“We must consider how some bugs are not detrimental but fundamental to life.”

-Dr. David Perlmutter

I’ve learned more in the last week than I’ve learned all year and it had nothing to do with markets. It had everything to do with my growing gut.

“Meet Your Microbiome” is how neurologist (and gut doctor), David Perlmutter introduced me to reality in what has been nothing short of a fantastic book everyone should read called Brain Maker.

“The Greek physician and father of modern medicine, Hippocrates, first said in the 3rd century BC that all disease begins in the gut.” Same thing goes for Long Bond Bulls. All corrections begin with this thing called #GrowthAccelerating.

Back to the Global Macro Grind…

Talk about Recency Bias… I’m in my hotel in Chicago this morning… and for breakfast, instead of my usual, I ordered “The Fitness Trainer!” Berry parfait yogurt, eggs, mixed bell peppers, baby spinach, scallions…

But my gut isn’t deflating. Weird.

With a sequential (i.e. quarter-over-quarter) surprise to the upside in Q2 GDP, the former Perma Bull narrative (“Reflation”) is. With the US Dollar at a 4-month high, Commodities (and Oil) don’t like that inasmuch as Long Bond Bulls shouldn’t.

The way this macro pivot works is pretty straightforward:

- Q2 US GDP accelerates vs. Q1 as both European and Japanese growth continues to slow

- US Dollar becomes the relative winner in the Currency War

- Rates rise off their all-time lows

- Reflation (Oil down -7% in the last month) deflates

- The Fed corroborates USD strength with hawkish commentary that they nailed it all along

Again, and I want to be crystal clear on this… so let me write again, again…

A sequential acceleration is what we call a TRADE. And TRADES are not TRENDS (3 months or more, multiple quarters). All a Q2 GDP acceleration ensures is a Q3 sequential deceleration back to bearish TREND.

If that’s too “short-term” for you, stop reading and start pounding some empty carbs. As the authors of #GrowthSlowing, “all-time-lows in bond yields”, etc., I think my research team and I should have a pretty good handle on how to trade this.

Bought a bond, sold a bond…

That’s right. If you don’t like “short-term trading”, tell your boss you are risk managing. That’s what I signaled when I told subscribers to “sell-some” Zeroes (ZROZ) in Real-Time Alerts yesterday. We call it risk managing the range.

For something like the 10yr US Treasury Yield, here’s what I mean by that:

- The low-end of the immediate-term TRADE risk range = 1.35%

- The top-end of the immediate-term TRADE risk range = 1.65%

- Intermediate-term TREND resistance for the 10yr yield = 2.03%

In other words, if you want to actively risk manage the range of consensus finally being LONG what’s been our Best Idea on the long side of macro for a year now, you sell bonds on rallies and patiently buy them back on selloffs.

Patience has been (and will continue to be) the key to profiting from both cyclical and secular #GrowthSlowing.

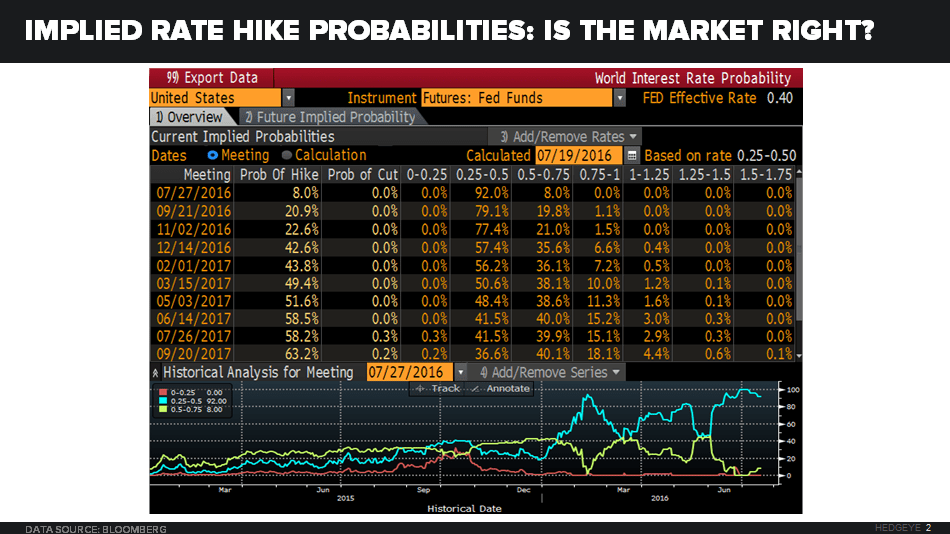

Another way to “play” the short-term higher-low that my model is signaling in the 10yr Yield is via Fed Fund Futures. Those are the macro market’s expectations of when (and if) the Fed actually has the spine to “raise rates.”

Looking at the implied market probability of another hike, across durations:

- JUL meeting = 8%

- SEP meeting = 21%

- DEC meeting = 43%

For now, I think those SEP expectations are too low. If I’m right on that, rates will keep making a series of higher-lows and Fed funds futures will continue higher until we get another jobs report bomb (PS. don’t rule that out).

The other thing that should keep happening on that is a continuation of what I absolutely love in life – the value of my hard earned currency appreciating = #StrongDollar.

And all of that “reflation” hope, fully loaded with consensus being long things that have been tethered to a rising Oil price (think ISMs, PMIs, Industrial Stocks) should deflate at a faster pace than my gut seems to be, despite feeling smarter about it.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.35-1.65%

SPX 2115-2188

NASDAQ 4

VIX 11.50-17.04

USD 96.11-97.51

EUR/USD 1.09-1.11

Oil (WTI) 43.91-46.65

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer