“People have a tendency to stay with what they have, at least in part because of loss aversion.”

-Richard Thaler

Don’t go all Brexit on me. You know that there’s a tendency to stay, right? That’s what we #Behavioral Economics people call the Endowment Effect – i.e. that people over value their stuff vs. other people’s stuff (see George Carlin’s “A Place For My Stuff” for the more graphic depiction of why you probably think your stuff is better than other people’s stuff).

As Thaler explains, “while loss aversion is certainly part of the explanation for our findings, there is a related phenomenon: inertia. In physics, an object in a state of rest stays that way, unless something happens. People act the same way: they stick with what they have unless there is some good reason to switch.” (Misbehaving, pg 155)

Are there some good reasons for Brits to exit? Sure. Are there more reasons to stay? Probably. At $1.47 GBP/USD (Pound vs. USD), that’s not my opinion. That’s what’s priced in. The tendency for The People of the UK to stay is already priced into both the Foreign Currency and US stock markets.

Back to the Global Macro Grind…

Oh Muddler, did you have to add that last part? Did you really have to remind me that if I was chasing the spooz at SP again yesterday that I was pricing in what’s already priced into both FX and Equity markets?

It’s not personal, bro. Most of the time, my stuff (multi-duration, multi-factor quantamental process, bro!) is better than the moving monkey stuff. We built Hedgeye on that.

One of the core behavioral risk management screens we’ve built to monitor what is (or is not) priced into consensus is looking at the rate of change in the big bets Institutional Investors are making in macro markets.

Looking at the most recent CFTC futures & options data, here’s what augments what I think is getting priced in:

- SP500 (Index + E-mini) net LONG positioning +117,566 contracts is the biggest net long position of the year

- USD net LONG position of only +4,681 contracts is well under its 3-to-12 month avg of +12,000-to-36,000

- GBP/USD net SHORT position of -33,972 dropped -30,719 from its net short peak last week

In other words, measuring where macro positioning is relative to itself (using 1-year z-scores):

- SP500 net LONG position = +2.63x

- USD net LONG position = -1.81x

- GBP net SHORT position = -0.54x

And this positioning was BEFORE yesterday’s squeeze in both Pounds and the SP500!

I’m not suggesting that neither the SP500 nor the GBP/USD can’t go higher (there’s always a chance!). What I’m telling you is that consensus was already positioning for both to go higher… and they did. #NiceCall

Yes, rate of change matters. As the vote to Remain ramped, so have these bets. Going back to the week prior, the net SHORT position in GBP/USD hit its YTD high at -2.39x on a 1-year z-score.

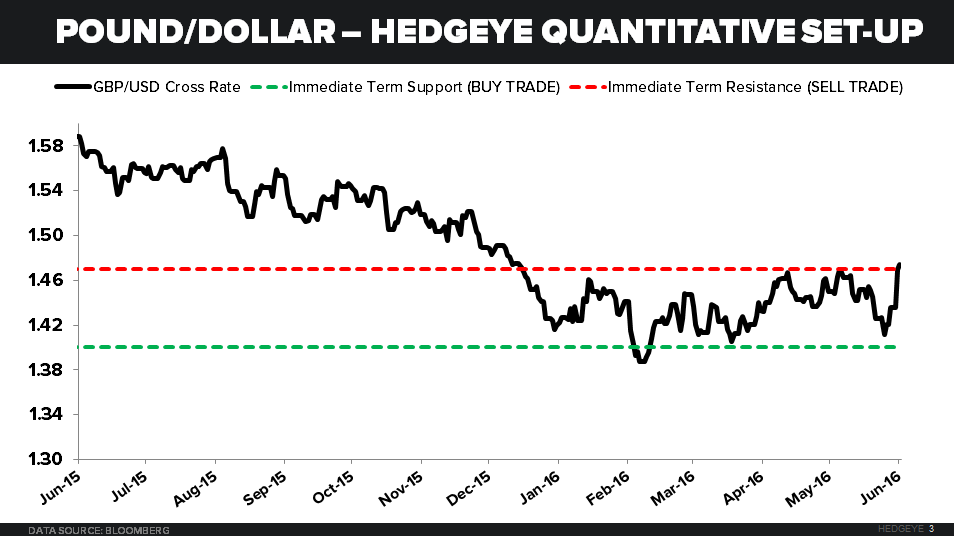

And now, my immediate-term risk range process is implying that the asymmetry (in Pound terms) is to the downside with an immediate-term GBP/USD risk management range of $1.40-1.47.

Sell on the news anyone?

No matter what the decision, on Friday morning we’ll all get to enjoy going back to risk managing what’s going on in the rest of the world’s markets and economies.

On that broader signaling horizon, here are some things Mr. Macro Market is thinking about this morning:

- Dr. Copper being blasted for another -1% #deflation down day (post its “No Brexit” reflation day)

- Spanish Stocks (IBEX) leading the first batch of European stocks to go red (still in crash mode)

- Chinese Stocks (Shanghai Comp) showing no follow through, down another -0.4% overnight

Imagine “no Brexit” wasn’t priced in and it perpetuated a worldwide “bottom” in global demand? Lol. The dude who has been calling for “PMIs to bottom” for a year now will have officially nailed it using the wrong causal factor!

More realistically, what these 3 things might be signaling is that:

- USD is about to make another long-term-higher-low vs. GBP

- European Stocks are about to make another lower-high within their bearish @Hedgeye TRENDS

- Chinese Stocks still suck (-44% from last year’s high), no matter what gets newsy

And my vote on my 11-month old tendency to stay with our local and global #GrowthSlowing call will be to remain.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.54-1.72%

SPX 2056-2095

NASDAQ 4

DAX 91

VIX 16.33-23.12

USD 93.12-95.04

EUR/USD 1.11-1.14

Copper 2.00-2.10

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer