Below are our analysts’ new updates on our fourteen current high conviction long and short ideas. As a reminder, if nothing material has changed in the past week which would affect a particular idea, our analyst has noted this.

Please note that we removed McDonald's (MCD) from the long side of Investing Ideas. We will send Hedgeye CEO Keith McCullough's refreshed levels for our high-conviction Investing Ideas in a seperate email.

IDEAS UPDATES

TIP | TLT | GLD | JNK

To view our analyst's original report on Junk Bonds click here, here for TIPs and here for Gold.

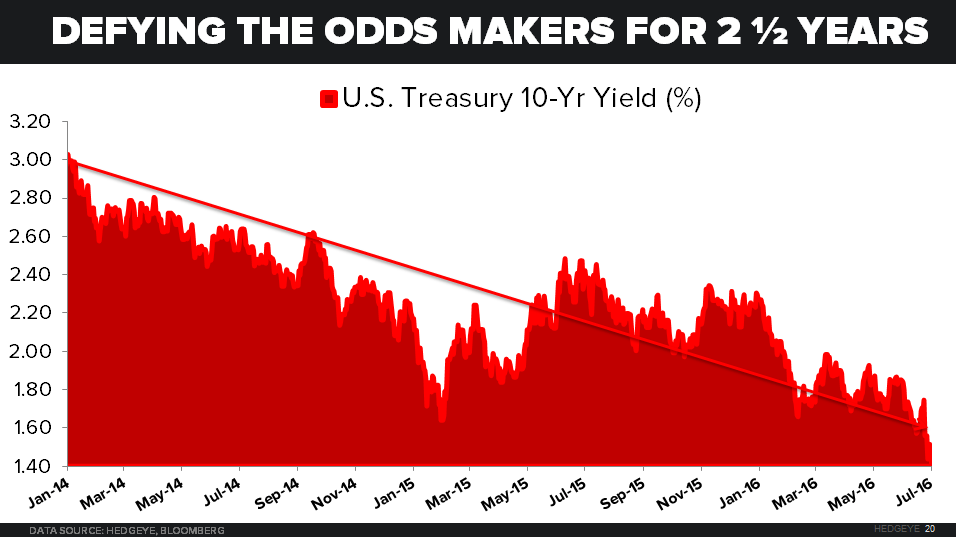

It was another week of all-time lows in long-term Treasury yields and YTD highs in Gold (GLD), Treasury Inflation-Protected Securities (TIP), and Long Bonds (TLT is at a new all-time high!) as the rotation out of volatile equity markets continues. Investors are getting fed-up with the value in their accounts going up and down on a daily basis as evidenced in the fund flows chart at the bottom of the note.

Since equity markets peaked last summer, TLT has been a resilient and less volatile source of absolute alpha, and the good news is that spotting the opportunity requires a daily data grind and a wrestling with reality more than a sky-high IQ:

