Below are our analysts’ new updates on our fourteen current high conviction long and short ideas. As a reminder, if nothing material has changed in the past week which would affect a particular idea, our analyst has noted this. We will send Hedgeye CEO Keith McCullough's refreshed levels for our high-conviction Investing Ideas in a seperate email.

IDEAS UPDATES

TIP | TLT | GLD | JNK

To view our analyst's original report on Junk Bonds click here, here for TIPs and here for Gold.

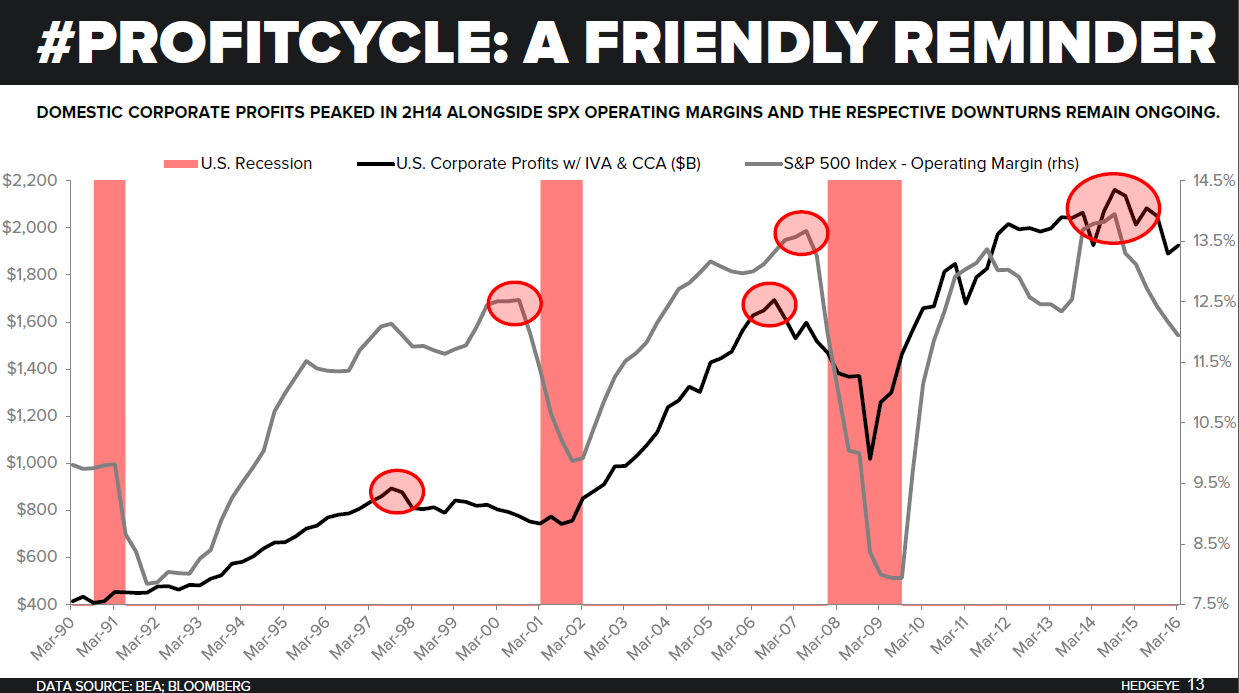

On Thursday, we introduced our Q3 Macro Themes: #ProfitCycle, #ConsumerCredit, #EuropeImploding. The gist of themes #1 and #2 emphasize that the economic cycle continues to roll over as evidenced by declining corporate profitability and the pending deceleration in consumer credit growth which is more of a “when” rather than an “if” scenario.

Consumer credit growth has a direct effect on consumption. Employment and consumption peaked on a Y/Y rate of change basis in Q1 2015 right after corporate profits peaked in the second half of 2014:

After corporate profits and consumption peaks, a decline in consumer credit unfolds as follows:

- If your income is $50K and you take out credit, you can spend $55K.

- The next year credit may get easier and you can spend $57K, and others who weren’t previously able to take out credit can take out credit and spend more than they make too. Spending is spending and it counts as consumption whether it’s with a credit card or cash.

- The scary thing this time around is that the Fed has a smaller policy cushion to lower rates and allow the consumer to lever up more, or at least cushion the deceleration in credit growth that creates deflation risk.

- Eventually profits slow, the labor market deteriorates, and consumer confidence rolls over.

- Financial institutions begin to tighten lending standards to corporations, on the margins, and then eventually the consumer

We expect consumer credit deceleration to be another headwind to consumption in the back half of 2016, which is why it was one of our three themes. As shown in the chart below, the market is sniffing out this marginal change in credit for the credit card lenders. This comes despite the fact that accounts receivables have grown and we’re at a cycle peak in delinquencies and net charge off rates:

All-in-all a corporate profit slowdown is a causal factor of consumer credit contraction which is a self-reinforcing part of a slowing cycle. This has been our call for almost two years now via the long-bond which continues to be an alpha generating “expensive” exposure in 2016. With the move in some commodity leveraged sectors off the February lows (energy), junk bonds (JNK) have had a big run which has eaten into TLT long exposure, but we don’t expect junk bonds to side step a slowing cycle – nothing does. Even so the relative performance is greatly outpacing the broader market.

YTD 2016 scorecard:

- Long Bonds (TLT): +19.1%

- Junk Bonds (JNK): +6.4%

- Relative Performance: +12.7%

And to hit on the potential risk for inflation to pick up in the back half of the year, we’ll us a quote from our update two weeks ago to argue for why we want to stay long of Gold (GLD) and Treasury Inflation-Protected Securities (TIP):

- “We want to be long of continued growth decelerating and inflation picking up from a GIP modeling perspective into the back half of 2016. TIPS are a great way to play both of these views along with our GLD (reflation) and TLT (growth slowing) positions

- The policy response globally will continue to be currency devaluation and monetary easing with the intent to create inflation, and we take their commitment to this very seriously”

DNKN

To view our analyst's original report on Dunkin Brands click here.

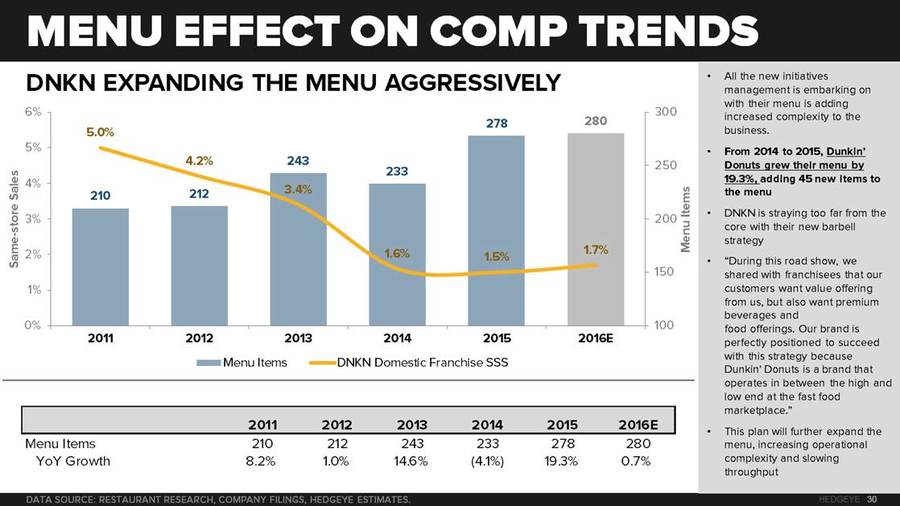

Dunkin Brands (DNKN) has been aggressively adding to their menu as they implement the barbell strategy. With that we have seen a decline in their SSS performance over the last five years. One of DNKN’s core growth initiatives is to own coffee, which means more innovation and more items on the menu. This coupled with their attempt to add more premium items to their food menu will further complicate restaurant operations, slowing the service times.

We believe this will be a core aspect to the decline in SSS over time, which will lead to slowing new unit growth. With the stock up in the last week, we want to reiterate our SHORT call on DNKN and think it still has meaningful downside from here.

WAB

To view our analyst's original report on Wabtec click here.

While the bull story continues to pin its hopes on an acquisition of a French manufacturing company (which we still think will not go through in its current form), Wabtech's (WAB) aftermarket business is continuing to deteriorate as equipment continues to be pulled into storage. Add in weak rail volumes, poor railcar and locomotive orders and we continue to expect 2016 EPS ex-Faiveley below $4/share as the company’s core freight market enters a multi-year downturn.

HBI

To view our analyst's original report on Hanesbrands click here.

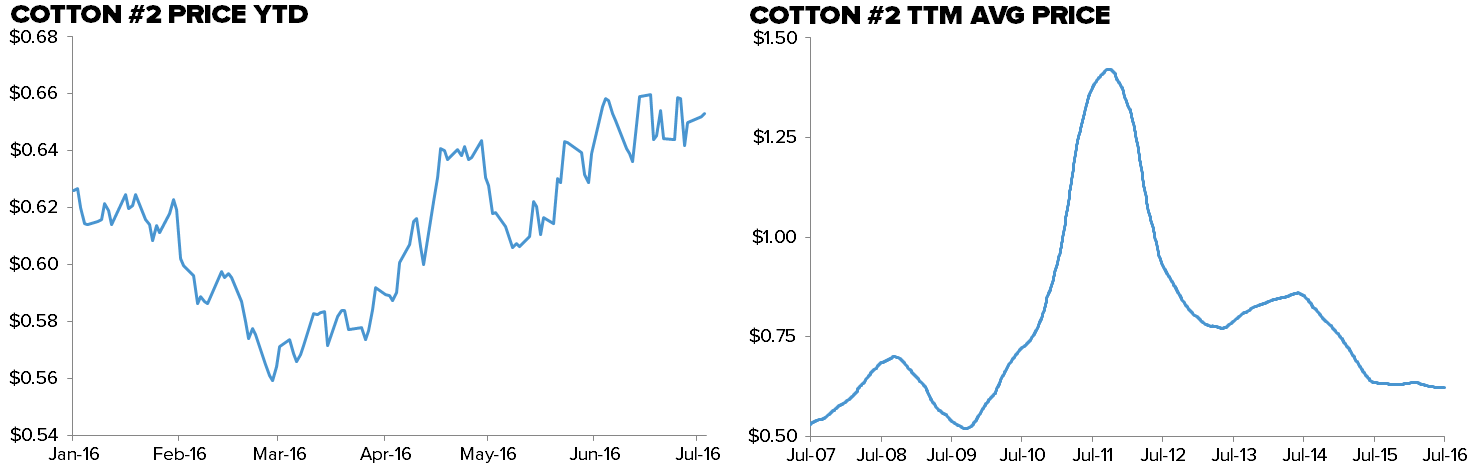

Cotton prices are up 16% from the March bottom. The upward trend in cotton prices since March’s bottom is notable, but the margin implications for the price move over the last 4 months are not very significant. That is, unless we continue to see upward pressure on prices from here. To date we are now back around trailing twelve month levels.

If cotton continues up, it will increase the risk of owning Hanesbrands (HBI) stock. Here’s the rundown on the company’s cotton exposure.

At HBI, cotton makes up 7% of COGS. The company hedges cotton out 6-9 months with the goal of providing time to adjust selling prices as much as possible to accommodate the input cost change. After including hedging and production process, it takes about 4-5 quarters for price fluctuations to flow through to the P&L.

A 10% move in cotton prices is about a 50bps impact to gross margin, or a 4% EPS impact. At the very least, we do not see cotton going down from here so that input cost tailwind has dissipated and HBI has now recognized nearly all of the benefit over the past 5 years when cotton went from $1.40 to $0.63.

MDRX

To view our analyst's original report on Allscripts click here.

MDRX, #EPIC | RIVERVIEW HEALTH

Mery Technology Services (IT division of Mercy Health) announced at the end of June that Riverview Health will implement Epic EHR through Mercy's Epic Community Connect program and hosting platform. Riverview Health uses Allscripts Pro EHR and the old Misys practice management system for approximately 70 docs. Riverview Health also uses Allscripts Payerpath for outpatient EDI/Clearinghouse services and on the inpatient side, they use Quadramed for EHR.

Assuming $2,000 per doc per year in recurring maintenance for legacy Misys, $429/per doc per month for Allscripts Pro EHR and $79 per doc per month for Payerpath, we estimate an annual revenue figure of $0.6 million or bookings value of $2.8 million (5-year contract average).

TIF

To view our analyst's original report on Tiffany click here.

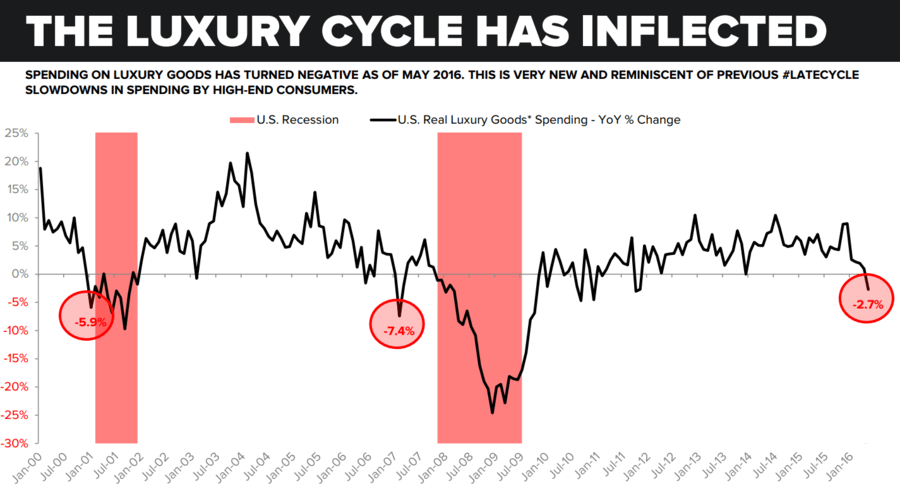

Late cycle, consumer discretionary stocks are an area to avoid. This is particularly true for a name like Tiffany (TIF). The chart below is from our Macro team's 3Q Themes Call showing how luxury spending has turned notably negative. As the consumer slowdown progresses, luxury spending (for example on the fine jewelry that TIF sells) will continue to decline.

