“How in the world can earnings go up if nominal GDP is rising by less than wages?”

-Jeffrey Gundlach

A few years ago @Hedgeye we took the Briggs-Myers Personality test (BMTI).

I scored as a “Thinking Introvert” which probably explains why I'm comparatively better at generating written analysis than delivering extemporaneous verbal content on Hedgeye TV.

I’m okay with that. It’s also why we have a team … and a psychologically diverse one according to the intra company dispersion in test results.

The BMTI is cool but there’s a simpler and arguably better Street version. #Broscience, conceived by the bro’s, for the bro’s.

Here it is: Watch how someone parks their car.

Style and manner of parking offers a fairly clean insight into a person’s personality. Think about it.

Back to the Global Macro Grind…

You can get a fairly clean insight into how a person’s positioned by the nature of the questions they ask.

We ask and receive a lot of questions daily.

Because our business model carries no conflicts of interest, we’ve gradually become a kind of cogitation hub and a nexus for feedback, interaction and idea generation.

That was an objective, not a byproduct of the Hedgeye operational vision. We’ll always get things wrong, but “failing fast” and the cultivation of passionate players in perpetual pursuit of collective and personal evolution is our cultural hedge against staying wrong.

Anyway, I chose the Gundlach quote for a few reasons.

- It relates directly to our 3Q16 #ProfitCycle Macro theme.

- We have the same suspect opinion of consensus expectations for high-teens S&P500 earning growth in 2017.

- It’s great when name guys make pithy, off the cuff comments like the underlying basis for the assertion is obvious even to non-institution/non-macro investors.

- It captures the collective angst and questioning that currently pervades our inbox.

On point #4 – while the phraseology varies, most of the more recent questions and discussion distill down to “now what?”

Multiple Expansion – with forward earnings multiples making new highs - has driven most of the post-Brexit retrace in prices.

And with Utilities PE’s at their highest ever, performance spreads between cyclical and noncyclicals at peak, small caps trading at a discount to large caps and yields near all-time lows, late-cycle, slow growth positioning has (rightly) become as crowded as it’s ever been.

And because growth is not accelerating, the chief market purveyors of Panglossianism and serial thesis drift have coalesced around the hope for a further collapse in equity risk premiums as the justification and catalyst to drive further price appreciation.

Recall, the equity risk premium (ERP) represents the extra return required for holding equities over “risk-free” government bonds. Thus, most risk premium based models are relative valuation models that value stocks relative to bonds.

So, conceptually, what’s embedded in the call for a falling ERP?

Equity risk premiums have already come in a bit so any further decline will be the result of a move toward historic lows. A move to all-time low spreads for equity risk premiums relative to bonds that are, themselves, already in unchartered valuation water basically equates to an expectation for peak & sustained complacency.

In other words, the hope that NIRP drives ERP towards NERP in some kind of clean, linear fashion is a flimsy conceptual framework on which to anchor an investment strategy and stocks need a tangible fundamental development to help them grow into those multiples and drive prices higher.

Which brings us back to earnings expectations.

Let’s break Gundlach’s comment down into discrete parts to get a better feel for the intuition and implications:

First, why do we care about nominal GDP?

Nominal GDP, by definition = aggregate national income.

Subtract out personal income, depreciation, business taxes and add back government transfers/subsidies and net factor income from abroad and you have corporate profits.

The easier way to think about it is this: National income can either go to labor or capital (i.e. businesses) and while accounting measures of profits and GDP can vary from quarter to quarter the larger trend in Profits is invariably tethered to Income – and particularly so when productivity growth is weak like it is now and unable support margin improvements.

Indeed, since the interest rate cycle turned in 1980, Nominal GDP growth has averaged 5.5% while Corporate Profit growth has averaged 6.6%.

The trend in profitability is also cyclical and that’s important.

- Profits rise faster than costs in the early-to-mid part of the cycle as businesses continue to economize on labor and growth in sales/output rises faster than payroll growth.

- Historically, labor’s share of national income rises at the tail end of an expansion when the labor market tightens and after growth and profits have been strong for a protracted period.

As the chart below illustrates, Corporate Profits rarely grow above 15% on an annual basis and even more rarely at this point in the cycle.

This cycle is not proving different, which takes us to the 2nd part of Gundlach’s comment about nominal GDP rising less than wages.

- With productivity declining and employment growing at a premium to output, unit labor costs are rising as is labor’s share of nation income.

