“Everybody’s out there wrestling like a robot.”

-Hulk Hogan

At $2.08T (T = Trillion, in US Dollars) in losses, Friday June 24th, 2016 will be remembered by objective market historians as the biggest down day ever (surpassing SEP 29, 2008), in terms of Global Equity value lost. By our scorecard, ever is a long time.

Oh, but is that “inflation adjusted, Keith?” Seriously, we’re half-way through 2016 and we’ve not only had the biggest loss in global “stocks” (on a one day basis) ever, but in the USA we had the worst 6-week start to the year, ever. Evers are adding up.

Yes, pre and post both “China” and “Brexit” (no the 34k NFP jobs print last month didn’t have to do with either), #GrowthSlowing has proven to be causal. With consensus still wrestling with equity “valuations”, we’re the only independent research firm on Wall St. whose favorite asset allocations remains the Long Bond, Gold, and Safe Yield Stocks that look like bonds (Utilities).

Back to the Global Macro Grind…

What changes this morning? Not a whole heck of a lot. While I’m assuming they’ll try to bounce US Equity Beta into month and quarter end (Thursday), the 2016 game clock continues to tick with some immediate-term catalysts:

- US corporates levering up to buy back stock on no volume up days, are now in their “black-out” period (EPS Season)

- Pre-announcement Season = ON. And we continue to think Q2 US Corporate Profits will be the worst yet

- Financials (XLF) report first and with US long-term yields at all-time lows, guidance is going to be nasty

Yep, instead of calling Earnings Season “Ex-Energy”, you’re going to have to be all about being long Energy (with the US Dollar back to +0.5% year-over-year) and “backing out the Financials”… if you want to be an “earnings have bottomed” bull.

Say what? The US Dollar isn’t getting smashed by the Fed anymore? Nope, thanks to the UK reminding the world that a devalued currency is a bad thing, the US Dollar Index rally was part of the following macro FX matrix last week:

- US Dollar Index +1.5% to -3.1% YTD

- Euro vs. USD -1.4% to +2.3% YTD

- Yen (vs. USD) +1.7% to +17.4% YTD

- Pound (vs. USD) -4.7% to -7.1% YTD

- Gold +2.0% to +24.3% YTD

Gold is a currency? Yes. While it has “no yield”, neither does the British Pound. Gold competes with both real interest rates and central bankers trying to devalue currencies around the world. Since it has no yield, it loves playing against “negative yields.”

Btw, who in their right mind would want to be long the Euro vs. Gold, from here?

Friday was one of the best absolute and relative performance days in my 17 year career. While I am genuinely humbled by that (it was a research team effort, not just me), I’m not considering Hedgeye’s position consensus, yet.

Most of what happened on Friday had been in motion, in rate of change terms, since AUG-SEP 2015. Our call on US long-term yields going to all-time lows, didn’t happen in a 1-day vacuum.

This morning’s follow through in being long duration and/or low-beta stocks with a “safe” yield looks like this:

- UST 10yr Yield down another 10 basis points to a fresh YTD low of 1.47%

- UK 10yr Yield down another 13 basis point to a fresh all-time low of 0.96%

- Swiss and German 10s testing all-time lows at -0.61% and -0.12%, respectively

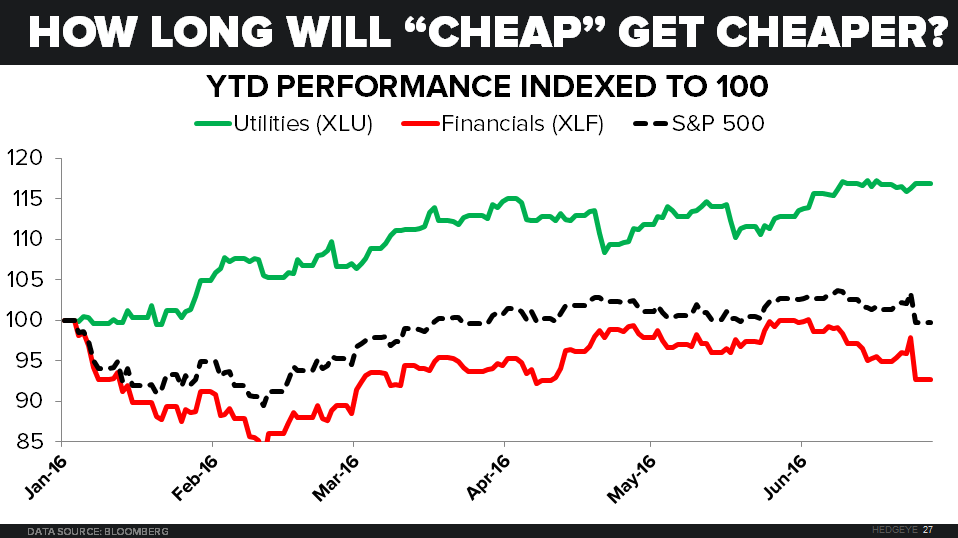

If all you do is US Equities, did someone say underweight (short) the Financials vs. Utilities in 2016?

- Financials (XLF) hammered on Friday, losing another -5.4% to down -7.3% YTD

- Utilities (XLU) did their job for our clients, closing +0.6% on a very red day for Equity Beta at +16.9% YTD

While US Equity Beta and Small Caps had “nice charts” at the May and June highs, from a TRENDING US Equity Style Factor perspective, they continue to be shorts on weeks like last week. With the SP500 (beta) down for the 3rd week in a row:

- High Beta Stocks dropped -3.0% on the week to -1.7% YTD

- Low Beta Stocks were almost flat at -0.2% on the week to +9.4% YTD

- Small Cap Stocks were -2.7% on the week to -1.9% YTD

- Large Cap Stocks were -1.8% on the week to +0.1% YTD

*Mean performance of Top Quintile vs. Bottom Quintile, SP500 Companies

While a US Equity perma bull might say something passive aggressive like, “well the market is kind of flat”, that’ll make you beta in 2016, if you’re lucky. Those generating alpha are up +8-15% in 2016. They’re going to take a lot of market share from beta chasers.

One of the “technologically innovative” share gainers at the peak of #TheCycle (2015) were “Robo Advisors.” Unlike a firm like ours, these guys have the efficient-market-robotic-pie-chart-allocation thing down cold… until global equities implode, that is…

Betterment (one of the more marketing savvy Robo Advisors), “suspended trading” on Friday. Personally, I enjoyed seeing that headline. With Total US Equity Volume +65% vs. its 1-month average (on the day), you do not want your hard earned net worth to get that kind of memo. You want a real-time risk manager who isn’t a consensus exposure chasing robot.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.45-1.65%

SPX 2021-2066

RUT 1115-1151

NASDAQ 4

VIX 17.66-26.99

USD 94.08-96.12

EUR/USD 1.09-1.12

Gold 1

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer