For over a year we have been vocal on how the changing paradigm between Nike and Foot Locker has created a disconnect in FL's real long term (Tail – 3yrs or less) earnings power and the consensus expectations (For detail on the long term call see our February Black Book: CLICK HERE). Yes, we’ve seen some of that playout to date. Mostly in the stock price…off 16% in the past year vs. the XRT -13%, rather than the reported earnings numbers. But we think that starting now, there is a clear disconnect in the intermediate term (Trend – 3 months or more) consensus expectations and what we think are hittable earnings numbers. After 3 years of nearly bulletproof earnings prints (FL has gone 11 straight quarters meeting or exceeding street numbers), FL will see a significant miss or guide down before the books are closed on 2016.

We may not have to wait that long. From where we sit, the current Street expectations for FL’s 2Q16 (to be reported in mid-August) which call for a 3.6% comp to be leveraged into $0.91 in earnings (~10% earnings growth ) look overly optimistic based on the following data points:

1) The May comp was running negative at the time of the 1Q earnings call on 5/20 as management cited a shifted Jordan shoe launch as the cause. Well and good, but we haven’t seen any recovery in online traffic trends since that time which have actually softened since.

2) 2Q comp and merchandise margin compares get tougher sequentially from 1Q when the company missed comp by 160bps and gross margin by 30bps. Editor’s note – our 2% comp assumption implies a sequential acceleration of 40bps on a 2 year average and 10bps on the 3 year. The punchline here is that there are no more easy compares for FL.

3) Any comp miss puts significant pressure on margins as FL needs a low mid-single digit comp to leverage occupancy and about the same to leverage SG&A. The FX SG&A tailwind is now completely gone, and management said clearly on the last call that SG&A leverage in 2Q will be difficult as the company invests in stores and its new corporate HQ.

4) The Nike effect is in full swing. It started in late-May when Foot Locker management was as vocally bearish on Nike as it had been over the last 56 quarters – that’s 14 years. Then Nike reported a meaningful deceleration in it’s Basketball segment two weeks ago after a half decade of outsized growth. That’s meaningful context especially when we consider the fact that FL comps felt the Nike benefit as post-recession results went from -6% to HSD. Now as the Basketball tailwind rolls off, and FL turns more bearish on NKE, we’ve witnessed decelerating comps at FL from 7.8% to 2.9% in 1Q16. With NKE readjusting the price/value equation as evidenced by the KD9, that ASP tailwind that FL has relied upon for so long goes away, but the mall traffic problem still persists. Yet, the street is assuming that FL can re-accelerate growth in the back half of FY16 against tough compares.

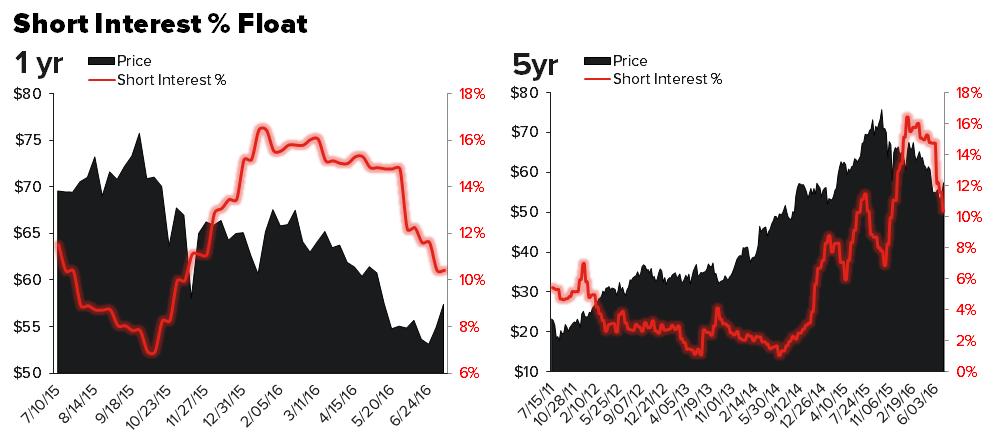

5) The 2Q earnings event is about a month away. FL’s vague “double digit” earnings growth guidance has historically given it the flexibility to reiterate that guidance even on big beats. Should FL miss 2Q expectations, that double digit growth rate looks like it will have to be revised down, unless FL believes it can significantly improve trends in the 2nd half of the year. Short interest has come down from the mid-teens peak earlier this year, and we think this short has plenty of room to run.