Even Before Brexit, Global Growth Was Decelerating.

Editor's Note: In this complimentary edition of About Everything, Hedgeye Demography Sector Head Neil Howe discusses lackluster global growth and the IMF's continually downgraded GDP forecasts.

WHAT’S HAPPENING?

Shortly before the Brexit vote, the International Monetary Fund (IMF) warned that a British exit could cut U.K. GDP growth by 0.8 to 3.0% in 2017. In the following year, 2018, it projected that Brexit would cut rest-of-EU GDP by 0.2 to 0.5% and rest-of-world GDP by 0.0 to 0.2%.

No news there: Few imagined that Brexit would be a stimulant. What’s less widely known is that the global economy was slowing down well before it entered the Brexit sand trap.

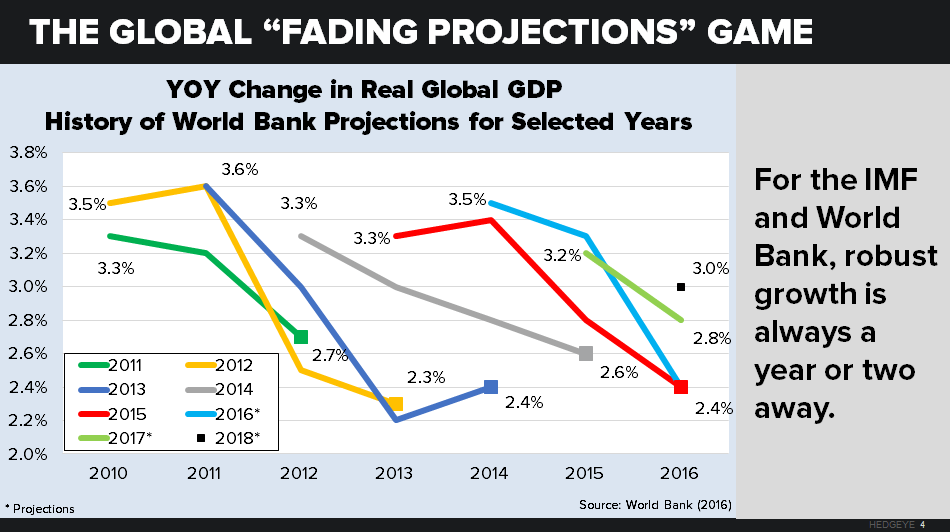

According to the IMF, GDP growth shrank from 5.0% in 2010 to 3.1% last year. The World Bank reports that global GDP growth fell from 3.8% in 2010 to 2.4% last year. The brief re-acceleration in 2014 kindled momentary optimism and then disappeared. Emerging markets and developing economies (EMDEs) have fared the worst, with growth sliding almost every year, while advanced economies have been zig-zagging well below 2% growth for years now. (The IMF and World Bank global growth rates don’t match due to the different ways they weight national GDPs.)

Current-year forecasts are marred by negative surprises. The latest IMF projection pegs global growth in 2016 at 3.2%—down from an earlier 2016 projection of 3.4% in January and 3.8% last year. The World Bank’s 2016 projection of 2.4% has likewise shriveled— from 3.2% in January and 3.5% last year.

If this strikes you like a quarterly earnings forecast (where the quarter gets uglier the closer it gets), you’re on to something.

In fact, over the past decade, these highly compensated, D.C.-based bureaucrats have consistently chosen to revise their predictions downward. Back in 2010, when the IMF took its first stab at growth figures for 2015, the estimate (+4.6 percent) came in at nearly double the final figure.

This pattern means that, as disappointing as the 2016 projection looks today, the final number will probably come in even lower.

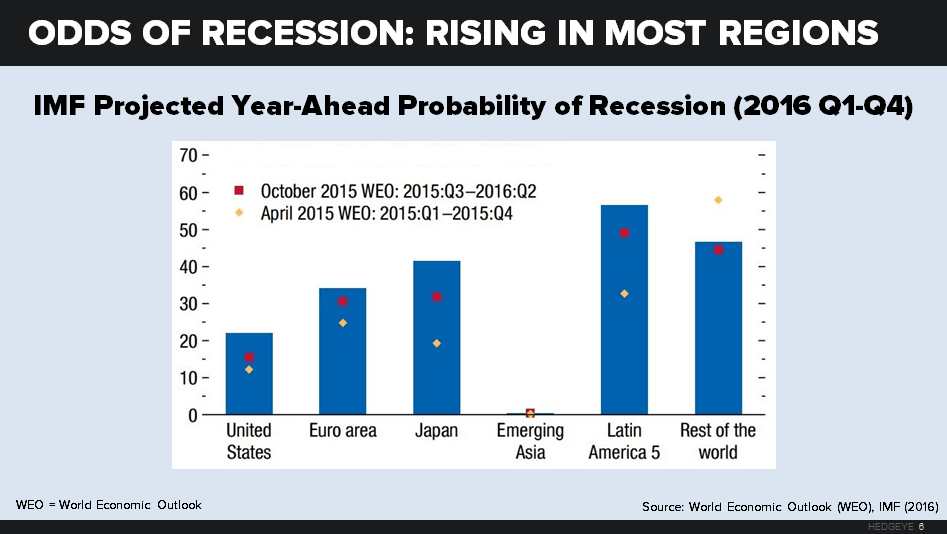

Not surprisingly, the IMF year-ahead odds of recession have been rising since April of 2015 in nearly every region except Emerging Asia (where it remains zero). Since Latin America is already in a recession, that one is an easy call.

