I think you'll enjoy this issue of "About Everything." It's on the decline of movies as an economic industry and as a cultural institution. Just last week, Variety published the latest--and one of the best--examinations of why movies are in trouble. Box office revenues are stagnant, movie-goers are declining, and a growing share of all revenues go to a declining number of mega-blockbusters. Fun fact: In 2015, the five top movies accounted for 25% of all box office revenue, up from just 16% from 2000 to 2013.

You may also like the Hedgeye Q and A on this piece that I did on July 21st: CLICK HERE to watch.

THE LAST PICTURE SHOW

WHAT’S HAPPENING?

The film industry is struggling. Ticket sales have been on a downward tilt since 2002, and this year U.S. theaters are on pace to sell the fewest tickets per capita of any year since before the 1920s.

If it were just a matter of disappointing ticket sales, that would be bad enough. But other important metrics also paint a picture of an industry in decline.

For one, an ever-smaller share of movies accounts for an ever-larger portion of box office sales. Plus, films make up a shrinking share of sales for most top media companies. Walt Disney (DIS) now earns just 13% of its revenue from movies, down from roughly a quarter in 2005. Viacom (VIAB), which owns Paramount Pictures, gets 22% of its revenue from movies, down from 36% as recently as 2010. That share could decline even further if the company’s talks to offload a 49% stake in Paramount go through.

Meanwhile, sales have stagnated over the past three years for 20th Century Fox (FOXA), Columbia Pictures (SNE), and Warner Bros. Pictures (TWX). Smaller players that specialize in film like Lionsgate Films (LGF) and DreamWorks Animation (DWA) have seen their sales slide as well.

All told, forecasters and media outlets are bearish on the industry, saying that 2016 may end up being the worst year ever for movies. Yikes.

WHY IT’S HAPPENING: DRIVERS

Better competition from TV. Back in 1961 when TV programming was considered a “vast wasteland” (in the famous words of FCC Chairman Newton Minow), there was a vast quality gap between television and movies. But that gap has narrowed dramatically in recent decades. Some might even say the gap has reversed.

Additionally, high-end networks now upload an entire season’s worth of shows all at once. Which means that these shows are meant to be binge-watched—and thus are even designed more like movies. In 40 continuous hours, a TV show can boast more complex plotting and deeper subtext than would be possible in any single movie.

More competition from other media. The slate of players vying for people’s attention is constantly expanding. Movies have got mobile apps, video games, and the vast universe of screened entertainment as a whole to contend with. (Video game industry sales overtook box office sales roughly a decade ago. Today, the margin is more than 2 to 1.)

Paid subscription services like Netflix and Hulu have created a whole new world where would-be theatergoers can find the same high-quality entertainment at a low price from the comfort of their bedrooms. Not to mention the countless free options—think YouTube and Snapchat (yes, Snapchat has its own scripted programming)—that provide hours of entertainment for just the price of an Internet connection.