TIF has little to no square footage growth, comps running at negative high single digits, and is facing an increasingly weak consumer environment. At the same time, management and street expectations are baking in a back half acceleration in the business. We think TIF will struggle to clear that bar.

LAZ

To view our analyst's original report on Lazard click here.

No update on Lazard (LAZ) this week but Hedgeye Financials analyst Jonathan Casteleyn reiterates his short call.

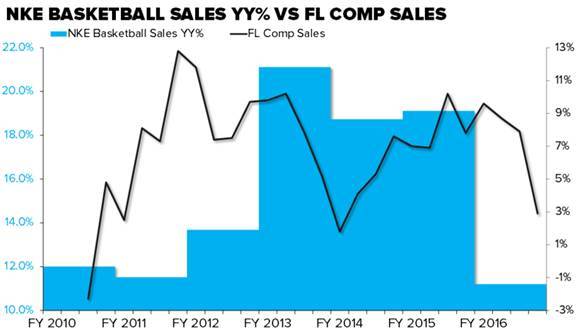

FL

To view our analyst's original report on Foot Locker click here.

From 2009 through the 1st half of 2015, Foot Locker (FL) rode the Nike basketball wave, as category growth went from low double digits to high-teens. FL comps felt the lift coming off the recession hit (and pre-Hicks agenda) going from -6% to HSD. Now, as the Basketball tailwind rolls off and FL turns more bearish on NKE than it has been in 14 years, we saw comps decelerate at FL from 7.8% to 2.9% in 1Q16.

With NKE readjusting the price/value equation as evidenced by the KD9 (which retails at a 17% discount to the $150 KD8), that ASP tailwind that FL has relied upon for so long goes away, but the mall traffic problem still persists. Yet, the street is assuming that FL can re-accelerate growth in the back half of FY16 as compares continue to remain elevated. We don’t think that math adds up.

HOLX | ZBH

To view our analyst's original report on Zimmer Biomet click here and here for Hologic.

Despite a strong headline number, Healthcare employment continues to slow since hitting its peak in August 2015. We believe slowing employment and job openings growth suggest weakening demand for healthcare services such as PAP, HPV and surgical procedures such as Total Knee Replacements. We would also note that Medical Equipment employment also posted the slowest growth since newly insured under the ACA first entered the market, suggesting that demand may be waning.

Veteran Healthcare Sector Head Tom Tobin and analyst Andrew Freedman gave a special preview of their upcoming Healthcare Themes call on HedgeyeTV earlier this week. Don’t miss the key investing callouts and trends in healthcare as well as changes to their Best Ideas list (Tickers include ATHN, ILMN, HOLX, AHS, ZBH, MD, MDRX).

Click The Video below to watch

Click here to access the associated slides.

LMT

To view our analyst's original report on Lockheed Martin click here.

Expect a drumbeat of good news announcements for Lockheed Martin (LMT) prior to its Q2 earnings report on 19 July. This week’s first time appearance of five F35s at the Royal Air Tattoo and Farnborough provide the backdrop for the announcement of the finalization of the contract for ~160 Lot 9 and 10 low rate production F35s to be delivered in 2017 and 18 worth in ~$16B.

Average F35A unit price for Lot 10 will be ~$97M down from $103M on Lot 8 and it is showing good progress toward goal of $85M by 2019. Also expect an announcement of the plan for long term sustainment of the F35 by means of a hybrid contract between the US and a Joint Venture of LMT, BAE, UTX and others. Initial value will exceed $14B between 2018 and 2022 for the fleet of ~500 at that time. Total operating and sustainment costs for the fleet of ~3000 F35s between now and 2070 is estimated at $1 Trillion.

The world political situation is also driving demand for other LMT products, with NATO reaffirming its commitment to have all members achieve defense spending of 2% GDP. If attained this would be an increase of ~ $100B in annual military spending, a potential boon to many defense primes.

This past Thursday, the US and Korea announced the deployment of LMT's Theater High Altitude Air Defense (THAAD) missile defense system to Korea despite previous Chinese objections.