Below are our analysts’ new updates on our fifteen current high conviction long and short ideas. As a reminder, if nothing material has changed in the past week which would affect a particular idea, our analyst has noted this.

Please note that we removed NuSkin (NUS) from the short side of Investing Ideas and added Lockheed Martin Corporation (LMT) to the long side. Hedgeye Potomac Senior Defense Policy Advisor LtGen Emerson "Emo" Gardner USMC Ret. will send out a full report outlining our high-conviction long thesis next week. Please see below Hedgeye CEO Keith McCullough's refreshed levels for our high-conviction Investing Ideas.

LEVELS

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

TLT | GLD | JNK

To view our analyst's original report on Junk Bonds click here and here for Gold.

Did Janet fool you with her hawk costume? As we showed in Wednesday's Chart of the Day before the main-event (the FOMC statement and press conference), Yellen is a labor economist and ALL IS NOT WELL according to her own indicator. Below is the Fed’s Labor Market Conditions Index, which has declined in every month this year to the lowest sequential level since the Great Recession:

Despite hawkish comments from various Fed Heads, it’s only fitting that the proxy for forward looking growth expectations, the 10-year yield, reached a new cycle low on Wednesday after another recessionary Industrial Production print:

If you need more proof that the Central Planning #BeliefSystem is breaking down, long-term Treasuries and Gold front-running a predictably dovish Fed are confirming that breakdown. Gold reached a new YTD high to close out the week. Gold (GLD) is up 22.5% year-to-date versus 1.3% for the S&P 500. Meanwhile, the 10-year Treasury yield hit a new cycle low! Meaning, Long Bonds (TLT) are up 12.5%.

In other words, if you have a tested view on the economic cycle, it’s easy to sit comfortably through the manic messages from central planners.

MCD

To view our analyst's original report on McDonald's click here.

No update on McDonald's (MCD) this week but Hedgeye Restaurants analyst Howard Penney reiterates his long call.

DNKN

To view our analyst's original report on Dunkin Brands click here.

In this brief HedgeyeTV video excerpt, Restaurants analyst Howard Penney laid out the three key reasons to short Dunkin Brands (DNKN) during a Black Book presentation for institutional investors.

Click the Video below to watch

WAB

To view our analyst's original report on Wabtec click here.

While Wabtech (WAB) awaits further news from the regulators on their Faiveley deal, WAB’s aftermarket business continues to weaken. As train speeds pick up, equipment gets pushed off the track. This has a two pronged effect on WAB’s aftermarket business as equipment heads to storage. Less equipment requires maintenance and servicing while the stored equipment can be used for parts.

ZBH

To view our analyst's original report on Zimmer Biomet click here.

The private equity firms KKR, Goldman Sachs and TPG sold shares in Zimmer Biomet (ZBH) this week in a large 11M share offering. The secondary was priced below the previous day’s $118.24. These firms owned 18.6M shares, so the offering reduces their collective exposure to ZBH by more than half.

As insiders, it’s tempting to look at insider private equity sellers and think they “know something,” but that is information we’d prefer to remain in the dark on. While market weakness has many narratives, from Brexit, the Fed, SYF, rising jobless claims, weak employment trends, we’re sticking with the slow-moving #ACATaper and #Deflation themes.

For more Healthcare insights...

Earlier this week, our Healthcare analysts Tom Tobin and Andrew Freedman hosted a live Q&A to discuss their top ideas and the latest trends in the Healthcare space.

Topics included:

- Employment, JOLTS and an #ACATaper Update related to companies like AHS, HCA, HOLX, MD and ZBH

- ATHN Tracker update and latest thoughts

Click the Video below to watch

Click here to access the associated slides.

HBI

To view our analyst's original report on Hanesbrands click here.

This week Hanesbrands (HBI) announced that CEO Rich Noll would be stepping down in October.

Our take:

- This is VERY bad for HBI. The bulls who are stepping up and saying that this is a non-event because HBI has a ‘deep bench’ are in a severe state of denial.

- Rich Noll has ruled HBI with an iron fist since it was spun out of Sara Lee a decade ago. In that regard, you could argue that his successor will be welcomed by the organization. But like the guy or not, Noll’s approach has been extremely effective as it relates to the stock.

- Noll is 58, and his successor is 57. It’s not like the organization is being handed down to a new generation of leadership.

Remember that our call here is based on the following…

- HBI is the leader in a no-growth category

- The company is starting to feel pressure from competition at the high-end (Tommy John, Lululemon, Underarmour, etc…) while getting incrementally squeezed at the low end, as Gildan gets heavier into underwear.

- Margins are beyond peak as factory utilization (something most retail analysts don’t understand) is at a peak of 90%+, and cotton costs are near trough.

- The primary channels where HBI sells its product clearly have too much inventory (WalMart, Target, Macy’s, Kohl’s, JC Penney, etc…)

- Due to the grim outlook in its ‘core’ business, HBI has been acquiring other businesses at what we’d consider an alarming rate and at equally alarming prices. Its latest acquisition – an underwear company in Australia – is at 12x EBITDA according to the acquired company – despite Noll’s assertion that they were buying it closer to 10x EBITDA. Noll announced that he is stepping down before that deal even closes.

- According to what is dictated in the proxy statement, HBI takes egregious special charges that strip out of earnings costs what would otherwise prevent management from getting paid. These ‘adjusted earnings’ have been a key factor in Noll’s compensation, allowing him to sell $26mm in stock over the past 7 months.

- Its tax rate of 8.8% is unsustainably low, and is likely to head closer to a normal rate for your average US tax-paying multinational.

MDRX

To view our analyst's original report on Allscripts click here.

We continue to believe that much of Allscripts' (MDRX) announced deals and bookings over the past two years are not reflective of client’s firm commitment to Allscripts, but rather due to a deferment of a larger decision to switch vendors. Advocate Health signed a contract extension and hosting agreement for the use of Touchworks in 4Q15. According to management:

“This week another one of our largest Allscripts TouchWorks EHR clients, Advocate Medical Group, selected Allscripts hosting solutions to help improve system stability and overall performance. Advocate also signed a long-term extension for TouchWorks.” – Q3 Earnings Call

Advocate Health and Northshore Health have been trying to merge since September 2014, but the FTC was blocking the deal (originally planned to close in early 2015) over anti-trust concerns. However, it was announced this week (link to article) that a Judge ruled against the FTC request to block the merger, thus allowing the merger to proceed.

The problem for Allscripts is that Northshore University Health is a big Epic shop and in these types of situations, Epic almost always wins out as the vendor of choice for the combined organization. Therefore, it seems that Allscripts' days are numbered at Advocate, which would mark yet another pending ambulatory loss.

We continue to believe that Allscripts is $5-7 stock and see the pressure mounting over the next 12-18 months.

TIF

To view our analyst's original report on Tiffany click here.

Tiffany (TIF) has underperformed the retail sector. The company is down 4% over the last month while the Retail (XRT) is up 3%. Though the stock is down 20% year-to-date, we believe this short still has room to run. Sales are in decline, the company is poorly managed, and we do not think it is an acquisition target. Given our current research and the current macro data, we would not consider getting off this short unless 2017 EPS expectations came down 20%, or the stock dropped into the low 40s.

LAZ

To view our analyst's original report on Lazard click here.

While the technology sector created exciting headlines this week, with Microsoft's all cash bid for LinkedIn ($26 BB) and Symantec's acquisition of Blue Coat Systems ($4.7 BB), none of the boutique M&A firms caught part of the deals. Despite the flurry of activity, M&A announcements industrywide are down -14% globally year-to-date which we think is just an opening foray considering less active strategic buyers and a rising cost of capital.

For Lazard (LAZ) specifically, activity levels in 2Q have all but dried up, with transactions listed on their website down -37% year-over-year on an absolute deal count and a -74% drop in deal value. We lowered our annual estimates for 2016 to $2.49 this week, -17% below consensus and have an upcoming 2Q16 estimate of $0.57 (with Consensus at $0.61). Our fair value range is $22-$26 per share for LAZ stock based on 8-10x our out year estimates. The stock remains on our Best Ideas Short list.

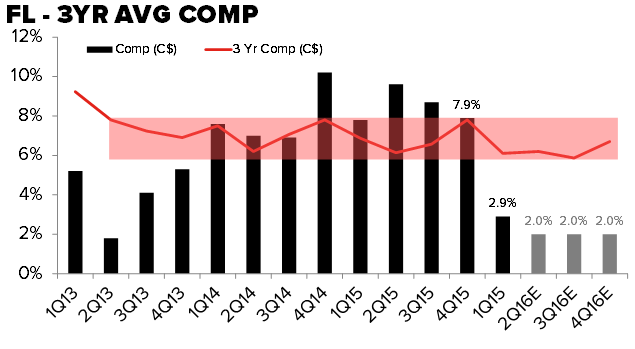

FL

To view our analyst's original report on Foot Locker click here.

Current expectations for Foot Locker (FL) 2Q look very difficult. The Street is expecting 90 cents in earnings driven by 3.6% comparable sales growth. However, the following data points lead us to believe these estimates are aggressive:

- The May comp was running negative at the time of the 1Q earnings call on 5/20 with management citing a shifted Jordan shoe launch as the cause. However, we have not seen any recovery in online traffic trends since that time, which have actually gotten worse.

- 2Q comparable sales and merchandise margin compares are harder than 1Q when FL missed comp by 160bps and gross margin by 30bps. We'd note our assumption of a 2% comp implies a sequential acceleration of 40bps on a 2 year basis and 10bps on the 3 year.

- Any comp miss puts significant pressure on margins as FL needs a low to mid-single digit comp to leverage occupancy and about the same to leverage SG&A. The FX SG&A tailwind is now completely gone, and management said clearly on the last call that SG&A leverage in 2Q will be difficult.

- On the 1Q conference call, Foot Locker management was as bearish on Nike as they have been in roughly 56 quarters. At first, it was the discussion about how Basketball was down mid-single digits in the quarter, and a misaligned price/value equation for Nike. But then we heard CEO Johnson talk of the ‘big turn’ at Adidas, and how he would like more product from both Adidas and UnderArmour. Whether its driven by FL trying to diversify away from Nike, or Nike taking action against a brash wholesale partner, any drop in Nike penetration is a negative for FL earnings in 2016 and beyond.

DE

To view our analyst's original report on Deere & Company click here.

No update on Deere & Company (DE) this week but Hedgeye Industrials analyst Jay Van Sciver reiterates his short call.

HOLX

To view our analyst's original report on Hologic click here.

We have been getting a lot of detailed feedback and hearing critiques from institutional investors regarding our Hologic (HOLX) short call. Comments suggest management has been refuting specific points from our presentations both directly and indirectly. Management comments conflict where we’ve been able to see them, however. Below is a quote from Steve MacMillan at a recent conference.

“So our current status, we are very pleased with the adoption cycle [for 3D]. There is still a long runway, and when I say a long runway, think about it this way, even a year from now, we will probably only be about halfway through our own installed base. So, again, still years of opportunity ahead of us and continuing to grow. 2017, we think we certainly will place more systems than 2016 and really the rate limiting step becomes frankly the capacity of the market to absorb additional growth more than our ability to install. So we feel great about what's going to continue to drive the business.” (emphasis added)

Once an adoption curve reaches 50% penetration, sequential growth has already gone negative and year-over-year growth has begun. Also, based on the 30% penetration highlighted as of September 2015 (and unchanged since) the arithmetic doesn’t match the comment. Rather, it tells us HOLX plans on only converting 2.5 percentage points of the market per quarter through next year (20 points over 8 quarters), well below metrics we see in our data for FY2015. So which is it? Are we going to grow in 2017 or are we going to be at 50% conversion and declining?

The bottom line is that our short is indeed less attractive today, at lower prices, than it was when we began. And Steve MacMillan remains one of our favorite CEOs. Consensus numbers have fallen dramatically for Breast Health, removing some margin of error we had alongside a falling multiple the Street is willing to pay, again removing some of our downside from here.

We’ll update our Tomo-Tracker this weekend. QTD the trend has slowed well below our negative forecast. It seems likely, unless the data changes, that we'll have to lower our estimates again, and perhaps that will open up some breathing room again.

A Special Update On Restoration Hardware:

Restoration Hardware (RH) was a long-time Investing Ideas company before we removed it in April. Due to continued subscriber interest, below is a HedgeyeTV video update via our Retail analysts Brian McGough and Alec Richards.