We're sticking with what's worked all year.

As Hedgeye CEO Keith McCullough writes in a note sent to subscribers earlier this morning:

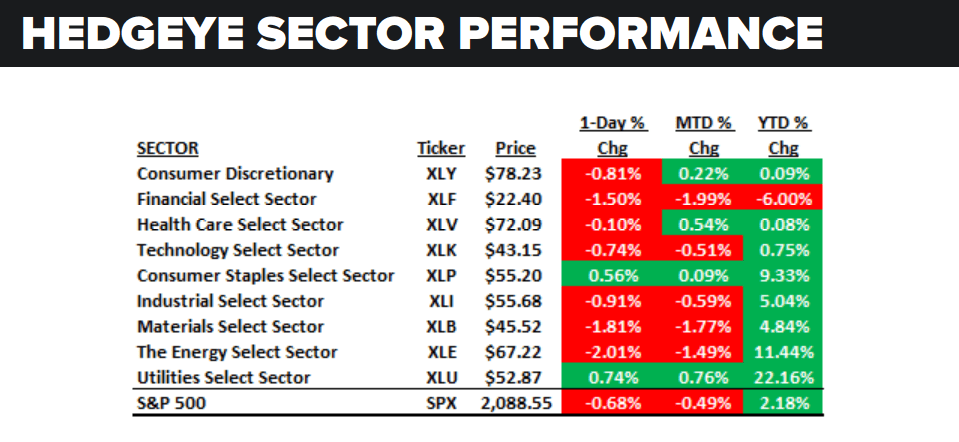

"Our Q3 Macro Themes Call is tomorrow and I’m staying long “expensive” (Utes, XLU +22.1% YTD) vs. short “cheap” (using the wrong bond yields, spreads, etc.) Financials (XLF -6% YTD); interesting immediate-term TRADE break-down signal in Basic Materials (XLB) yesterday – we’ll see if there’s follow through on deflating the “reflation.”

In the video below, Hedgeye CEO Keith McCullough explains why we like "expensive" Utilities: