“It only adds. I don’t understand how it subtracts.”

-Richard Feynman

I’ve spent all of this week up at the lake house in my homeland with my growing family. This is a place that is free of Wall Street’s noise. There are no Washington politics here. There are no central-market-planners either. It’s a place where I can breathe and think.

Like yours, my story on how I got to now is different. We are all different. If you study where everyone around you came from, you’ll quickly realize that our collective experiences only add to life’s lessons. They do no subtract.

How we all got to now is also the title of a book I’ve been reading this week. Steven Johnson is the author. He also wrote a great thought leader’s book called Where Good Ideas Come From.

After the biggest 1-day loss of Global Equity market cap in world history (Friday June 24th, 2016), I sincerely hope many of you were proactively positioned with not only good ideas, but great ones.

If you weren’t, I think you’ve been given one of life’s most progressive opportunities – the opportunity to learn, evolve, and improve. How We Got To Now is called history. It’s neither yours, nor mine. It’s ours – something we’ll spend a lifetime trying to understand.

Back to the Global Macro Grind…

And the bounce… in US Equities, that is… a two-day +3.5% S&P 500 v-bottom (on decelerating volume) into the beloved compensation period that is both Wall Street month and quarter end.

Although cash comp isn’t what it used to be (and how we got to now in 2016 will have a record number of macro narratives on why) … the most basic and truthful one is that in the last 6-12 months, both the economic and profit cycle slowed.

If you’ve had that right, you wouldn’t have had to blame anything. Your accounts are happy.

If, however, you’re looking for the latest perma bull marketing case for being long “stocks” instead of what’s been really getting people paid (Long Bond, Municipal Bonds, Utilities, Gold, etc.), here’s yesterday’s consensus headlines:

- “Oversold Conditions” – true (SPX 1998 is the low-end of our current 1 immediate-term risk range)

- “Brexit Backtracking” – uh, ok… are they going to re-vote or something?

- “Pension Fund Rebal” – sure, I don’t doubt there’s always a “buy program” somewhere

- “Lehman Moment Skepticism” – lol, is that what the bull case was all along?

- “Fed On Hold” – now we’re talking! Based on all growth and profit cycle forecasts being wrong, of course

- “Fiscal Stimulus Hopes” – oh, yeah – now we’re really talking – time for some bridges and roads, baby!

Not one of these headlines has anything to do with real economic or profit cycle growth accelerating. They all have to do with either the risks that a complacent consensus didn’t forecast, or what “the worst case” isn’t (and how government can make it all better again).

I get it. Instead of truly trying to understand how we got to now (causal factor analysis across durations), what establishment media needs to do is hurry up some headlines on how they get ad revs up tomorrow.

Progress?

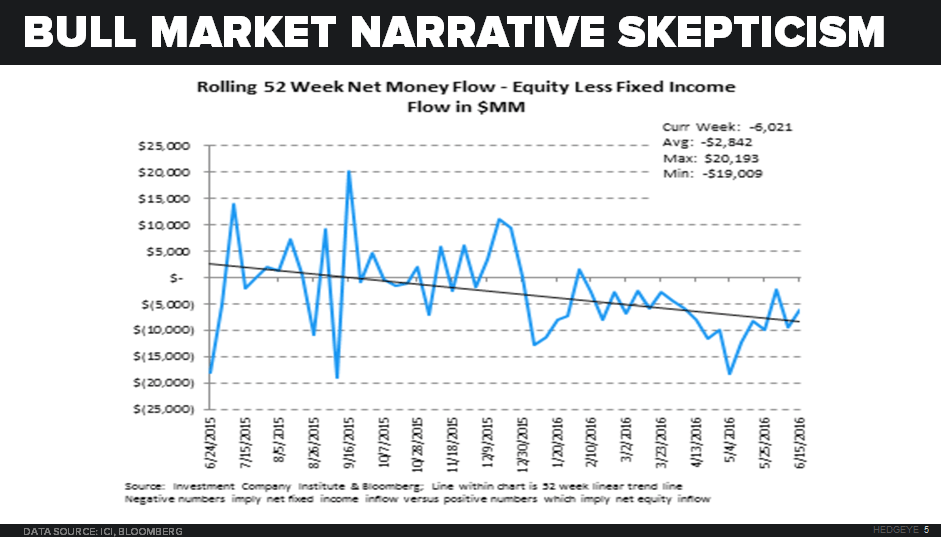

Nah. This is Wall Street. And while we think we can get away with more and more and more of this behavior, The People are telling us (see equity fund outflows, fee compression, redemptions, etc. for details) that they don’t trust us anymore.

Should they?

With serious change in our collective behavior, I think they could. In fact, I think this might be the greatest growth opportunity that our profession has ever seen. But wow are we going to have to change both how we got to now before we have a chance to get there.

Ex-Energy, Ex-China, Ex-Brexit, the latest rate of change surprise in the US economy (next to #LateCycle employment and consumer credit growth slowing) is that US Housing’s gains from the 2015 highs are slowing.

In yesterday’s Pending US Home Sales report for the month of May, we saw signed contracts slow -4.7% month-over-month to negative (-0.2% year-over-year) for the 1st time in two years.

Since US Housing (and Autos) didn’t peak (in rate of change terms) until October of 2015, big ticket consumption is at risk of slowing from now until the US Election. Unless, of course, what happened to people’s net worth in June magically stimulates confidence…

If we want a confident population, we need to stop trying to centrally-plan stock market volatility and let The People’s hard earned currency become the strongest in the world. We need to stop lying to them about economic reality too.

From a realistic set of expectations, most humans can start to believe in how they can get to tomorrow. Trust is earned, not allocated. How most great families, companies, and countries got to now understand that. It only adds to progress.

Our immediate-term Global Macro Risk Ranges are now (with intermediate-term TREND Research Views in brackets):

UST 10yr Yield 1.40-1.60% (bearish)

SPX 1 (bearish)

RUT 1087-1142 (bearish)

NASDAQ 4 (bearish)

Nikkei 140 (bearish)

DAX 9106-9758 (bearish)

VIX 15.19-25.84 (bullish)

USD 94.73-97.01 (bullish)

EUR/USD 1.09-1.12 (bearish)

YEN 101.10-105.38 (bullish)

Oil (WTI) 46.66-51.21 (bullish)

Nat Gas 2.56-2.91 (bullish)

Gold 1 (bullish)

Copper 2.05-2.20 (bearish)

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer