Below are our analysts’ new updates on our fourteen current high conviction long and short ideas. As a reminder, if nothing material has changed in the past week which would affect a particular idea, our analyst has noted this. We will send Hedgeye CEO Keith McCullough's refreshed levels for our high-conviction Investing Ideas in a seperate email.

IDEAS UPDATES

TIP | TLT | GLD | JNK

To view our analyst's original report on Junk Bonds click here, here for TIPs and here for Gold.

After a couple weeks of our long positions moving against us relative to the broader market (good thing they haven’t all year!), the good news is that the market is at all-time highs if you were long the index. The bad news? You’re still underperforming long-term Treasuries in 2016. Moreover, you’re long one of the Top-3 "most expensive" markets of the last 100 years. For the record, we remain skeptical of overly optimistic consensus expectations for an earnings rebound by Q4 of 2016.

Please see chart below. The most important point to make here is that the current cycle-high forward multiple is slapped on earnings expectations that are a sea of green for every sector starting in Q4 of this year and double digits in Q1 and Q2 of 2017 (see last week’s write-up for more color)

So, despite a two-week period of underperformance for our Investing Ideas macro positions, here's the S&P 500 YTD scorecard against what have been our active calls for all of for 2016:

- TLT: +15.1%

- JNK: +7.2%

- S&P 500: +6.4%

Of course, prospective returns are much more important than calling out what’s already happened. So we’ll dig into an important scenario analysis laid out by Senior Analyst Darius Dale in with regard to Q2 GDP which gets reported next week (Again, see last week’s note for a detailed analysis on how retail sales drives GDP). To quote Darius:

- “Next Friday’s Q2 GDP report is likely to come in better than expected – perhaps by a significant degree.

- While backward-looking in nature, any such “beat” will likely affirm the recent optimism in the domestic equity and credit markets – optimism that we’ve admittedly been on the wrong side of.

- That being said, however, we’re inclined to fade such optimism given our expressly dour outlook for domestic economic growth from here.”

So what does this all mean? It means that the time between the FOMC’s July 27th meeting and its September 21st meeting is likely to contain a meaningful degree of hawkish rhetoric out of various vocal Fed Heads. That may serve to catalyze incremental convergence in the factor exposures we’ve been bullish and bearish on in the YTD.

To sum things up on inflation expectations, we could see a brief period of a Hawkish policy pivot. However, with growth continuing to track a decelerating trend in our model in Q3 and Q4, with 1) difficult PCE comps (consumer expenditures) and 2) easy inflation comps, we want to stick with our allocations to growth slowing and inflation picking up in the latter part of 2016.

DNKN

To view our analyst's original report on Dunkin Brands click here.

Dunkin Brands (DNKN) reported 2Q16 earnings this past Thursday, which showed significant weakness in the business. Coming off the 1Q16 comps at Dunkin’ U.S. of 2%, they slowed to 0.5% in 2Q16, missing consensus estimates of 1.0%. Breaking down the comp, traffic was negative 240bps, and there was slightly less than 300bps of price on the menu.

It was not just a problem isolated to Dunkin’ U.S. either. Their other three segments missed expectations as well. Management indicated that franchisees remain cautious, with a level of uncertainty surrounding the political picture, regulations and labor. They even noted some franchisees are sitting on sites to see who will be our next president.

The significant price that franchisees have been taking coupled with a slowing QSR space is having a significant effect on DNKN and we do not anticipate the weakness in the the company's business to dissipate anytime soon. We remain SHORT.

WAB

To view our analyst's original report on Wabtec click here.

We expect Wabtec's (WAB) earnings report on July 25th to contain a number of unusually important elements. WAB’s report and guidance will test the sustainability of 1Q 2016’s Freight segment decremental margin, which the 10-Q indicates was driven by lower Material costs.

These favorable decremental margin expectations are now imbedded in 2H 2016 consensus estimates, and we expect the recent snap back in steel prices to have a significant 2H16 impact. While Materials costs went unmentioned in both the press release and earnings call, the company has apparently subsequently claimed mix as a factor; we do not find that claim credible.

