U.S. equity markets are backing off today ahead of a full week of central planning. (The Fed's policy announcement is tomorrow and the BOJ meeting on Thursday.)

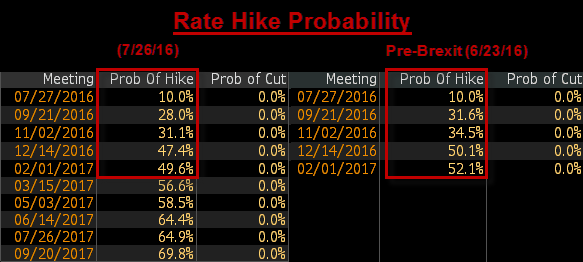

Market expectations for 2016 Fed rate hikes are now within spitting distance of pre-Brexit hike probabilities.

What a difference a month can make. Contrast this against the implied rate hike probabilities directly following the Brexit vote when rate CUT expectations for the July meeting spiked to 10%.

None of this is really shocking. In fact, it highlights the unbelievable amount of uncertainty surrounding Fed policy that's supposedly undergirding the recent rally to all-time highs.