Editor's Note: Shares of Buffalo Wild Wings were up 5.8% yesterday after it was announced that activist Marcato Capital Management had acquired a 5.1% stake in the company. In the institutional research note below, originally published on 6/13, Hedgeye Restaurants analysts Howard Penney and Shayne Laidlaw wrote that BWLD was "vulnerable to activism" and lay out the problems that have long plagued the company.

THE UPSHOT

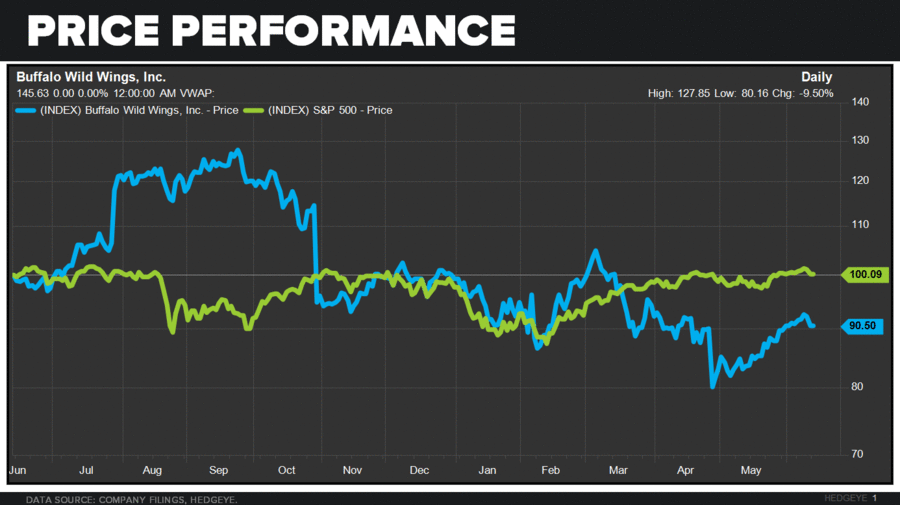

For the past two years, BWLD has underperformed the S&P 500 by 11% and is down 8% year-to-date. There is a very strong possibility that FY2016 is going to be a disaster for BWLD when the company posts negative SSS for the first time in 9 years and the second year of disappointing earnings growth. Although we remain very bearish on the Casual Dining industry overall, BWLD has a unique position within the industry to capitalize on their live TV offering, being a great place for people to gather and watch a game for three to four hours.

The recent decision for CFO, Mary Twinem to retire after a disastrous acquisition in 2015 suggests that the company has other issues to deal with. From an outsiders perspective, this move could be a sign that the business may have been financially mismanaged over the past few years. We highlight certain capital allocation concerns that could be improved to create significant shareholder value. More recently, the company’s track record when it comes to projecting their performance has come into question. BWLD has missed SSS for 4 of the last 5 quarters; and missed EPS for the past 6 quarters.

We are confident that the BWLD brand is not dead, but the company has had some missteps that have led to underperformance in the business. There is a lot an activist can do with a business like BWLD and in a slowing sales environment the chances of someone taking action could increase.

WHAT HAS GONE WRONG?

