“I like my money right where I can see it: hanging in my closet.”

-Carrie Bradshaw

Post Trump parading around Cleveland, we’re all well aware of what it looks like to be big time. And I mean big time. Big Daddy Rich. Money oozing out of their flow. Really expensive shoes and suits. These people are so rich, they don’t need helicopter money.

Admittedly, it doesn’t always go over well… but in all of my macro meetings these days, I delve into what I think is one of our better ideas in Consumer Discretionary right now – shorting a certain kind of rich people.

And not just people who have money – that means we’d be shorting ourselves! I mean the people who, fully levered and lathered up in the illusion of their “wealth”, are about to meet their maker – it’s called mean reversion.

Back to the Global Macro Grind…

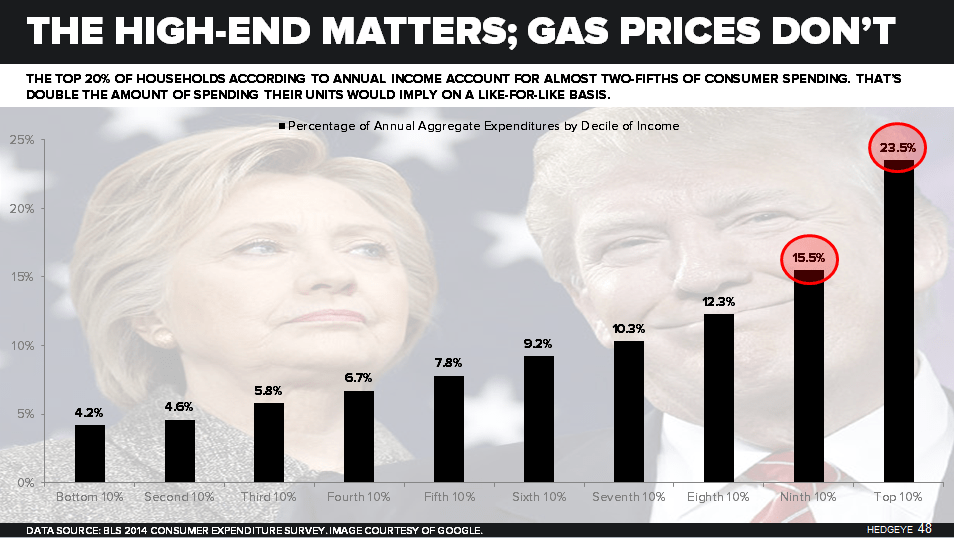

In today’s Chart of The Day is slide 48 of our current Q3 Macro Themes deck. It’s titled “The High-End Matters” and it shows that the Top 20% of US Households account for 39% of US Consumer Spending. That’s not a typo.

Looking at the percentage of annual aggregate US consumer expenditures by decile of income:

- Top 10% = 23.5% of consumer spending

- Ninth 10% = 15.5% of consumer spending

- Bottom 30% = 10.6% of consumer spending

Yeah. The Top 10% is killing it. They own 84.5% of US Financial Assets. The poor bastards in the Bottom 50% (lots of peeps) own 1%. That’s probably why plenty of card carrying Republicans are becoming politically “flexible” enough to associate with Trump.

You see, when you have to start every sentence with how big time you are – you know, how rich and famous … and generally just nailing it in everything that you do… there’s some implied insecurity in that. And there should be.

Another chart that we often show to remind you of the mean reversion risks associated with someone who acts like they are big time (all of the time) is US Household Wealth as a % of Disposable Income:

A) It just rolled off an all-time high of around 655%

B) When it rolls off #TheCycle high, it always crashes

To be fair, there’s always a chance that “it’s different this time”… and nothing (other than US Equity Volume, European and Japanese Equities, etc.) ever crashes again… but I don’t buy lottery tickets.

Measurable mean reversion risks complimented by real-time data is how I roll.

On an economy-wide basis, the “wealth effect” (i.e. how sweet the Trump Jr. slick back flow is looking at the highs) is in the process of rolling off its Q1 2015 #CyclePeak. That’s why the Fed has been desperate to protect the SPY house.

Newsflash: the super-high-end ballers I’m talking about didn’t make it with their daddy’s Long Bond fund. When their net worth slows, their spending slows. That’s why US Luxury Goods Spending is running at a cycle-low of down -2.7% year-over-year.

That’s probably why you’re seeing headlines like:

- “Christie’s and Sotheby’s High-End Art Sales -25-33% year-over-year”

- “This is bs. We demand helicopter-money!”

One of the super-rich places that my colleague and Sector Head of Demography Research, Neil Howe, has written about lately is Silicon Valley. I know. They know everything.

I’m sure they know Tech Employment is slowing and VC funding to the area was down -14% year-over-year in the 1st half of 2016. There’s definitely not a bubble in “wealth” there.

That said, with the recent addition to our Research Team – Technology Sector Head, Ami Joseph – we’re going to ham & egg it for the next traverse of Nasdaq 5100 and see if we can find ourselves some obscene corporate behavior to sell into.

Not to be confused with the Nasdaq all-time-bubble-high that you could have got sucked into when “the chart looked good” at this time last year (Nasdaq 5219 turned into a -19.3% draw-down by FEB 2016), this one is a lower-high on decelerating volume.

Yep. Yesterday’s Total US Equity Volume was down -17% and -22% vs. it’s 1-month and 1-year averages, respectively. At the all-time highs, who is crushing it? Or, are they about to get crushed again? From this stage of #TheCycle, crush or be crushed, I guess.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.36-1.65%

SPX 2125-2184

NASDAQ 4

VIX 11.53-16.93

USD 95.99-97.45

Gold 1311-1370

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer