- We are lowering our full year LAZ earnings estimate to $2.49 for '16 and remain at $2.57 for '17, -17% and -27% below Consensus

- We continue to outline that Lazard has the most exposure to the upcoming BREXIT vote with over 25% of global advisory revenues in Europe. A withdrawal by Britain would be the worst case scenario

- The M&A cycle peaked last year in our view and historically new restructuring revenue takes 2 years to offset M&A losses (but overall Advisory revenues never comp up overall -- see our BlackBook below)

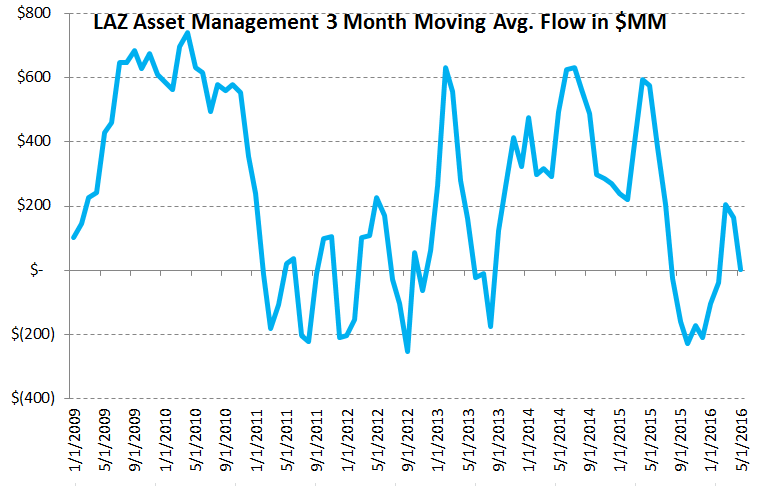

- The asset management business is working on a slightly better quarter solely on market appreciation as our data outlines no organic growth in 2Q16 thus far

- LAZ shares remain a value trap in our view with Consensus estimates that need a substantial haircut and financials that won't comp up for at least the balance of 2016

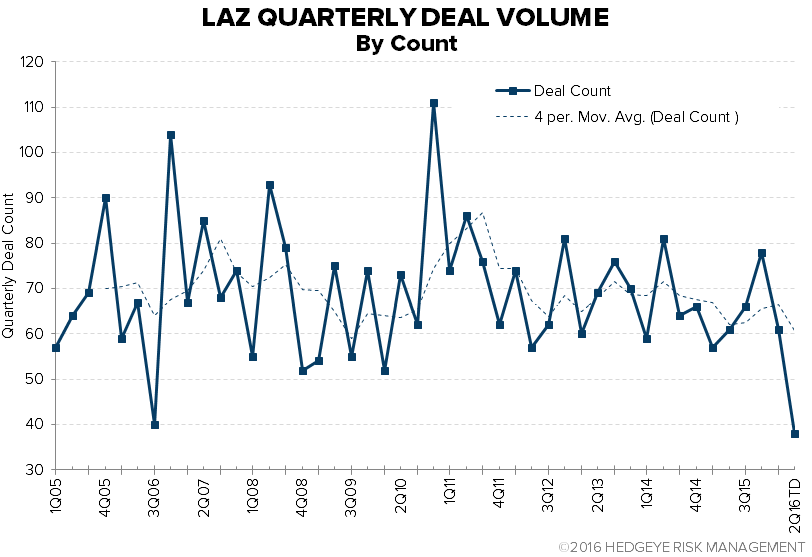

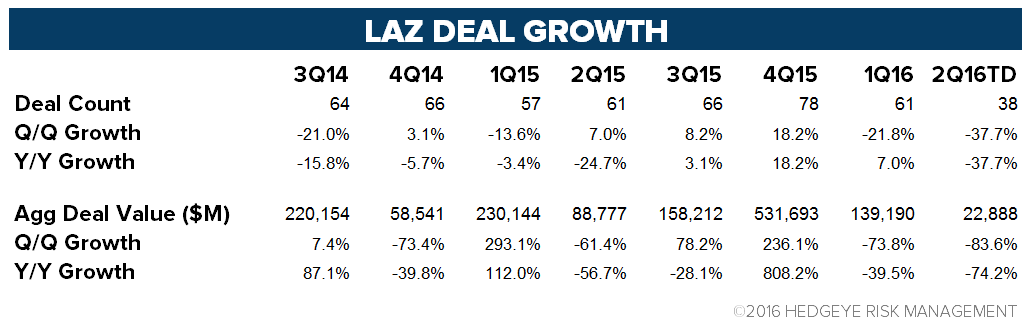

While the technology sector yesterday created exciting headlines with Microsoft's all cash bid for LinkedIn ($26 BB) and Symantec's acquisition of Blue Coat Systems ($4.7 BB), none of the boutique M&A firms caught part of the deals. Despite the flurry of activity, M&A announcements industry wide are down -14% globally year-to-date which we think is just an opening foray considering less active strategic buyers and a rising cost of capital. For Lazard specifically, activity levels in 2Q have all but dried up, with transactions listed on their website down -37% year-over-year on an absolute deal count and a -74% drop in deal value. While the firm doesn't disclose all activity online (restructuring deals are listed when completed with M&A transactions listed on an announced basis), the dearth in activity is sharper than we expected. We are lowering our annual estimates for 2016 to $2.49, -17% below consensus and have an upcoming 2Q16 estimate of $0.57 (with Consensus at $0.61). Rebounding global equity markets with average balances up +6% thus far in the second quarter should salvage a really low 2Q result within the asset management division. However this slight improvement is solely due to markets as a rolling 3 month average of Lazard Asset Management flows from Morningstar has flat organic growth brewing for 2Q16.

We continue to ascribe a fair value range of $22-$26 for LAZ shares based on 8-10x our out year estimates and the stock remains on our Best Ideas Short list. We do not think shares are attractive on valuation until fundamentals comp higher year-over-year which we don't see until 2017.

LAZ - Incremental Color in 10Q is Dark

LAZ - Don't Get Caught Watching the Paint Dry

LAZ - Hiring in Restructuring, Chairman Bullish From Davos

LAZ - Value Trap - Best Ideas BlackBook

LAZ - As Good As It Gets - Adding to Best Ideas

Please let us know of questions,

Jonathan Casteleyn, CFA, CMT

Joshua Steiner, CFA