Strategic missteps

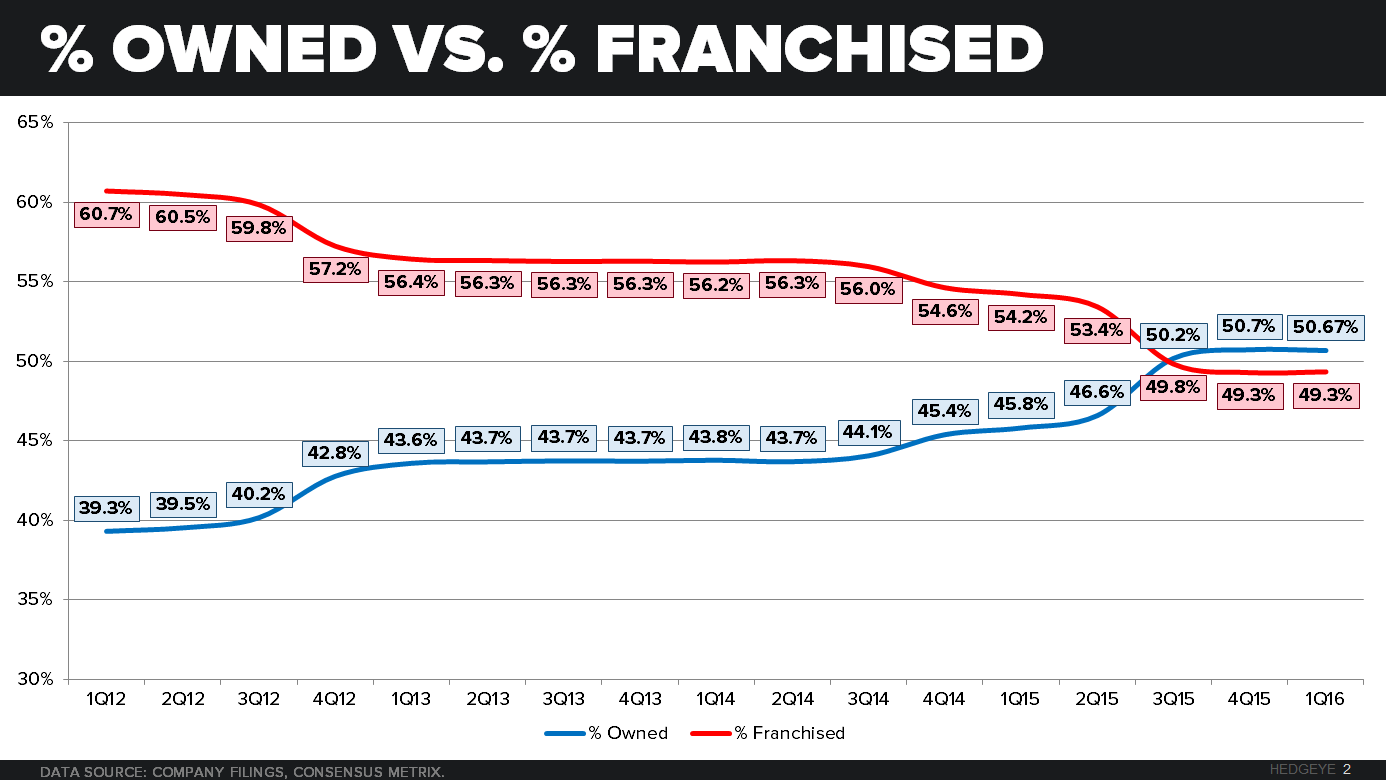

- Acquiring franchise stores increases business risk – BWLD went from 39.3% company-owned restaurants in 1Q12 to 50.7% company-owned in 1Q16. Why in a slowing sales; lower return environment would the parent company want even greater exposure to the volatility in the business?

