Q2 GDP ↑ (vs. Q1) = U.S. Dollar ↑ = Rates ↑ = Reflation (i.e. commodities) ↓ = Fed hawkish

That's our latest thinking on the current macro setup. Here's analysis from Hedgeye CEO Keith McCullough in a note sent to subscribers earlier this morning:

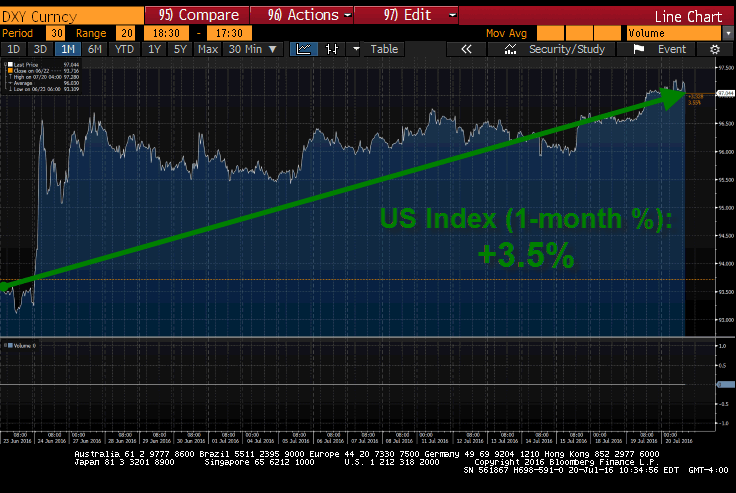

"The #StrongDollar move continues as consensus remains A) bearish on USD (see net positioning in CFTC futures & options data) and B) finally too dovish on what the Fed might do in SEP – what slows this down if we’re right on the Q2 sequential GDP acceleration as European and Japanese economic data continues to slow? Still bearish on Euros."

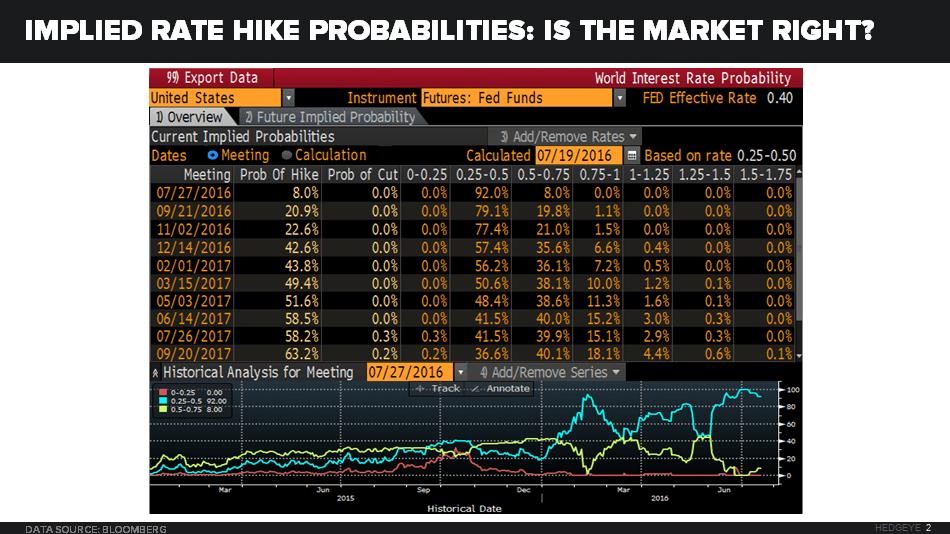

Note Fed Funds futures' current rate Hike Probabilities:

- JUL meeting = 8%

- SEP meeting = 21%

- DEC meeting = 43%

On #StrongDollar induced #Deflation...

McCullough writes:

"Oil continues to break-down as the USD continues to threaten a breakout – WTI down -1.4% yesterday takes it -7.1% in the last month as the inverse USD correlation there remains as real as it is for the CRB Index (down -1.1% yesterday to 186 and signaling bearish TREND @Hedgeye); WTI immediate-term risk range now = $43.91-46.65."

... Cue the Fed hawks:

- Atlanta Fed President Dennis Lockhart: “I wouldn’t rule out as many as two” rate hikes.

- “We should be looking toward removing accommodation,” said Robert Kaplan, president of the Federal Reserve Bank of Dallas. "We just should do it in a patient, gradual way.”

That's just in the past week.

What does this mean for investors going forward?

In the past few days, Hedgye CEO Keith McCullough has been trimming exposure to our favorite Macro idea, Long Bonds (TLT). We'll be happy to buy them back on selloffs (especially given our bearish outlook for Q3 GDP).