HBI

To view our analyst's original report on Hanesbrands click here.

Hanesbrands' (HBI) adjusted operating margin is at an all-time high of 16%, a level we think is clearly unsustainable. Excessive non-gaap charges are pumping up the margin level, as well as operating its manufacturing above 90% utilization.

Given the similar product assortments and the manufacturing profile, the closest comparable company to Hanesbrands is likely Fruit of the Loom, which is owned by Berkshire Hathaway. We estimate its current margin to be in the area of 12%, which is 400bps below HBI's margin. HBI does not have the brand strength to maintain a margin level that much higher than a large competitor.

We think as demand softness continues, and organic growth slows, utilization will trend downward and HBI's operating margin will move down to a level closer to that of Fruit of the Loom.

MDRX | ZBH | HOLX

To view our analyst's original report on Allscripts click here, here for Zimmer Biomet and here for Hologic.

Below is a HedgeyeTV Q&A with Healthcare analysts Tom Tobin and analyst Andrew Freedman in which they discuss specific implications for Investing Ideas companies like Allscripts (MDRX), Zimmer Biomet (ZBH), and Hologic (HOLX). Other companies covered include AHS, ATHN, ILMN and MD.

Tom and Andrew also recap last week's Themes Presentation, which included a comprehensive overview of our #ACATaper and Healthcare Deflation themes with new datasets and analysis.

Click here to access the associated slides.

(**Also, click here to read an unlocked institutional research note on athenahealth (ATHN) written by our Healthcare team on 5/20. "Wrong call into print, but we did flag short-term risk after ATHN CFO departure," Hedgeye Healthcare analyst Andrew Freedman wrote.)

TIF

To view our analyst's original report on Tiffany click here.

Swiss Watch Exports numbers are one of the best indicators that we can find to gauge the global demand for luxury items - particularly jewelry. Of course, watches have their very own demand constraints and Tiffany (TIF) is underexposed to the category -- but the iWatch, FitBit, and other connected fitness wrist wear, we'd argue, don't compete with items priced above $3,000, which was down 19.5% for the month.

Looking at the trend in TIF comp sales vs. the global Swiss Watch exports numbers paints a pretty tight correlation between the two metrics, with the two most recent Swiss Watch export numbers showing a sequential deceleration in the YY trend. The only problem is that TIF Consensus estimates currently expect a reacceleration in comp trends sequentially on a 1yr and 2yr basis for 2Q16 and the balance of the year. With a positive comp bogey embedded in numbers for 4Q. We think that's a pipe dream.

LAZ

To view our analyst's original report on Lazard click here.

Lazard's (LAZ) advisory business had a nice win during the week announcing the mandate to assist in the $32 billion acquisition of U.K. semiconductor ARM Holdings by Softbank. The deal was the first indication that the fallout from Brexit has been viewed as a buying opportunity as the Japanese domiciled Software has been “looking” at the U.K. based ARM for over 10 years according to the Softbank chairman.

The sizeable deal is the first in about 2 quarters for Lazard and is a nice respite to the vacuum of activity that has ensued throughout the first part of the year. If the deal actually gets completed, Lazard should take in between $35-45 million, a nice payday to say the least. However, we see only a ~15% bump to the quarterly advisory run rate of $250 million for the firm’s M&A business.

With activity trending down -40% year-over-year, it will take more than one deal to get the stock out of the current fundamental weakness caused by a moribund M&A environment. LAZ reports its 2Q16 earnings this week on Thursday the 28th and, without some serious jawboning about an improvement in sentiment and the pipeline, they will be acknowledging the soft landscape. We see more downside for the stock.

