding the market dynamics of the pressure on the low end perpetuated by GIL entering the market, plus the tepid demand among HBI’s traditional retail partners, provides valuable context to HBI’s decision to risk up with its acquisition strategy.

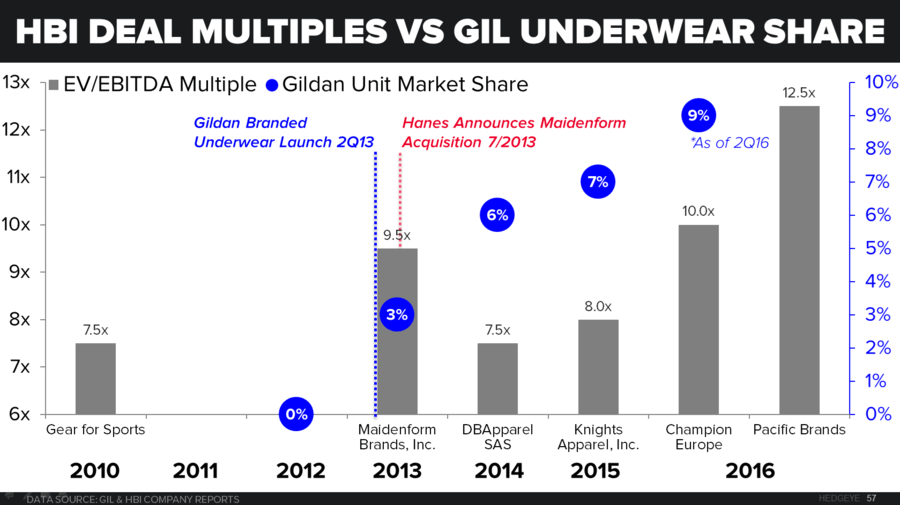

Gildan Taking Share

An outlier threat to organic growth for HBI has been the pressure applied at the low end by Gildan. Gildan launched its own branded underwear in 2013 and has been a thorn in HBI’s side ever since. The original belief was that GIL would likely consume private label market share, but as of this morning's 2Q16 earnings release, Gildan's unit share hit 9% in the Men's underwear market. Up 60bps sequentially from 1Q, and 180bps YY.

Think it doesn’t matter, think again. The men’s underwear market in the US is $5bn. That’s broken out into 28% market share for HBI, 24% market share for Fruit of the Loom, and 5% private label on a dollar basis. With the new comer GIL taking 9 points of share of units (5-6% in $) in its first 3 years of existence. That’s 5-6% of share in HBI’s largest single category that a) represents about 17% of the business and b) has come directly from the HBI’s key wholesale partners, which any way you slice it = lost market opportunity for HBI, with more pressure to come. On the flip side of that the appetite for additional inventory in basics appears to have dried up – GIL management cited negative unit volume growth in Specialty/National chains and flat to slightly positive in the mass channel. Who wants to be tied to a segment where competition is becoming more intense, at the same time wholesale volumes are trending lower as retailers plan more? Apparently not HBI.

HBI Paying Up For Growth

We don’t think it is a coincidence that at the same time Gildan dived into branded underwear, HBI turned into a serial acquirer – starting with Maidenform in July 13. Since then, the company has closed on an additional 4 deals (2 in the last month) all of which broaden HBI’s exposure away from selling tighty whities through wholesale doors in the US. Well and good, but that relationship discussed above (Competition ↑, demand ↓) has added a sense of desperation to HBI’s acquisition strategy – evidenced by the DD EBITDA multiples paid for marginal international assets to offset a declining core US business.

And at these prices, this year's deals have no immediate earnings accretion. Look no further than the updated guidance. When adjusting for the new acquisitions, HBI took up 2016 revenue guidance by $350mm and adjusted EPS guidance by $0.04. The $0.04 in earnings associated with the new Champion Europe and Pacific Brands is really just tax savings associated with debt raises in its higher tax jurisdictions, hence the guided tax rate change from LDD to HSD. That tax rate change alone is good for a $0.02 - $0.04 benefit in 2016, or all of the guided earnings benefit.

The key point from where we sit is, the company is guiding $350mm in incremental revenue from the acquisitions and ZERO EPS benefit this year. And, over the long term, it’s obvious that HBI plans to grow and clean up the newly acquired brands, but there is a lot of execution risk when slapping double digit EBITDA multiples on basics companies.

Other Callouts Relevant To HBI

Cotton Commentary

Cotton prices have bounced off the bottom, up about 30% off the March lows. Gildan management noted that should cotton stay at these levels for an extended period of time, it would warrant price increases in 2017. That is if the consumer/wholesale partners are willing to pay up – which we think is a pipe dream especially given how hard TGT and WMT are squeezing suppliers. More importantly the industry gross margin tailwind of the last 3-4 years is no longer a benefit, with more downward pressure as prices recover.

At HBI, the company hedges cotton out 6-9 months. Factor in the production process and it takes about 4-5 quarters for price fluctuations to flow through to the P&L. So we need to see that sustained price move to get a material impact to earnings, which we haven't seen yet, but for HBI a 10% move in cotton price is about a 50bps impact to gross margin, or a 4% EPS impact.