If you don’t trust national accounting and prefer to look at the activity reported by firms, the picture you get is pretty much the same. Take a look at Markit’s Global PMIs: You see a dip in 2012, a peak in 2014, and decline thereafter. Indeed, Global Manufacturing now teeters on the edge of contraction.

THE DEVELOPED WORLD: JUST TREADING WATER

The high-income economies haven’t exactly surged over the past five years—but they haven’t done too badly, either. Back in 2012 and 2013, both the Eurozone and Japan were moving in and out of recession. Today, at least for now, they’re out. According to the World Bank, GDP growth in these regions did pick up in 2014, rising from 1.3% to 1.8% (about where it was last year). Real import growth and real investment growth have been trending up since 2012.

Labor conditions are also improving in most advanced economies—most notably the United States. According to the most recent BLS Employment Situation Summary, the U.S. unemployment rate took its first big step downward in months, hitting 4.7% in May.

Other indicators are less encouraging. The IMF reports that headline inflation in advanced economies averaged just 0.3% in 2015, the lowest level since the recession. Long-term interest rates have been on a downward slide for years. Ten-year bond yields are now well below 2% in the United States and—post-Brexit—heading below zero in Germany and Japan.

Unfavorable demographics has constrained high-income GDP growth in recent years and will constrain it further in the future. According to the U.N. Population Division’s medium growth variant, the working-age populations of Japan and most European nations have already peaked and will decline at gathering speed in the decades to come.

EMERGING MARKETS: A TALE OF DIVERGENCE

While the developed world is speeding up slightly, the EMDEs as a whole is slowing down sharply. Unlike in advanced economies, rates of real import growth and real investment growth have been falling in EMDEs since 2010 and are now approaching recession levels.

Yet the bigger story is the wide divergence of growth trends within the EMDEs.

Commodity-exporting EMDEs. Economies that mainly export stuff (oil, gas, minerals, agricultural products) are doing very poorly as a whole. The World Bank projects that commodity-exporting emerging markets will grow by a miniscule 0.4% this year, down from 3.2% in 2013. That’s by far the fastest deceleration of any group.

Obviously, these economies are getting hammered by falling commodity prices. Energy prices plummeted by more than two-thirds from mid-2014 to early 2016, and raw materials did little better. Sure, they’ve rebounded some this year, but commodities are still trading at bargain-bin prices, much to the dismay of export-dependent emerging markets like Russia, Saudi Arabia, Nigeria, South Africa, Venezuela, Chile, and Brazil.

Part of the problem is China’s “rebalancing” policy—moving the economy away from massive capital outlays and toward consumer spending. This may be good news for China’s emerging middle class, but it’s bad news for the export-dependent and often low-income countries that used to furnish the raw materials for all of China’s buildings, trains, harbors, and dams.

China. The largest of the non-export dependent EMDEs, China is still growing rapidly—just less rapidly than before. The World Bank predicts that the country’s GDP growth rate will shrink from 7.7% in 2013 to 6.3% in 2018.

On top of China’s marked shift in trade philosophy, it’s also facing a “currency crisis” that has many savers looking for an exit ramp. China’s efforts to downsize its industrial capacity, plus efforts to defend its currency, have had a tidal impact on the direction of global capital flows. Emerging market capital inflows have recently turned negative for the first time since 2008.

Other non-export dependent EMDEs. Most other non-exporters, however, are doing better than they were a few years ago. According to the World Bank, the GDP for this group (excluding China) has grown by nearly a full percentage point since 2013.

India’s economy is expanding well over 7% annually, where it’s expected to remain in the near future. Southeast Asia’s largest economies, the ASEAN-5 (Malaysia, Philippines, Indonesia, Thailand, and Vietnam), together are growing more than 4% per year.

Typically, these economies benefit from lower raw material and energy prices. And few of them are hurt by China’s declining import demand: ASEAN, for example, has turned into a net importer of Chinese goods.

TAKEAWAYS

- Even before Brexit, global growth was gearing down. Each year since 2010—aside from a blip in 2014—the world economy’s growth rate has slowed. The IMF and the World Bank, if the past is any guide, will continue to lower their estimates for the coming years as time passes.

- The global slowdown varies widely by region. China and the export-dependent EMDEs are falling fastest. Advanced economies are stable, even rising slightly, while non-export EMDEs (ex China) are speeding up