Editor's Note: Below is a brief excerpt and chart from today's Early Look written by Hedgeye CEO Keith McCullough. Click here to learn more.

"... I get it. Instead of truly trying to understand how we got to now (causal factor analysis across durations), what establishment media needs to do is hurry up some headlines on how they get ad revs up tomorrow.

Progress?

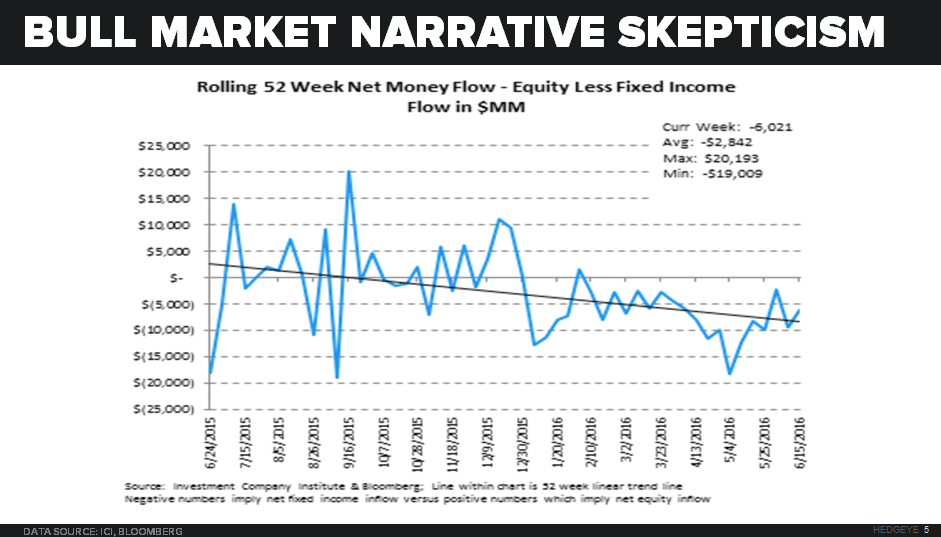

Nah. This is Wall Street. And while we think we can get away with more and more and more of this behavior, The People are telling us (see equity fund outflows, fee compression, redemptions, etc. for details) that they don’t trust us anymore."