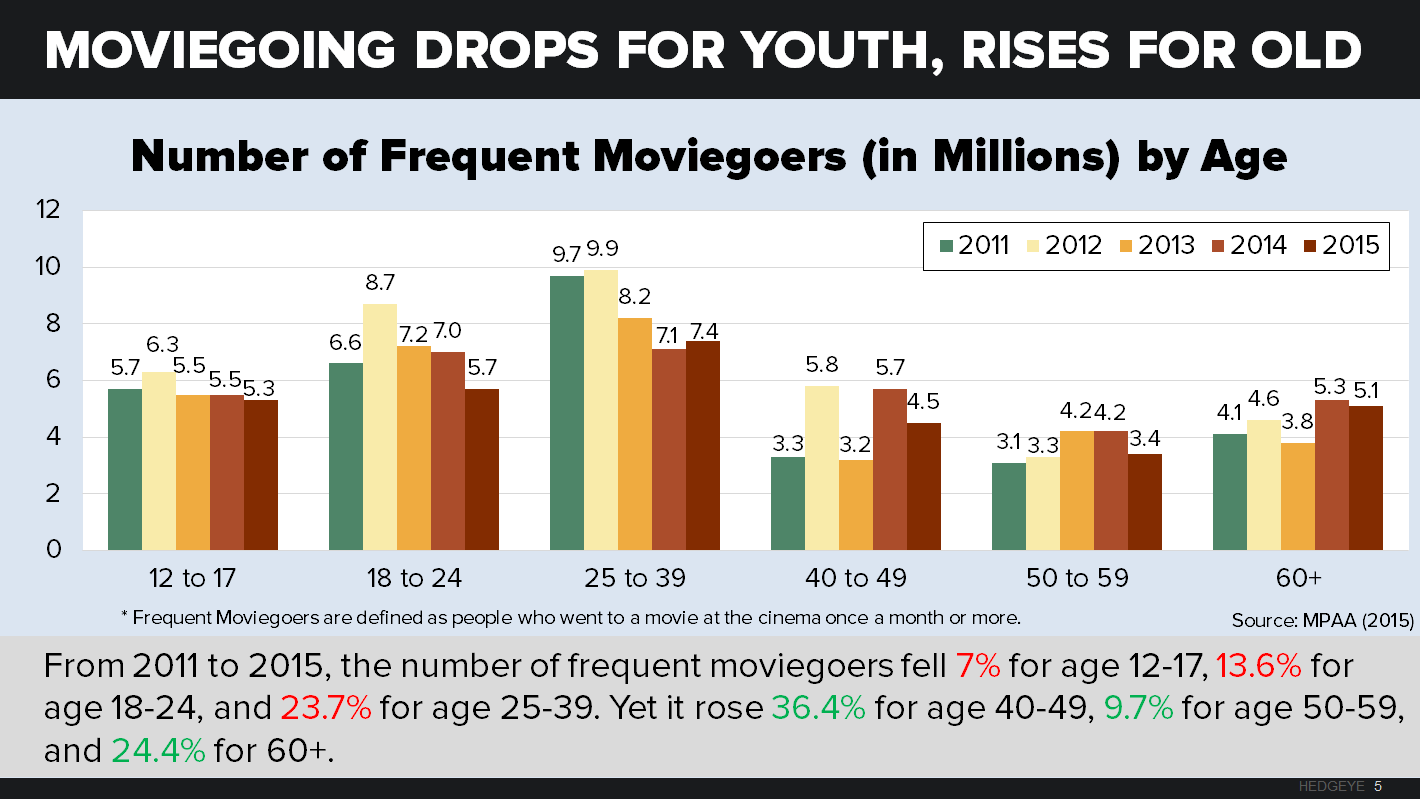

Generational change. Call it the great age divide: Theatergoing has been falling most among younger age brackets. Indeed, over the last few years, more than the entire decline has occurred among the younger age brackets that have historically fueled box office sales. From 2012 to 2015, the total number of “frequent” moviegoers (those who attend once a month or more) decreased among 12- to 17-year-olds, 18- to 24-year-olds, and 25- to 39-year-olds. Attendance among older audiences, meanwhile, is up: Over the same period, the number of frequent moviegoers grew among 50- to 59-year olds and the 60+.

Aftermarket cannibalizing of the box office. Originally, filmmakers used video sales to grab an extra slice of revenue from consumers who weren’t willing to pay to see a movie in theaters. But now, this strategy works against the film industry. Today’s consumers expect to see a movie on store shelves (or in their Netflix queues) within weeks of it leaving theaters. With the exception of the very biggest blockbuster hits, most big-screen releases now register a resounding “meh, I’ll just wait” from consumers. Media expert Todd Juenger sums up this moviemaker dilemma by saying, "People are still watching the same amount of movies that they did a few years ago. They’re just spending $6 billion less a year to do it."

HOW STUDIOS ARE RESPONDING

Going old. Many moviemakers are catering to graying audiences by producing high-quality, thoughtful, and often transgressive films—usually about older people. Boomers have been avid media consumers their entire lives. As they moved into middle age, they fueled a golden age of G-rated cartoons for their kids. Today, these aging film connoisseurs are buying tickets to see grittier, introspective films starring older actors whose characters’ lives are in shambles (à la Youth, featuring Michael Caine). According to GfK MRI, the number of 65+ movie-goers is up 67% since 1995. And you wonder why richly meaningful films that might have been directed by Coppola, Altman, Lumet, or Polanski are still box office draws?