- S&P 500: +0.1% Y/Y

- TLT: +22.0% Y/Y

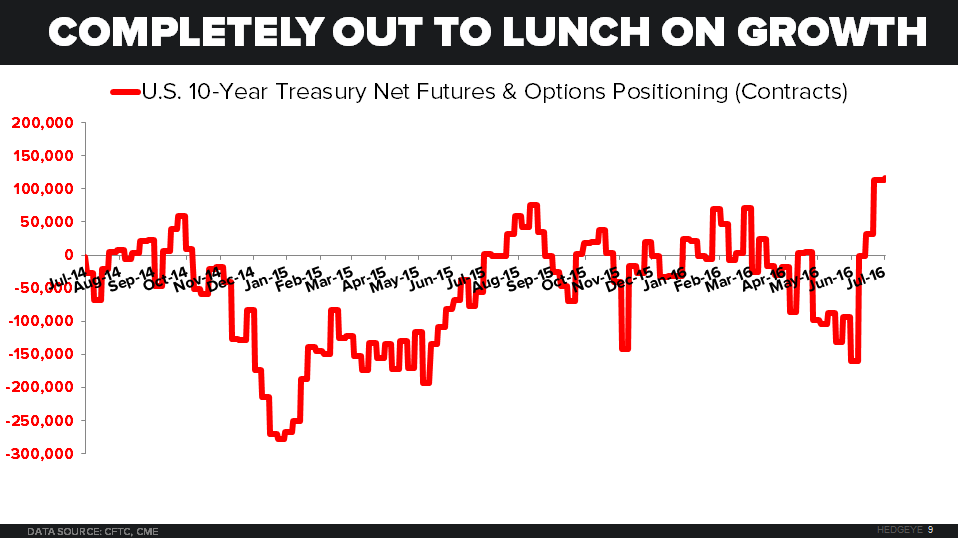

Brexit, Frexit, Yuan devaluation – whatever the story, investors are paying higher premiums for the safety and appreciation potential of the long bond, a source of long-standing outperformance in this #GrowthSlowing environment. Moving into 2015, net futures and options positioning shows that traders had the largest net short position in the 10-year Treasury of the entire cycle, as most were positioned for rate hikes and a “lift-off economy."

A year and a half later, the 10-year yield is crashing to all-time lows. That’s called consensus being out to lunch on growth.

The bottom line is that individual investors are no longer buying the latest bullet market narratives from old Wall Street. In the fund flow chart below which is published by our Financials team, we show the net difference between equity and bond money flow, which has been in negative territory for all of 2016. We agree with these allocation decisions in today’s environment, and we hope some of our subscribers are contributing to this shift and protecting their hard-earned wealth.

DNKN

To view our analyst's original report on Dunkin Brands click here.

No update on Dunkin Brands (DNKN) this week but Hedgeye Restaurants analyst Howard Penney reiterates his short call. Here are the key takeaways on DNKN from our original stock report:

-

Slowing Top Line: Since peaking in 4Q12, Dunkin Brands' 2-year same-store sales trends have slowed by over 350 basis points to 1.7% in 1Q16. Adjusting for the weather benefit in 1Q16, 2-year sales trends are likely flat.

-

Our proprietary Donut Tracker model continues to trend downward, making DNKN’s positive performance in 1Q16 look like a one quarter phenomenon supported by price, and is not indicative of stability or strength.

-

Overcomplicating The Menu Is Bad For Operations: DNKN currently faces an issue many operators have faced => menu overload. The number of Dunkin’ menu items is up over 43% since 2010 and up 19% YoY in 2015.

-

Slowing Unit Growth And Uses of Cash: The slowing sales trends poses a longer-term risk to the company => slowing unit growth. In addition, the further the brand gets from the core markets in New England, the more expensive it is to build stores.

-

Finally, due to the aforementioned slowing trends, the company’s ability to pay out significant amounts of cash to shareholders is also at risk.

WAB

To view our analyst's original report on Wabtec click here.

We got further confirmation of our Wabtech (WAB) short thesis this week. According to the most recent report issued by railroad industry consultancy group Economic Planning Associates:

"Railcar demand 'has weakened significantly in this year’s opening quarter and backlogs have dropped to only 95,038 cars,' according to the most recent report issued by Economic Planning Associates. The smaller backlog represents 5.6 quarters (roughly 17 months, through November 2017) of assemblies at current rates."

Other key callouts from the report:

- “The railroads will shoulder a heavy commodities burden this year,”

- “Coal and petroleum loadings have faltered considerably this year and will be slow in recovery."

- Demand for coal cars “is nonexistent,” EPA said.

We've continued to reiterate our view that weak rail volumes and poor railcar and locomotive orders will weigh on WAB. We continue to expect 2016 EPS ex-Faiveley below $4/share as the company’s core freight market enters a multi-year downturn.

ZBH

To view our analyst's original report on Zimmer Biomet click here.