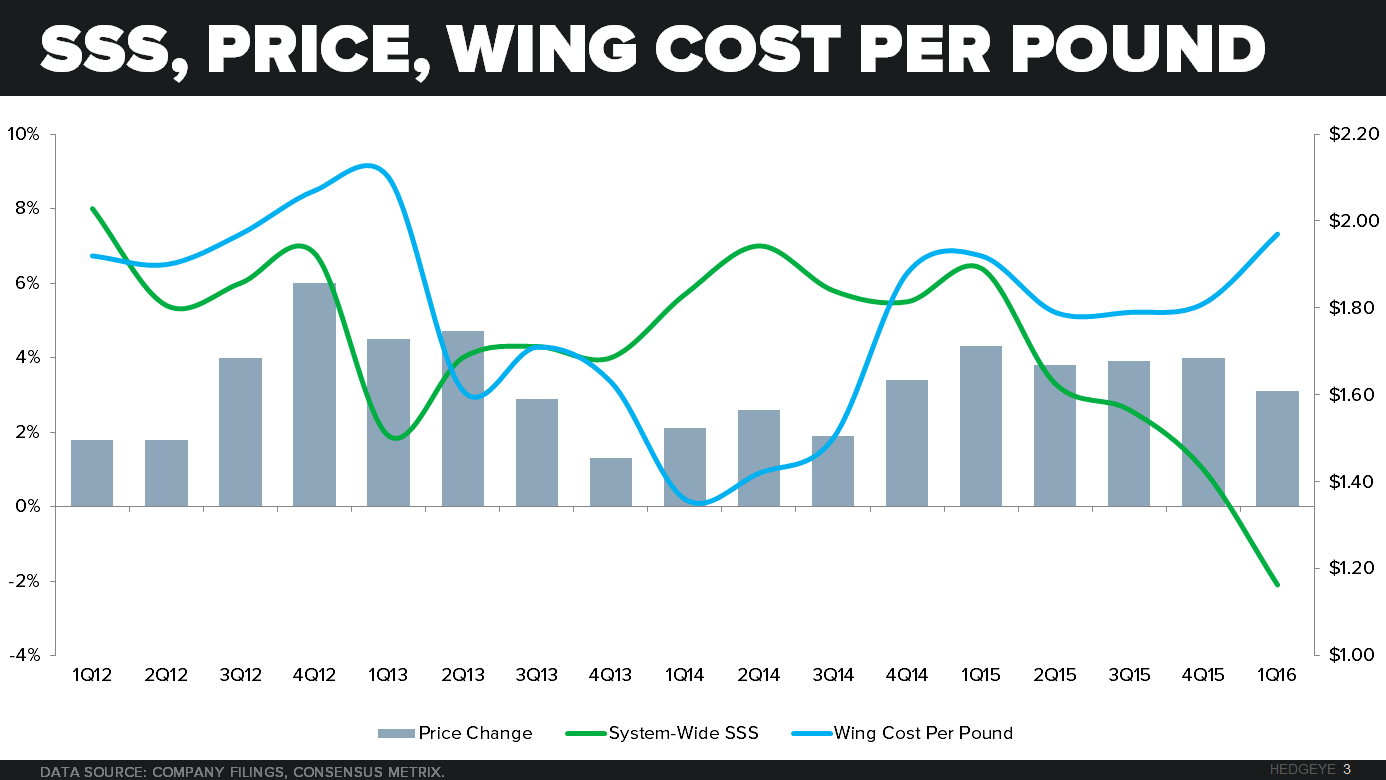

- BWLD has used price aggressively to drive same-store sales for years, but was increasingly aggressive in FY2015. Closing out 2015 with +4% price is likely to have an impact on performance, and will continue to have an impact throughout 2016.

Distracted management

- Management has diversified away from the core Buffalo Wild Wings brand, adding in R Taco and PizzaRev.

- They have a minority interest in Pie Squared Holdings which is the operator and franchisor of PizzaRev a California based fast-casual pizza restaurant. In addition they own and operate PizzaRev restaurants in Minnesota.

- In addition, BWLD has majority interest in Rusty Taco, Inc. the operator and franchisor of R Taco.

- They currently franchise two (2) PizzaRev restaurants and four (4) R Taco, with six (6) franchised R Taco’s.

- With the total number of Buffalo Wild Wings units standing at 1,190, these peripheral concepts merely serve as a pipe dream for growth, and more likely distract management from their core concept, which has plenty of issues in its own right.

Poor capital allocation

- Excessive new unit growth - new unit returns (new unit productivity) are slowing as they increase their unit count into a slowing restaurant environment.

- The company announced its first ever share repurchase authorization in November 2015.

- The company currently does not pay a dividend

- BWLD’s net debt / LTM EBITDA currently stands at 0.15x which is far below the industry norm, leaving them plenty of room to increase leverage and return some to shareholders.

WHAT CAN BE DONE TO CREATE SHAREHOLDER VALUE

The activist game plan for BWLD is clear cut and can create meaningful long term value for shareholders:

-

Focus On The Core

- Remove the distraction of non-core brands.

- Slow new unit growth

- Operations must be 100% focused on improving the performance of the Buffalo Wild Wings concept

-

Return Cash To Shareholders

- BWLD can drive better shareholder returns through share repurchases and paying dividend.

- With BWLD’s net debt / LTM EBITDA currently at 0.15x, they have ample room on the balance sheet to increase leverage and return cash to shareholders

-

Refranchise Restaurants/Cut G&A

- There is significant value from an operational perspective that can be gained by refranchising underperforming stores, especially from trimming corporate G&A

- Asset sales will lead to incremental share repurchases

- Improve the quality of the revenue stream to drive the multiple higher

-

This Board is Ripe For a Change

- There are three people on the Board that have been there for 17+

- The average age of the board is 63

- Given the increasing role of technology in the industry and the company, nobody on the board has the relevant experience