Editor's Note: Below is a complimentary excerpt from an institutional research note written by Hedgeye Financials analysts Josh Steiner and Jonathan Casteleyn. If you would like more info on how you can access our research please email sales@hedgeye.com.

While claims moved momentarily higher in early May, they have resumed a breakneck pace lower for now with the most recent week coming in at an impressively low 254k. However, the keyword here is "breakneck." While the labor market remains strong for now, the current level of claims seems unsustainable in the context of history.

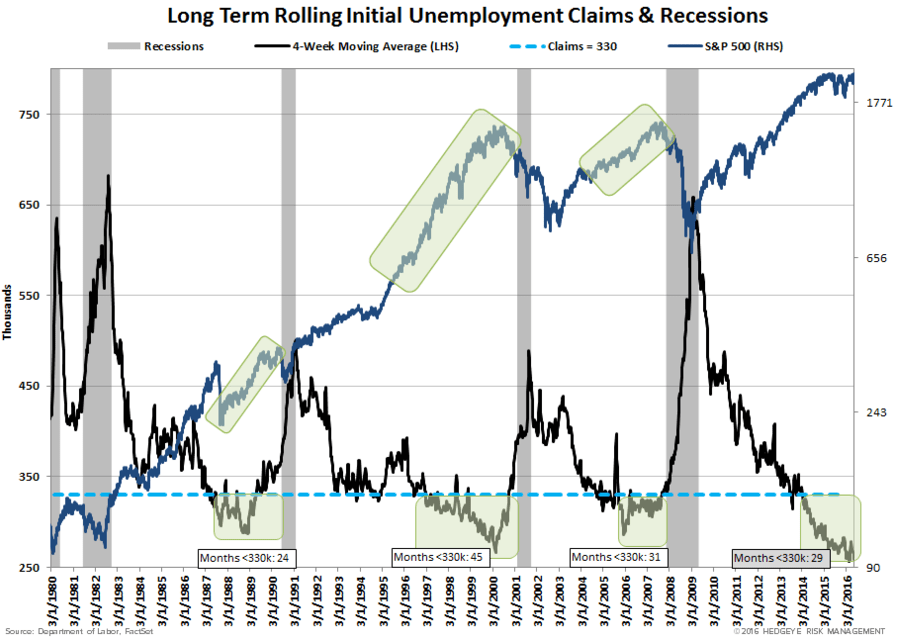

The chart below shows that in the last three cycles claims have dropped below and remained below 330k for 24, 45, and 31 months (average: 33 months) before the economy entered recession in the last three cycles. With the current cycle in its 29th month below that level, we are 5 months past the minimum, 4 months shy of the 33-month average, and 16 months from the max.

With the market at all-time highs and the labor market classically late stage, we remain bearish.

Tick tock.