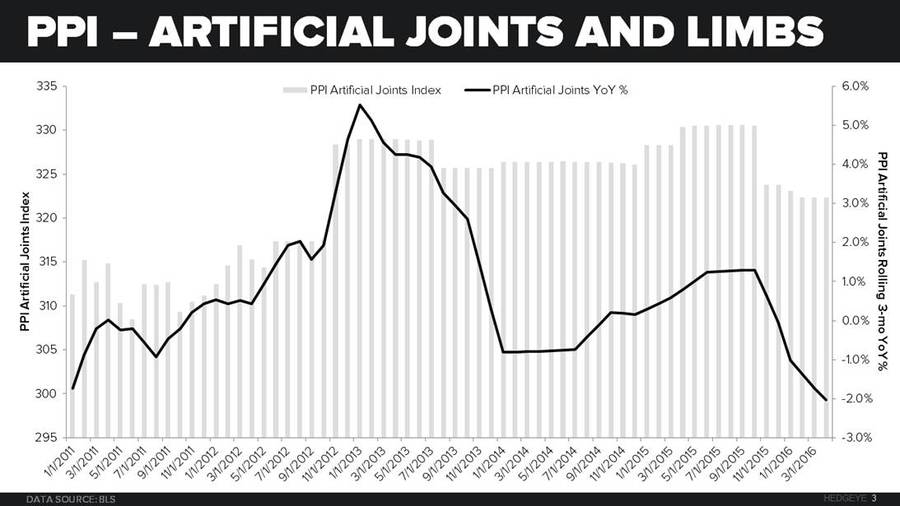

ZBH | Yeah, we could be wrong

Zimmer Biomet (ZBH) has been a frustrating name. On the one hand, we have built out and challenged a longer term negative view of the orthopedic space and ZBH’s role, particulalry now that they have doubled down on the market at a time when pricing and unit volume (in our view) are likely to deteriorate for some time. But a long term view, particulalry when it’s not held by the majority of investors, is a problem when the short term data doesn’t agree. In a battle of narratives, the last data point carry forward is the norm.

So with growth across the US Medical economy coming in stronger in 1Q16 and acclerating on a 2Y basis, despite the ACA tailwind fading, the question to answer now is where are we wrong? On the pricing front, the PPI Artificial Joints is a useful proxy for ZBH, although not perfect. The comparison is tougher sequentially so we’re expecting (our narrative) is that pricing gets worse sequentially and the positive narrative, that pricing is getting less worse and positive, will be a challenge to hold.

As for the broader uptick in consumption, we are in the process of challenging our own #ACATaper view by gathering data to analyze the number of insured persons in the United States, their consumption patterns over multiple years, and test if there is indeed a large upswing in medical consumption many years in the making. We’ll present our findings the week after next, so stay tuned. And if you’ve lost money in ZBH following our short recommendation, we’re not taking it lightly or sitting on our hands waiting for a better outcome.

HBI

To view our analyst's original report on Hanesbrands click here.

This week, Hanesbrands (HBI) closed its acquisition of Champion Europe at a multiple of 10x EBITDA.

One of the reasons we think HBI is paying desperately high multiples for new businesses is that they need to offset the quietly declining core US business. One area we think is underappreciated is the magnitude of the impact that Gildan is having on the low end of the underwear market. NPD reported about 7% share for Gildan Branded (which was just launched in 2013) underwear last year, which jumped to over 8% in Q1. The sentiment was that Gildan branded would take private label share, but if the NPD data is correct, the magnitude of growth implies it must be taking share from national brands like Hanes as well, which puts further pressure on an already depressed organic growth rate.

MDRX

To view our analyst's original report on Allscripts click here. Below is an excerpt from an institutional research note written by our Healthcare team on Allscripts (MDRX).

