INTRODUCTION: We’re in the later innings of digging into EXPE. While we have reservations on the longer-term EXPE story (i.e. EXPE vs. PCLN), our sense is that the only two things that really matter to the story right now is the OWW integration (2016 EBITDA target) and the longer-term AWAY story. We discuss the latter below, note to follow on the former. In short, the AWAY business model transition presents a material near-term opportunity, and despite pushback from property owners, EXPE may be holding all the cards here (Pay to Play). More importantly, EXPE really doesn’t need much out of AWAY this year to drive sentiment around the longer-term story.

KEY POINTS

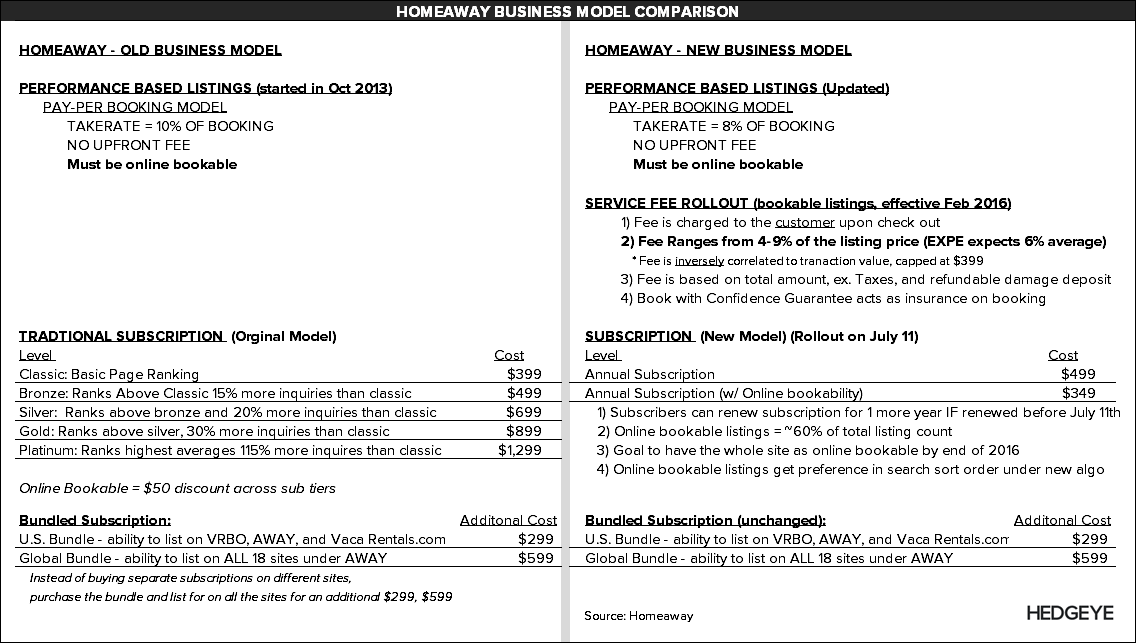

- MODEL TRANSITION: EXPE is trying to shift AWAY’s model more toward transactional than subscription-based. EXPE isn’t abandoning AWAY’s sub model, but trying to capture a take on its estimated $14-$16B in transactions that occur on the AWAY platform annually. AWAY had been in the process of rolling this out since 2013, but EXPE is now aggressively expediting the transition. Starting July 2016, EXPE will alter the search algorithm to prioritize online bookable properties rather than the prior method of ranking results by subscription tier (sub rates). Further, EXPE will be introducing a user fee, which also acts as insurance for the user.

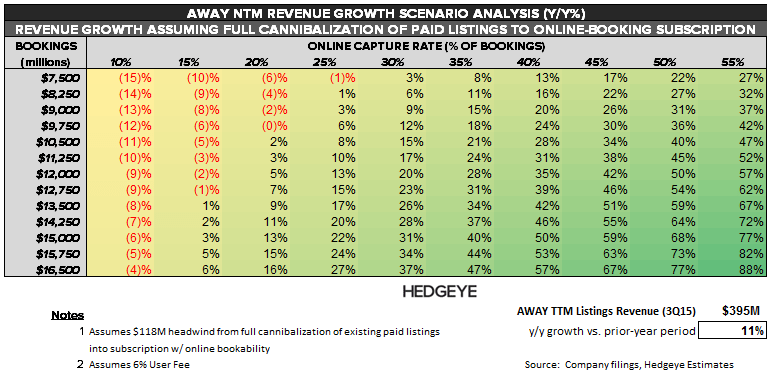

- NEAR-TERM OPPORTUNITY: The transition opportunity isn’t based on growing into some distant TAM, but capturing a commission on the $15B in estimated annual bookings that AWAY is already generating for its subs today. The clearest opportunity is the user fee, which could provide an incremental $900M assuming full online capture, but even a fraction of that opportunity would be material vs. AWAY’s $487M in 3Q15 TTM revenues (first scenario analysis below). If EXPE could sway its subs toward the Pay-Per-Book subscription (no sub fee, 8% take-rate), the opportunity grows to $2.1B. However, we doubt this happens without additional changes to the paid sub model, which will be largely dependent on the initial success of the transition.

