As we've been noting in the past few days, the market is not assigning a more than 50% probability of a Fed rate hike until the beginning of 2018.

That's right... a year and a half from now.

Meanwhile, rate CUT expectations have spiked and the market marches higher. Here's analysis from Hedgeye CEO Keith McCullough in a note sent to subscribers earlier this morning:

"Watching the Old Wall (and it’s media) shift to “Fed on Hold, buy stocks” is funny – but a friendly reminder that this is not funny if you are a bank; 1.44% 10yr Yield minus 0.62% 2yr = fresh YTD low (and low for #TheCycle) as trending US employment growth continues to slow ex-Brexit."

https://twitter.com/KeithMcCullough/status/748118824759730176

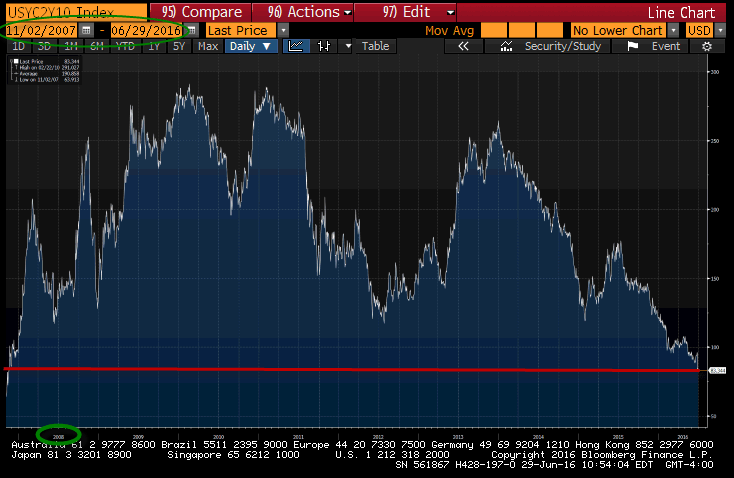

Below is a chart of 10s/2s yield spread. Notice that the last time it was at its current level the U.S. economy was in recession:

In short, the compression of the yield spread means pain for bank net interest margins... which is why bank stocks look like this year-to-date:

Ouch!

Take a look at the U.S. equity market sector scorecard.

Note: Our favorite sector long Utilities (XLU) continues to outperform Financials (XLF) by a wide margin:

https://twitter.com/KeithMcCullough/status/748108431324778496

What to do?

Stick with what's working in 2016. Long Utilities, Short Financials