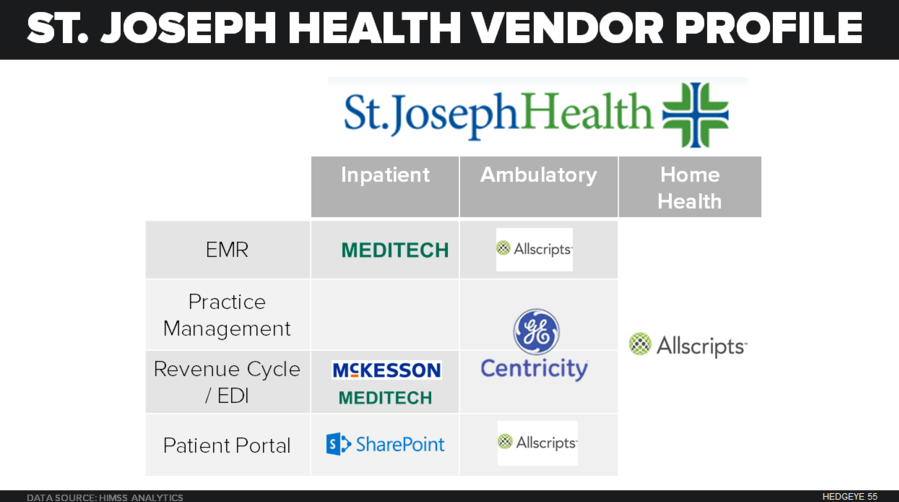

MDRX, #EPIC | MERGER RISK | PROVIDENCE HEALTH AND ST. JOSEPH HEALTH

Takeaway: Another ambulatory loss likely for Allscripts and Sunrise risk in 3 Hospitals.

overview

Providence Health & Services (PHS) and St. Joseph Health (STJSH) signed a letter of intent to merge in July 2015, and recently received regulatory approval from the California Attorney General's office. The combined organization will have 44 hospitals (29 PHS / 14 STJSH) and over 5,000 employed physicians (~4,000 PHS / ~1,500 STJSH). St. Joseph Health leverages a 'best of breed' IT strategy with exposure to 106 products from 75 different vendors.

STJSH's primary EHR vendors are MEDITECH for inpatient, Allscripts Pro in ambulatory and GE Centricity for practice management. STJSH also uses Allscript's FollowMyHealth patient portal in their medical group, as well as Hoag Health's medical group where they have an affiliation.

We believe these vendors are at risk for replacement as PHS is the larger organization in the merger and uses Epic as their primary inpatient and ambulatory EHR.

allscripts loss likely

For Allscripts, this translates into approximately $4.4 million in annual revenue at risk based on $429 per doc per month pricing for Pro EHR and $69 per doc per month pricing for FollowMyHealth. Assuming 5-year contracts, this equals a bookings value of $22 million.

However, the risk for Allscripts extends beyond St. Joseph Health as Hoag Health will likely feel pressure to make the switch to Epic as a result of a 2013 affiliation to form an integrated care network with St. Joseph. Hoag Health currently uses Allscripts Sunrise EHR for their 3 hospitals (571 beds) and 104 employed physicians, which we estimate represents $3-6 million in recurring maintenance revenue to Allscripts.

TIF

To view our analyst's original report on Tiffany click here.

Last week's Brexit announcement will likely have very negative implications for Tiffany (TIF).

- In the near term the resulting drops in the Euro and the pound will reduce reported revenue as Europe makes up ~11% of sales.

- Tiffany has been hurt by weak tourist traffic in the US over the last year and a half, while about 20% of US sales come from tourists. Expectations had been for this to be at or near a bottom with relatively stabile FX rates, but the strengthening dollar after the Brexit vote should only exacerbate the tourism issues.

Overall we continue to see global consumer demand slowing which means Tiffany earnings should continue to underperform expectations.

LAZ

To view our analyst's original report on Lazard click here.

While risk assets for the week recovered slightly after the unexpected shock of the British exit from the EU last week, some stories are starting to greatly lag the broader indices. Lazard (LAZ) is working on a downright awful earnings print for the second quarter and we think entering the seasonally slow summer months will also forgo any hope of a rebound for third quarter numbers.

Furthermore, we are operating on a $2.57 per share earnings estimate for 2017, -30% below the Street and we think the firm has no chance of comping higher year-over-year until 1Q 2017. With the Street still offsides on estimates and a 2016 that can only be salvaged by a rebound in 4Q, we remain Sell rated on shares of LAZ. Our fair value range continues at $22-26 per share.

FL

To view our analyst's original report on Foot Locker click here.

Nike reported its fiscal 4th quarter 2016 this week and results were poor.

Sales missed. Nike confirmed price pressure with basketball that retailers raised last month. Futures slowed sequentially, and missed expectations in every region. Gross Margins were uncharacteristically weak. Inventories were quite weak – eroding sequentially by 500bps relative to sales. SG&A remains elevated (Olympics). And guidance suggests an acceleration throughout the year – but isn’t that a stretch w/Brexit and 23% of Nike’s sales in Europe?

How does this translate to Foot Locker (FL)?

