Editor's Note: Below is a brief excerpt and chart from today's Early Look written by Hedgeye CEO Keith McCullough. Click here to learn more.

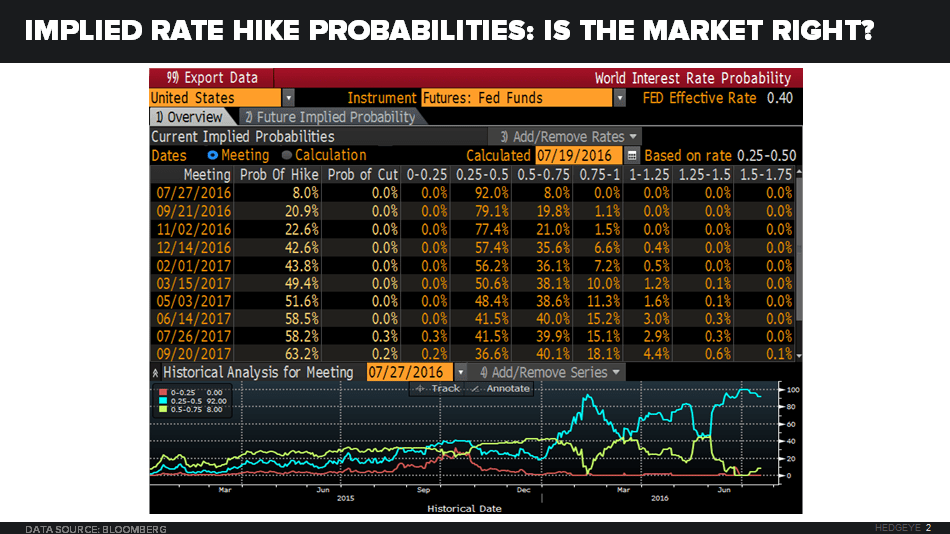

"... Looking at the implied market probability of another hike, across durations:

- JUL meeting = 8%

- SEP meeting = 21%

- DEC meeting = 43%

For now, I think those SEP expectations are too low. If I’m right on that, rates will keep making a series of higher-lows and Fed funds futures will continue higher until we get another jobs report bomb (PS. don’t rule that out)."