- PAY TO PLAY: The new cost structure is causing a bit of backlash amongst property owners (here, here, here, and addressed by AWAY CEO, Brian Sharples: here). AWAY’s prior platform was very profitable for its listing subs (effective 3% take-rate, but much lower for US paid subscribers), so the push back makes sense. Naturally, there is some execution risk on the online bookability opt-in since these owners are incentivized to keep as much of that offline, but EXPE basically holds all the cards here since the owner bears all the financial risk. AWAY's paid subs are generating too much income from the service to push back; especially since that income is largely volume-dependent, and is also used to help pay down those property mortgages. Further, competition may be picking up within the vacation rental (VR) space, adding another layer of risk. We expect most paid subs to opt in; especially given the change to search algorithm starting 3Q16.

- CONTROLLING THE STORY: EXPE doesn’t need much in online bookings conversion out of AWAY to drive optimism in the story this year given the opportunity from the user fee alone. Remember that AWAY was a low-teens top-line grower prior to the acquisition; it’s possible that AWAY produces multiples of that rate, if not an acceleration, even under relatively restrictive bookings and conversion assumptions (see last scenario analysis below). More importantly, all mgmt really needs to here to fuel the story is show progress with the transition; it can basically cherry pick any metric it wants to do so. And given that we’re so early in the transition, we suspect mgmt has a pass over the 2-3 quarters if there are any hiccups along the way.

MODEL TRANSITION

EXPE is trying to shift AWAY’s model more toward transactional than subscription based. EXPE isn’t abandoning AWAY’s sub model (yet), but trying to capture a take on its estimated $14-$16B in transactions that occur on the AWAY platform annually.

AWAY had been in the process of rolling this out since 2013, but had been fairly passive about it. The only real incentive to adopt online bookability was a $50 discount off the subscription rate. AWAY’s search algorithm would still prioritize by the subscription tier (rate), so online bookability didn’t really have much of a draw unless the sub really believed it drive more transaction volume by doing so. Based on 3Q15 results, only about 25% had opted in for online bookability

However, EXPE is now aggressively expediting the transition. Starting July 11th the search algorithm will be on a “Best Match” Policy, which will be largely driven by whether the listing is online bookable and related factors such as inquiry response time and maintaining up-to-date calendars. EXPE is also providing only one subscription plan at $499 with a $150 discount if the property is online bookable.

EXPE is also introducing a service fee, which ranges from 4%-9% of the total transaction; EXPE expects the average rate to be around 6%. Certainly, the fee raises the price to the end consumer (and/or cuts into the price received by the owner). However, we don’t necessarily see the fee as a major deterrent to booking since the percentage is still lower than the 6%-12% charged by Airbnb. It’s also worth noting that the fee % is inversely correlated to transaction size (see table below) with a cap of $399, which would only be trigged on a rental of over $7300. Further, the fee comes with a booking guarantee, which protects against fraud, double-bookings, etc. In essence, the fee is also serving as insurance, which seems like it would be a big draw within the sharing economy, but granted that’s anecdotal.

NEAR-TERM OPPORTUNITY

The opportunity from the transition isn’t based on growing into a magical TAM, but on capturing a commission on the $15B in estimated annual bookings that AWAY is already generating for its subs today. Granted, that $15B is purely an estimate by AWAY’s own admission, but there’s still a strong opportunity for the transactional model even if the actual booking number is half of its estimate (see first scenario analysis below).

The clearest opportunity is in the user fee, which could provide an incremental $900M vs. $487M in AWAY’s TTM revenues (3Q15) if AWAY can capture 100% of the estimated $15B transactions online. If EXPE could sway its subs toward the Pay-Per-Book subscription (no sub fee, 8% take-rate), the total opportunity grows to $2.1B. However, we don’t believe the latter will happen unless AWAY forces it subs into it the pay-per-book (PPB) option, jacks up the price on paid subscriptions, or introducing a bookings fee for paid subs.

Either way, that’s not likely to happen until AWAY captures actual transaction volume online in order to better size up its actual bookings and the effective take-rate off of that. If AWAY discovers that its effective take-rate is as low as it believes, we believe it will sunset the paid sub model, at least in its existing form.