There’s no way FL comes out of this smelling better than it does today. Sales should weaken, gross margins should decline (remember 20%+ Europe exposure), SG&A and capex will BOTH head higher as FL tries to build up a more successful e-comm business. Management is good at FL, and it will spend where it needs to – and after its Nike business went from 50% to 73% of revs over six years it really did not have to invest at all (hence unsustainably low SG&A). Now that changes.

HOLX

To view our analyst's original report on Hologic click here.

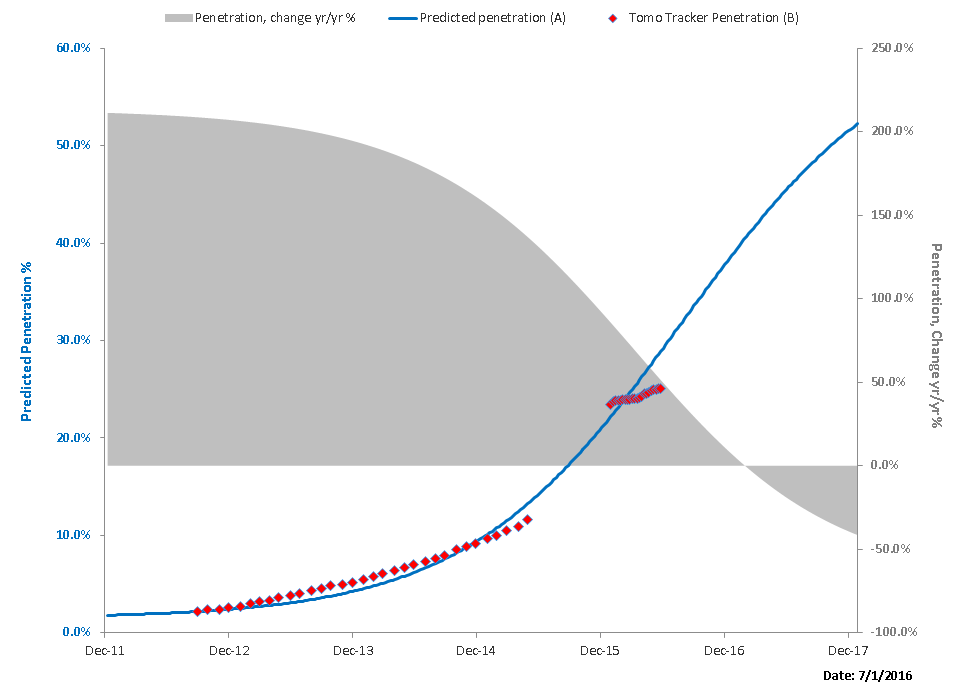

HOLX | MQSA shows the market is where Hologic was 9 months ago.

Takeaway: MQSA DBT facilities up 63 m/m while HOLX gains 21.

MQSA VS TOMO TRACKER

MQSA added DBT facility and unit counts at the end of May. With the update this morning for June, we can see that the market added 107 new units and 63 new facilities month over month. This compares to just 21 new facilities in our Tomo Tracker. We believe this means that market share was less robust month over month than the stated market share of ~60% that management has quoted in the past. The DBT units per facility were flat at 1.38 per facility, below the 1.47 for FFDM broadly (3D is a subset of FFDM). This implies facilities have yet to convert 100% of their 2D gantries, but that further upside is limited.

The market is 28.7% penetrated, exactly where Hologic (HOLX) was 9 months ago when the company last reported 3D unit number of 2,400. We think it is reasonable that Hologic has penetrated their market share to a greater degree than the DBT adoption reported by MQSA this morning. This would imply that growth will begin to decline sequentially from here and turn negative on a year over year basis late 4Q16/1Q17.

TOMO ADOPTION CHART

As the variance between actual and predicted penetration for HOLX 3D facilities widens, the implication for our below consensus 2017 Breast Health estimate is that we will need to reduce our estimate for 3D palcements and revenue, something we will address prior to the company's 3Q16 earnings release. Estimates have come in dramatically since the last earnings release, but management has been strenuous with their description of a market that has continued "runway" for growth, setting up a reasonable opportuninty for negative revision in the near term should our view play out.

LMT

Click here to read our original report on Lockheed Martin.