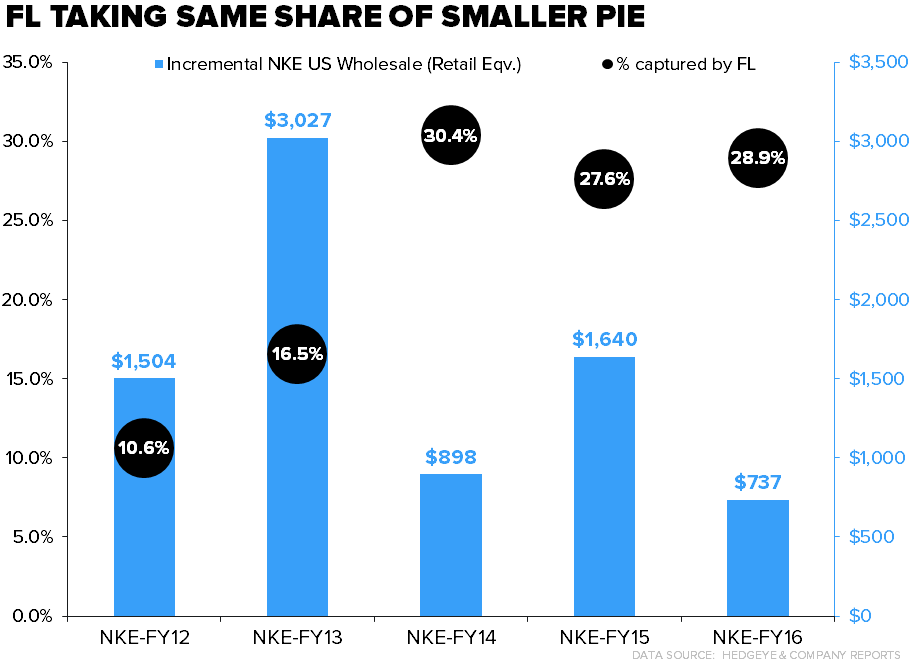

FL

To view our analyst's original report on Foot Locker click here.

Nike filed its 10-K this week. The punchline is that trends are not good for traditional wholesale partners, particularly Foot Locker (FL).

NKE’s North American wholesale business was up $737mm dollars. Of that $700+mm, FL captured 29%. That’s up from previous years when NKE was growing like a weed, but in-line with the prior two years. All in, that’s an incremental $215mm to FL, good for 4% growth in its US business. However, that’s about half the 8% average growth rate NKE wholesale has handed to FL on a silver platter over the past 4 years.

Going forward, assuming FL still gets the same allocations from Nike (despite the fact that FL was as bearish as it’s ever been on the brand on its most recent call), we think the NKE benefit gets cut in half again in 2017. This changing dynamic means that unless we see unprecedented growth/share gains from Adidas and/or Under Armour, FL sales growth expectations are way too high.

LMT

To view our analyst's original report on Lockheed Martin click here.

Although Lockheed Martin (LMT) is coming off a strong Q2 report that showed sales up 11%, cash from operations up 16% and increased guidance for the rest of the year, there are two areas of caution. The first are the interminable negotiations which began 10 months ago to definitize the contract valued at ~$10B for delivery of 150 F35s from Lot 9 (FY 2015) and Lot 10 (FY 2016). The Lot 9 aircraft are well down the construction line and the Lot 10 orders are now beginning their two year journey to delivery.

LMT CEO Marilyn Hewson said the company is carrying $900M to keep supplier operations flowing efficiently but that those company cash requirements are going to increase astronomically as the aircraft move closer to completion without a contract. Even the UK Defense Minister begged the Pentagon this week to quickly close the deal as the delay begins to impact UK companies. The deal is reportedly going to close “soon” but meanwhile LMT is out the cash.

The second area is Turkey. The turmoil there has resulted in the arrest or removal of over 40,000 military and civil servants to include 1/3 of the general officers and relief or removal of over 6,000 other military commanders and personnel. There are now apparently insufficient pilots to man the country’s F16s.

Even after the purge passes, the remaining personnel will be focused inward and there will be questions of loyalty. With much of the coup reprisals focused on the air force, it seems doubtful, even in the best case, that Erdogan will be enthusiastic about moving quickly on Turkey’s plan to buy 100 F35s beginning with two acft this year.

We believe that there will be delays.