Going young: reboots and sequels. While many Boomers consider remakes uncreative and formulaic, plenty of Millennials don’t mind the lack of originality. Over the past decade, series like Transformers have dominated the top box office spots. And with studios creating fewer, more expensive films (with more explosions than intellectual content), these crowd-pleasers with built-in audiences reduce some of filmmaking’s risks.

But beware: Even sequels are not a guaranteed proposition. Over the past six months, high-profile titles like X-Men: Apocalypse and Allegiant have tanked at the box office.

Going young: whiz-bang technology at the theater. Some film giants are using cutting-edge tech to draw Millennials to the movies. Paramount is reportedly in talks with IMAX to create VR movies. (Care to watch the action from any angle?) Meanwhile, Lions Gate Entertainment and 21st Century Fox have agreed to sell movies via Oculus’s online store.

However, it’s too early to tell whether VR moviemaking is a promising growth strategy or a passing fad. Remember 3-D movies? Plenty once picked that as the “next big thing.”

Going abroad. This may be the safest bet for today’s moviemakers. From 2010 to 2015, the U.S./Canadian share of global box office revenues slid from 33% to 28%. While this may not seem like much of a decline, it leaves China in line to become the largest movie market in the world by 2017.

Walt Disney Pictures is leading the way in overseas markets. The film giant accounts for four of the five highest-grossing films imported to China in 2016. This accomplishment puts Disney on track to be the first Hollywood studio to make $1 billion in one year at the (highly regulated) Chinese box office. Disney even plans to have a branded film in production in China by the end of the year.

Meanwhile, India’s movie audience is also growing at a breakneck pace. In 2015, the top 10 Hollywood releases in India collected about $98 million at the box office—a single-year jump of 34%.

To be sure, even this strategy has its ceiling. High-speed Internet is already beginning to reach these foreign moviegoers. Over time, films will have to compete with the same low-priced, high-quality alternatives that have been hurting the U.S. box office. Netflix is now available in 190 countries worldwide. As the company stocks up on foreign-language movies—and as competitors follow suit—it will mean trouble for the movie industry.

BROADER IMPLICATIONS

Go long on companies that can synergize many media. Once upon a time, a successful movie stood on its own. Today, it is only one avenue by which a branded character or story is delivered to audiences: Along with the movie, there is the book, the song, the videogame, the theme park, the clothing, the toy merchandise, and so on. In the movie industry, the biggest players own the most successful movie franchises. Universal has Harry Potter. Disney has Pixar, Lucasfilm, and Marvel Comics. Warner Bros. has DC Comics. And Lionsgate has The Hunger Games and Divergent series.

Major players like Universal and Disney thus have the edge over smaller players like Columbia and 20th Century Fox that don’t have successful franchises or theme parks. And in a world where standalone films aren’t selling, the biggest losers will be independent filmmakers. Inevitably, these smaller shops will have to transition to TV production and on-line branded entertainment—taking a hit on their market value as they go. And some will be gobbled up, leading to more concentration in the industry. NBCUniversal, for example, plans to acquire DreamWorks Animation by the end of the year.

Expect movie theater operators to be hit hardest. While studios are still able to profit when movies hit pay-per-view, movie theater operators miss out entirely. To stay afloat, many of the larger ones are buying up smaller competitors to enhance economies of scale.

These companies are also doubling down on amenities. Regal has invested in 4DX technology, which gives younger audiences an immersive experience complete with bumps, wind, and fog.

But at this point, there’s probably more money to be made chasing older audiences. Many theater chains are trying to woo Boomers with a deluxe high-margin, high-touch theatergoing experience. In 2014, AMC Theaters announced that it would be spending $600 million to install reclining leather seats in some of its theaters. Others are offering dine-in services for a lavish (hors d’oeuvres and vintage wine) “dinner and a movie” experience.

TAKEAWAYS

- By any measure, the film industry is hurting. Thanks to the massive amount of quality content available to today’s consumers at low (or no) cost, many would-be theatergoers—especially Millennials—are staying home.

- Studios are trying everything to remain viable. But most of their strategies—whether rolling out sequels or searching abroad for profits—have downside risk. Bet on the largest companies to ride the wave of their star franchises and outlast their smaller competitors.