- Input costs are rising faster than output prices - a point we’ve made before but one that’s worth re-highlighting. If the price to produce something (unit labor costs) is growing faster than the price at which that something can be sold (implied by the GDP deflator) then margin pressure will remain ongoing….

- …. This is Gundlach’s point – if aggregate wages are rising faster than aggregate income (i.e. Nominal GDP), any earnings growth becomes a challenge, let alone an expectation of earnings growth to sustainably run 5X nominal GDP. Sure, record repo activity and an overindexing to the goods/industrial economy could provide relative support to S&P500 earnings but that doesn’t negate the underlying fundamental reality.

- Further, in a situation of slack demand and waning productivity, employment gains become bittersweet. A rising employment-to-population ratio is paid for via corporate margin compression.

If you’re finding this discussion too tedious for a sunny, summer (Friday) morning, I’ll leave you with this:

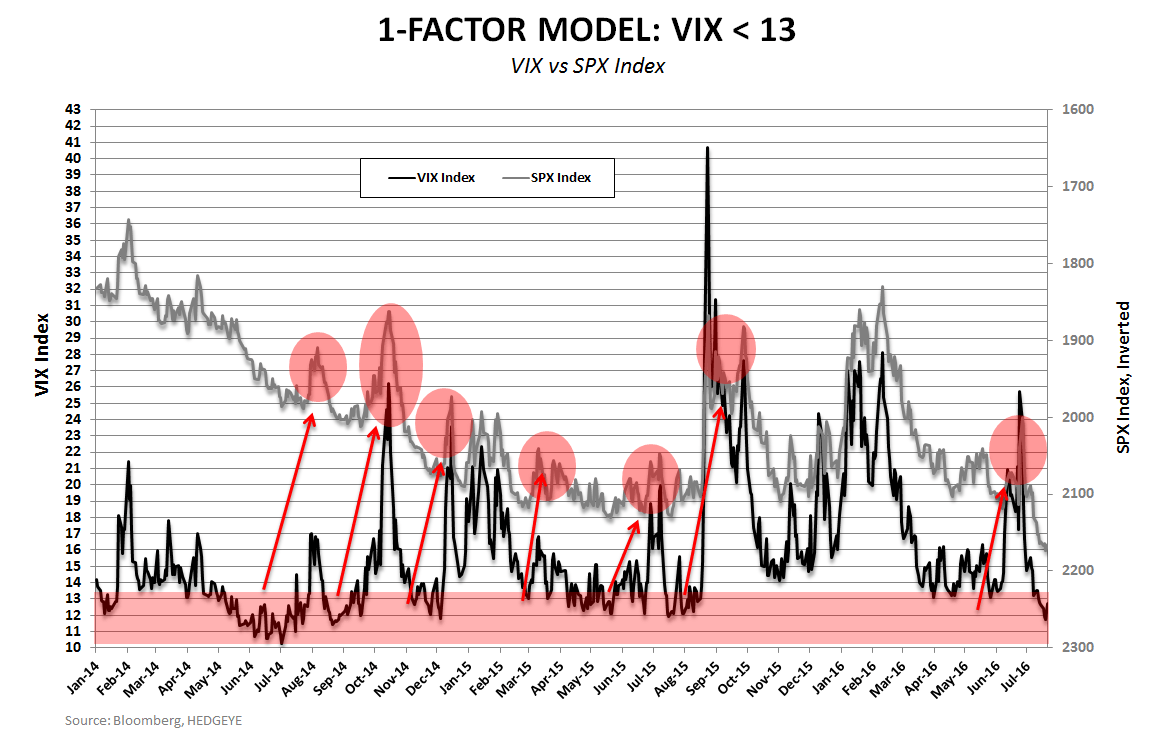

1 Factor Model: In the Chart of the Day below we simply show VIX vs S&P500 (S&P500 is inverted on right axis).

What you’ll simply notice is how simply effective it is to take down gross exposure and tighten net exposure when VIX goes <13.

Global risks haven’t “greatly moderated” so building exposure into VIX 10/11/12 embeds the assumption that those risks cumulate latently with no impact on risk premiums or prices. That seems like a pretty heroic assumption.

Yes, the current expansion still has some runway but the cycle will continue its interminable negative 2nd derivative march and it won’t waive curfew just because you want to stroll home late from the pro-cyclical party.

Risk manage as best you can by understanding the prevailing, underlying macro reality within the context of consensus’s expectations for it.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.38-1.65%

SPX 2129-2180

VIX 11.55-16.93

USD 95.87-97.52

Gold 1311-1365

Have a great weekend,

Christian B. Drake

U.S. Macro analyst