LAZARD SHAREHOLDERS HAVE HAD A ROUGH YEAR. 2016 WASN'T MUCH BETTER.

Market fallout post-Brexit triggered an -11% selloff in Lazard (LAZ) the Friday following the UK referendum. Investors were selling due to its significant European exposure (25% of global advisory revenues) and as concerns mounted about slowing M&A activity industrywide.

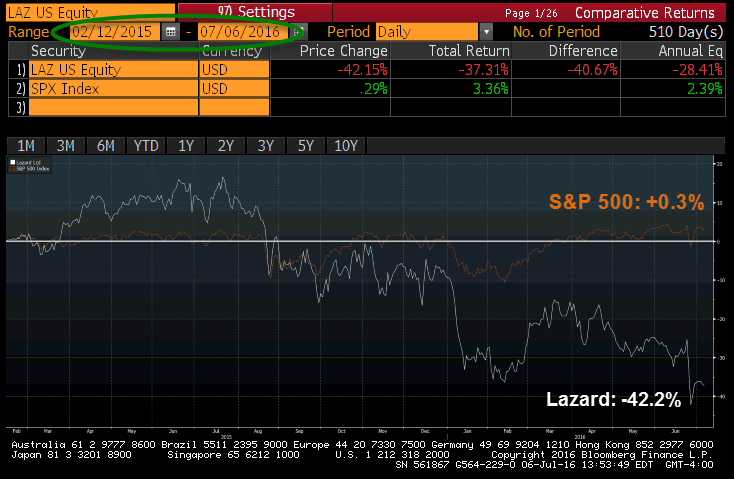

Hedgeye Financials analyst Jonathan Casteleyn first recommended institutional subscribers short LAZ on February 12, 2015. Since then, the stock is down -42% versus +0.3% for the S&P 500.

Casteleyn thinks Lazard has additional downside. During an updated Black Book presentation back in January, Casteleyn reiterated his short call. In it, he outlined unrecognized risks and complacency in this highly cyclical company.

Below are the three key takeaways:

1. M&A Set to Fall

After a new high water mark in global mergers and acquisitions in 2015, the Street is still unrealistic about the opportunity for activity into '16. Estimates are still 20% too high based on "flat to up" activity levels for the New Year which ignore various warnings in the data. Our research shows with corporate funding costs on the rise, that every 100 bps rise in credit costs has historically impacted M&A activity by -20%. Thus the backup in credit spreads that started in 1Q15 all but guarantees a negative comp for mergers in '16. In addition, rising private equity percentages in global announcements and also record highs in consideration values signal an exhausted M&A marketplace.

2. Restructuring Won't Bail Them Out

Complacency is also being sourced by "hopeful" insulation that the firm's restructuring business can plug any gap as the revenue opportunity in M&A slows. Historically, the restructuring business has had a 2 year lag after M&A peaks before contributing to results but restructuring cycles have just half the duration of M&A cycles and never fully cover the lost revenue. At just 15% of total advisory revenues across cycle, restructuring is a mild insulation at best.

3. EM/Non U.S. Asset Mgmt Exposure

The firm's most profitable business, asset management, has unfavorable Emerging Market exposure and total non-US exposure sits at over 50% of AUM. The ongoing elevated levels of the U.S. dollar and investments in petro-oriented economies has historically weighed on demand for institutional exposure to non-developed domiciles. We will flesh out what a reasonable yield on Lazard's AUM business is.

For more information on Jonathan's Casteleyn's research email sales@hedgeye.com