PAY TO PLAY

The new cost structure is causing a bit of backlash amongst the property owners (here, here, here, and finally addressed by AWAY CEO, Brian Sharples: here), which makes sense since AWAY’s prior platform was very profitable. We can’t definitviely calculate average bookings/listing since AWAY can’t either. But there are a few different ways to slice up the data to back into it, all of which point average annual bookings north of $10K for paid subs (see analysis below), which would effectively translate to commission of under 5% on its bookings. Note that likely skews much lower for US subs since they are monetizing at 2x the rate of EU, which in turn is dragging down the average booking calculation. For context, Int’l had represented roughly 33% of AWAY’s revenue prior to the acquisition. At a bare minimum, it’s probably safe to say that AWAY’s paid subs are doing in excess of $5K in average bookings; otherwise they probably would have opted into the pay-per-book option.

Naturally, there is some execution risk on the opt-in for online bookability since these owners are doing well enough without the option, and it’s easier to avoid taxes without an electronic trail. The user fee also effectively makes the transaction more expensive, so the user is theoretically less likely to book. But we suspect the real reason why AWAY’s paid subs are resisting the change is that they simply don’t want to put AWAY in a position to take price on them; moving those transactions online would do exactly that. AWAY would have a better idea of how much business it's actually generating for its subscribers, and in turn, its effective take-rate off of that. If AWAY adjust its pricing model accordingly.

But ultimately we believe AWAY holds all the cards here, and the property owners need to play ball. Naturally, the change in the search algorithm puts those without bookability at a disadvantage. But we believe the more important factor is that there is just too much rental income at risk to try and steer the transaction offline, especially since that income is largely volume dependent.

AWAY’s average bookings per transaction ranges between $1k and $2K depending on which metric you’re using (Escapia average or EXPE’s expected average user fee). Compare that to average annual rental income that is well in excess of $10K, and there is a lot of risk to losing any transaction volume, especially considering that over 60% of vacation properties are mortgaged, with roughly half over 70% financed. Competition may also be heating up within the Vacation Rental space. Vacation property purchases were particularly strong for over the past two year (2014 was a record); according to the NAR, 40% of 2015 vacation home buyers plan to rent these properties out for income. In short, the secular tailwind in VR demand is being met with increasing supply.

In short, EXPE is changing the rules of the game, and we don’t believe AWAY’s property owners can do much about it since they bear the brunt of the financial risk, and are in increasing competition with each another.

CONTROLLING THE STORY

EXPE doesn’t need that much in online bookings conversion out of AWAY to fuel optimism in the story this year given the opportunity from the user fee alone. In the last scenario analysis below, we illustrate the opportunity by flexing annual bookings against online capture rate. We’re only factoring in the user fee while assuming full cannibalization of AWAY’s paid subs into the online booking subscription ($118M headwind based on 3Q15 Paid Sub ARPU).

The negative is the risk of declining revenue from paid sub cannibalization, but that would essentially require less than a 20% capture rate despite all listings having online bookability in our analysis. The positive is that AWAY could still drive growth even if its actual bookings are half of its 2015 estimate. Under most logical assumptions, AWAY is producing accelerating Listings revenue growth this year vs. the 11% growth it produced in the TTM period ending 3Q15.

However, note that the new search algorithm and subscription plans don’t kick in until 3Q16 (July 11th), so we may not see a sudden surge bookable listings, especially since the opt-in will likely not occur overnight. However, the user fee has already kicked in (Feb), and we already know booking volume more than doubled y/y in 1Q (170% y/y), so we’ll start to see some of that flow through to 2Q/3Q revenue, which is based on the stay not the booking. Further, the transactional model is more seasonal, which should inflate AWAY’s 2Q/3Q growth rates vs. the year ago period.

But more importantly, all EXPE mgmt really needs to do is show progress with the transition, and mgmt will have a handful of metrics that it can cherry pick to paint any picture it wants. So even if revenues do initially decline from sub cannibalization, mgmt could chalk it up to higher-than-expected opt-in to online model, which will only breed optimism for the longer term story. If transaction volume growth decelerates vs. that 1Q metric, mgmt could blame it on the timing of algo/model change. It’s hard to envision a scenario that management couldn’t talk around since it’s still very early in the transition.

That said, we suspect mgmt has a pass over the 2-3 quarters if there are any hiccups since it is still very early in the transition. On the other hand, if mgmt shows any signs progress with the transition, the story only gains momentum.

Let us know if you have questions, or would like to discuss in more detail.